Home›Personal Loans›Best Personal Loans for Veterans and Military of 2026

Advertiser Disclosure: WiseIQ is reader-supported. When you apply through links on this page, we may earn a commission at no extra cost to you. Learn more.

PERSONAL LOANS

Best Personal Loans for Veterans and Military of 2026

Sorted by APR. These are today's best rates for your loan amount.

Filtered for lenders most likely to approve your application.

Sorted by funding speed. Same-day and next-day options highlighted.

Personal loans built for debt consolidation — lower rates than most credit cards.

We've simplified the comparison to the top 3 options for first-time borrowers.

Based on your browsing, here are the top picks most users in your position chose.

LIVE RATE8.99% APRfor qualified borrowers · No hard credit pull

📋 Reviewed by WiseIQ Editorial Team · Updated April 2026 · Editorially independent

Explore top personal loan options tailored for veterans and military members. Our guide helps you find competitive rates, flexible terms, and exclusive benefits to meet your financial needs.

WiseIQ Expert Tip

Before accepting any loan offer, calculate the total cost of the loan (principal + all interest + fees). A lower monthly payment often means paying thousands more over the life of the loan.

Quick Comparison: Best Personal Loans for Veterans and Military at a Glance

WISEIQ TOP PICK

PERSONAL LOANS

Upstart

Best for fair & thin credit · AI-powered approval

APR RANGE

7.80%–35.99%

LOAN AMOUNT

$1K–$50K

MIN. CREDIT

300

✓ No prepayment penalty✓ Funds in 1 business day✓ Soft pull pre-qualification✓ Considers education & job history

A personal loan is not the right tool for every situation. Consider alternatives if any of the following apply to you:

You have home equity: A HELOC typically offers rates 5–10% lower than personal loans. If you own your home, compare HELOC rates before taking a personal loan.

Your debt is primarily credit card debt: A balance transfer card with a 0% intro APR (typically 12–21 months) will cost less than a personal loan if you can pay off the balance within the intro period.

You need less than $1,000: Most personal loan lenders have minimum amounts of $1,000–$2,000. For smaller needs, a credit union payday alternative loan (PAL) or a 0% APR credit card may be more appropriate.

Your credit score is below 500: Most personal loan lenders — including those that accept "bad credit" — have practical minimums around 500–560. Below this, secured loans, credit-builder loans, or co-signer arrangements are more realistic options.

You are in active bankruptcy: Personal loan lenders will decline applicants in active Chapter 7 or Chapter 13 proceedings. Resolve your bankruptcy first.

🎯

Not sure which option is right for you?

Answer 3 quick questions and get a personalized recommendation in seconds.

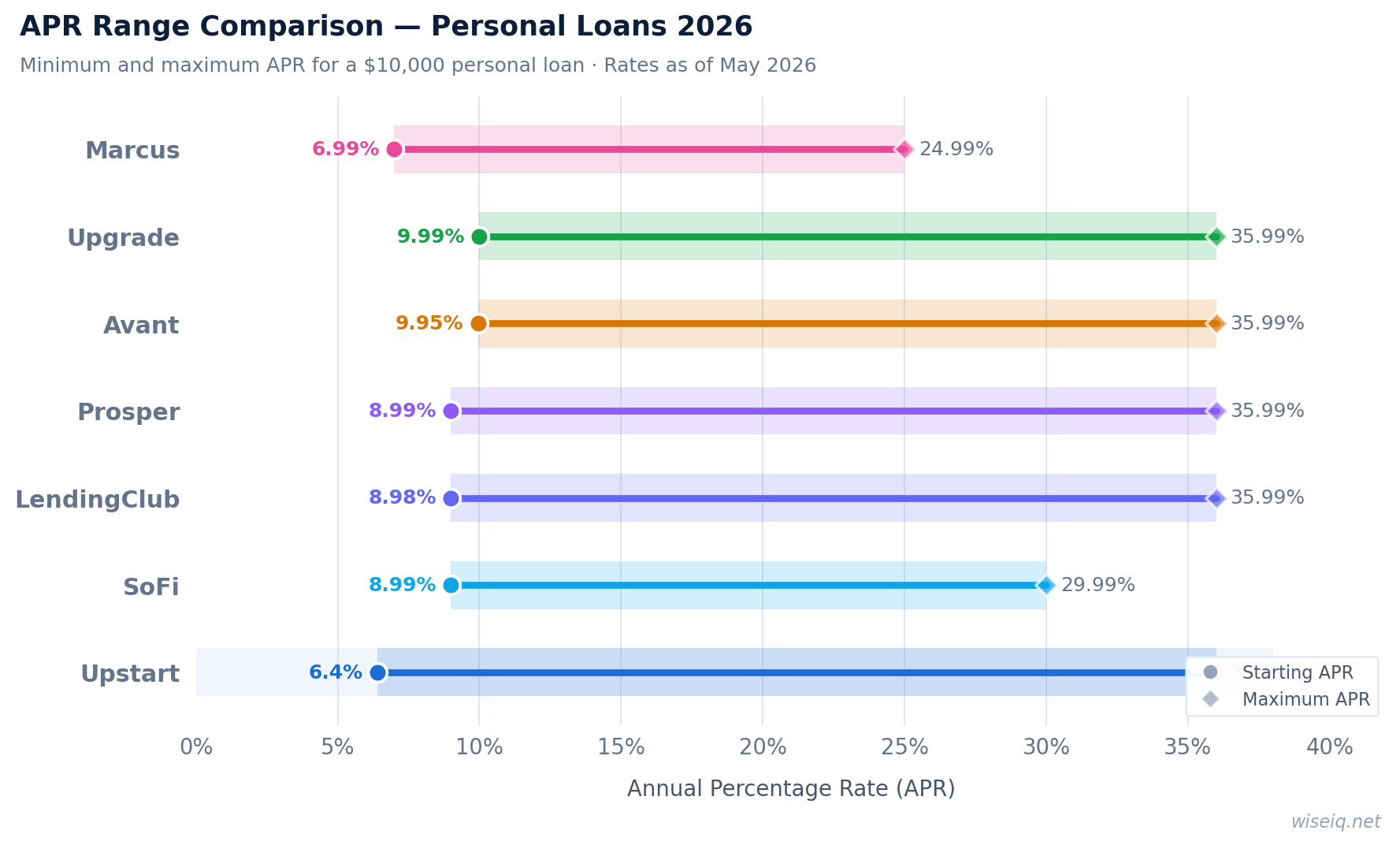

APR Range Comparison: Personal Loans 2026 — Starting and maximum APR for a $10,000 loan. Rates verified May 2026.

How We Chose the Best Personal Loans for Veterans and Military

Our Selection Criteria:

Military-Specific Benefits:We prioritized lenders offering exclusive rates, discounts, or tailored services for active-duty military, veterans, and their families.

Competitive Rates & Fees:Loans with low Annual Percentage Rates (APR) and minimal or no fees (origination, prepayment, late) were favored to ensure affordability.

Flexible Loan Terms & Amounts:We considered lenders providing a wide range of loan amounts and repayment terms to accommodate diverse financial needs.

Accessibility & Eligibility:Lenders with clear eligibility requirements and straightforward application processes, including options for various credit profiles, were highly rated.

Who Should Apply?

Active-Duty Service Members:

If you are currently serving in the military and need funds for unexpected expenses, debt consolidation, or a major purchase, these loans offer competitive rates and often include benefits like SCRA protections or autopay discounts. Lenders like Navy Federal and USAA are particularly well-suited for your needs.

Veterans:

For those who have honorably served, personal loans can provide financial flexibility for home improvements, starting a business, or managing existing debt. Many lenders recognize your service with favorable terms, even if you are no longer active duty.

Military Spouses and Dependents:

Eligible family members of service members and veterans can also access these specialized loan products. This ensures that military families as a whole can benefit from competitive financing options and dedicated support.

Individuals Seeking Debt Consolidation:

If you're looking to simplify your finances by combining high-interest debts into a single, lower-rate monthly payment, personal loans from these providers can be an excellent solution. The fixed rates offer predictability and can help you save money over time.

We monitor rates across 50+ lenders and alert you when better options become available for your profile.

No spam. Unsubscribe anytime. We never sell your data.

W

WiseIQ Editorial Team

Reviewed by Certified Financial Planners & Industry Experts

Our editorial team consists of financial writers, CFPs, and former banking professionals dedicated to providing accurate, unbiased financial guidance. All content is fact-checked and updated regularly. Learn about our editorial standards →

Frequently Asked Questions

What is the Servicemembers Civil Relief Act (SCRA)?

The SCRA is a federal law that provides financial and legal protections for active-duty military members, reservists, and National Guard members called to active duty. It can cap interest rates on pre-service debts at 6%, prevent foreclosures, and offer other legal safeguards.

Can I get a personal loan with bad credit as a veteran?

While many top lenders prefer good to excellent credit, some financial institutions and credit unions specializing in military members may offer more flexible eligibility criteria or alternative loan products. It's always recommended to check your credit score and explore options with lenders like Navy Federal or PenFed, which cater to a broader range of credit profiles within the military community.

Are there any specific personal loan programs for disabled veterans?

While there aren't widely advertised personal loan programs exclusively for disabled veterans, many lenders consider disability benefits as income, which can aid in loan qualification. Additionally, organizations like the VA offer various benefits and programs that can indirectly assist with financial needs, such as grants or aid for specific purposes.

What documents do I need to apply for a personal loan as a military member or veteran?

Typically, you'll need proof of identity (e.g., driver's license, military ID), proof of income (e.g., LES, pay stubs, W-2s, disability statements), and bank account information. Lenders may also request proof of military service, such as a DD-214 or a Statement of Service, to verify eligibility for military-specific benefits.

Focus on the Annual Percentage Rate (APR), which includes both interest and fees. Compare minimum credit score requirements, funding speed, loan amounts, and repayment terms. Read recent customer reviews on Trustpilot and the BBB. Getting pre-qualified lets you see real personalized offers.

The interest rate is the base cost of borrowing. APR (Annual Percentage Rate) includes the interest rate plus all fees (origination fees, closing costs, etc.), expressed as a yearly rate. APR gives you a more complete picture of the true cost of a loan — always compare APRs, not just interest rates.

Credit scores have a dramatic impact on rates. On a $20,000 personal loan, the difference between a 720 score (8% APR) and a 580 score (25% APR) is over $9,000 in additional interest over 5 years. Improving your score before applying can save thousands.

Reputable online lenders use bank-level encryption (256-bit SSL) to protect your data. Look for HTTPS in the URL, check that the lender is registered in your state, verify their BBB rating, and read privacy policies before submitting personal information. Avoid lenders who contact you unsolicited.