A Home Equity Line of Credit (HELOC) is a popular way to tap home equity, but it comes with significant drawbacks: your home is collateral (foreclosure risk), rates are variable, and approval takes 2–6 weeks. Depending on your situation, one of these alternatives may be a better fit.

Best Alternatives

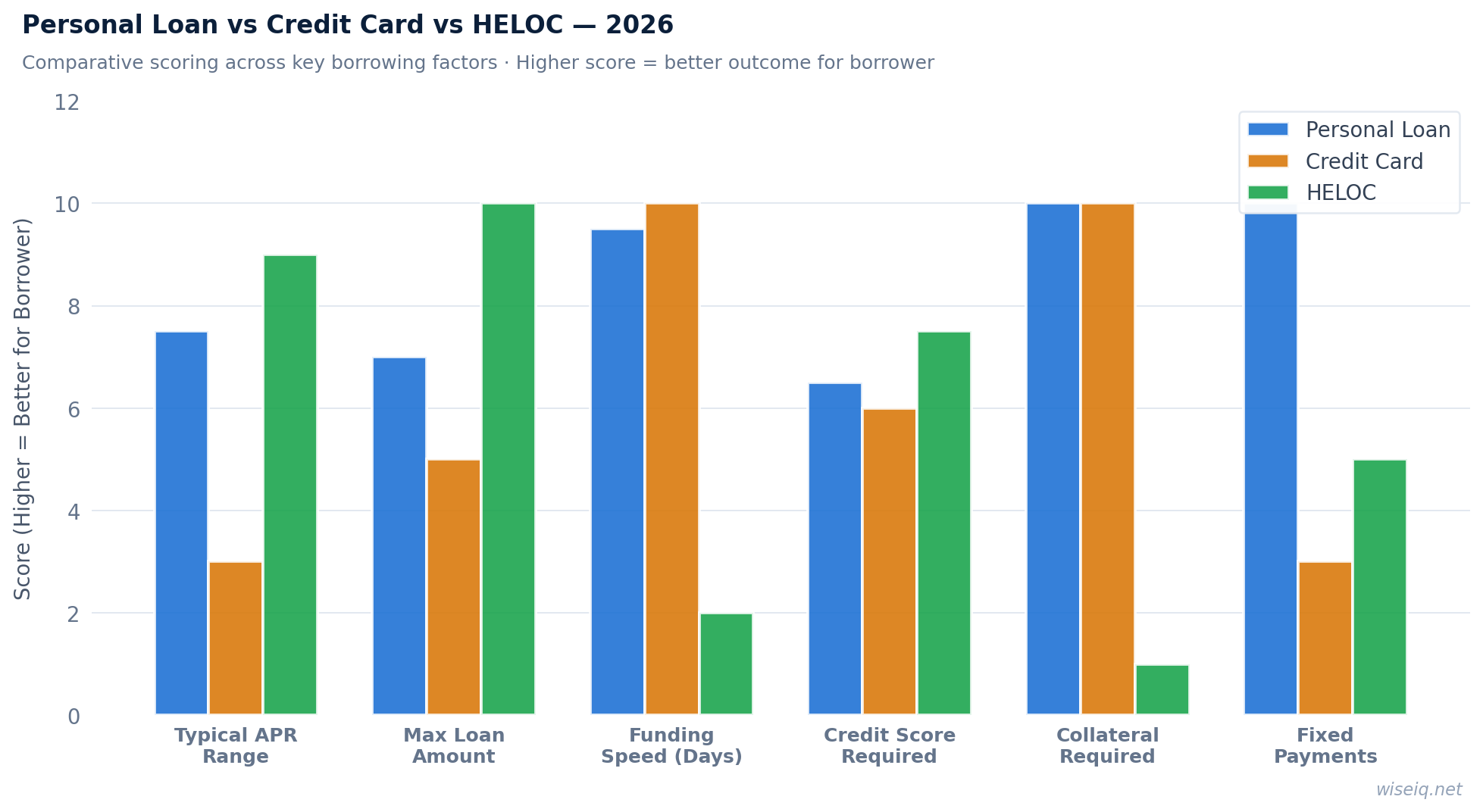

Personal Loan

Unsecured personal loans from lenders like SoFi, Upstart, and LightStream offer up to $100,000 with no home equity required. Rates start at 6.99% for excellent credit.

Pros: No collateral, funds in 1–3 days, fixed rate

Cons: Higher rate than HELOC for large amounts

Home Equity Loan

A home equity loan (second mortgage) gives you a lump sum at a fixed rate, unlike a HELOC's variable rate line of credit. Your home is still collateral.

Pros: Fixed rate, predictable payments, lower rate than personal loan

Cons: Home is collateral, takes 2–6 weeks

Cash-Out Refinance

Replace your existing mortgage with a larger one and take the difference in cash. Best when current rates are lower than your existing mortgage rate.

Pros: Single payment, potentially lower rate

Cons: Resets mortgage term, closing costs 2–5%

0% APR Credit Card

For smaller home improvement projects under $10,000, a 0% APR credit card offers interest-free financing for 12–21 months.

Pros: 0% interest for promo period, rewards

Cons: Limited to credit limit, high rate after promo

FHA 203(k) Rehab Loan

For major renovations, an FHA 203(k) loan combines your mortgage and renovation costs into one loan. Requires a licensed contractor.

Pros: High loan amounts, low down payment

Cons: Complex process, requires contractor, FHA limits

Government Grants and Programs

The USDA Rural Repair and Rehabilitation program and HUD's HOME program offer grants and low-interest loans for home repairs to eligible homeowners.

Pros: May not need to repay (grants)

Cons: Income limits, geographic restrictions, long process

Get Weekly Rate Alerts — Free

We monitor rates across 50+ lenders and alert you when better options become available for your profile.

No spam. Unsubscribe anytime. We never sell your data.

WiseIQ Editorial Team

Reviewed by Certified Financial Planners & Industry Experts

Our editorial team consists of financial writers, CFPs, and former banking professionals dedicated to providing accurate, unbiased financial guidance. All content is fact-checked and updated regularly. Learn about our editorial standards →

Frequently Asked Questions

What is the best alternative to a HELOC? +

For most borrowers, a personal loan is the best HELOC alternative. It funds in 1–3 days, has no foreclosure risk, and offers fixed rates. For larger projects where you have significant equity, a home equity loan at a fixed rate may offer a lower rate.

Can I get a home improvement loan without equity? +

Yes. Personal loans don't require home equity. Lenders like SoFi and LightStream offer up to $100,000 for home improvement with no collateral required.

Is a personal loan or HELOC better for home improvement? +

A personal loan is better if you want speed (funds in 1–3 days vs. 2–6 weeks), a fixed rate, and no risk to your home. A HELOC may offer a lower rate if you have significant equity and can wait for approval.

What is the difference between a HELOC and a home equity loan? +

A HELOC is a revolving line of credit with a variable rate. A home equity loan is a lump-sum loan with a fixed rate. Both use your home as collateral. A home equity loan is better if you want payment predictability.

How much can I borrow with a personal loan for home improvement? +

Most personal loan lenders offer up to $35,000–$100,000 for home improvement. SoFi and LightStream offer up to $100,000. The amount you qualify for depends on your credit score and income.

Advertiser Disclosure: WiseIQ may earn a referral fee from some lenders and financial products on this page. This does not influence our editorial ratings or recommendations. Our reviews are independently researched and editorially independent.