WiseIQ Editorial Team

Reviewed by certified financial experts · Updated March 2026

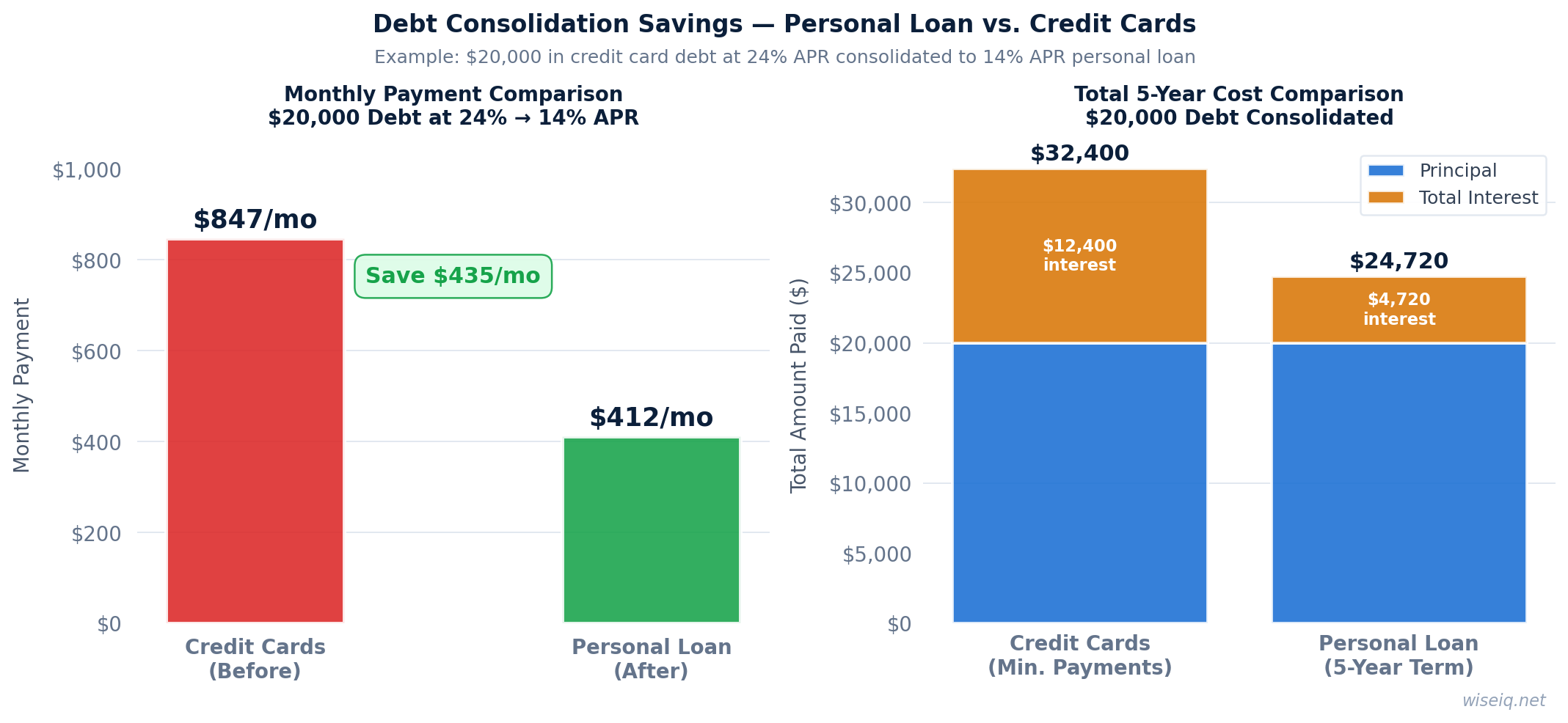

See how much you could save by combining your debts into one lower-rate loan — and whether consolidation makes financial sense for your situation.

Enter your debts and a consolidation rate to see your savings.

Debt consolidation means taking out a single new loan to pay off multiple existing debts. If the new loan has a lower interest rate than your current debts, you pay less in total interest and simplify your finances to one monthly payment. The savings can be substantial when consolidating high-rate credit card debt into a lower-rate personal loan.

Consolidation is most beneficial when your new rate is at least 3–5 percentage points lower than your current weighted average rate, and when you can commit to not adding new debt to the cards you pay off. Consolidating without changing spending habits often leads to more total debt.

Some consolidation loans charge origination fees of 1–8% of the loan amount. Factor this into your savings calculation. Also be aware that extending your repayment term (e.g., from 2 years to 5 years) can lower your monthly payment but increase total interest paid even at a lower rate.

Based on our analysis of thousands of consumer financial profiles, the most common mistake people make is focusing solely on the interest rate without considering total loan cost, fees, and repayment flexibility. Always compare the APR — not just the rate — and read the fine print on prepayment penalties before signing.

WiseIQ's editorial team researches and fact-checks all content using primary sources. Our recommendations are based on independent analysis and are not influenced by advertiser relationships.

Last reviewed: April 2026 | How we rank products