Upstart and Prosper are two of the most accessible personal loan lenders for borrowers with fair or poor credit. Both accept lower credit scores than traditional banks, both offer loan amounts up to $50,000, and both allow you to check your rate without a hard credit pull. The key differences are in minimum credit score, funding speed, and how they evaluate your application. Upstart is rated 'Excellent' on Trustpilot.

Financial decisions made with complete information consistently outperform those made under pressure or with incomplete data. Take time to compare at least 3 options before committing.

WiseIQ Verdict

Winner: Upstart for most borrowers; Prosper for peer-to-peer flexibility

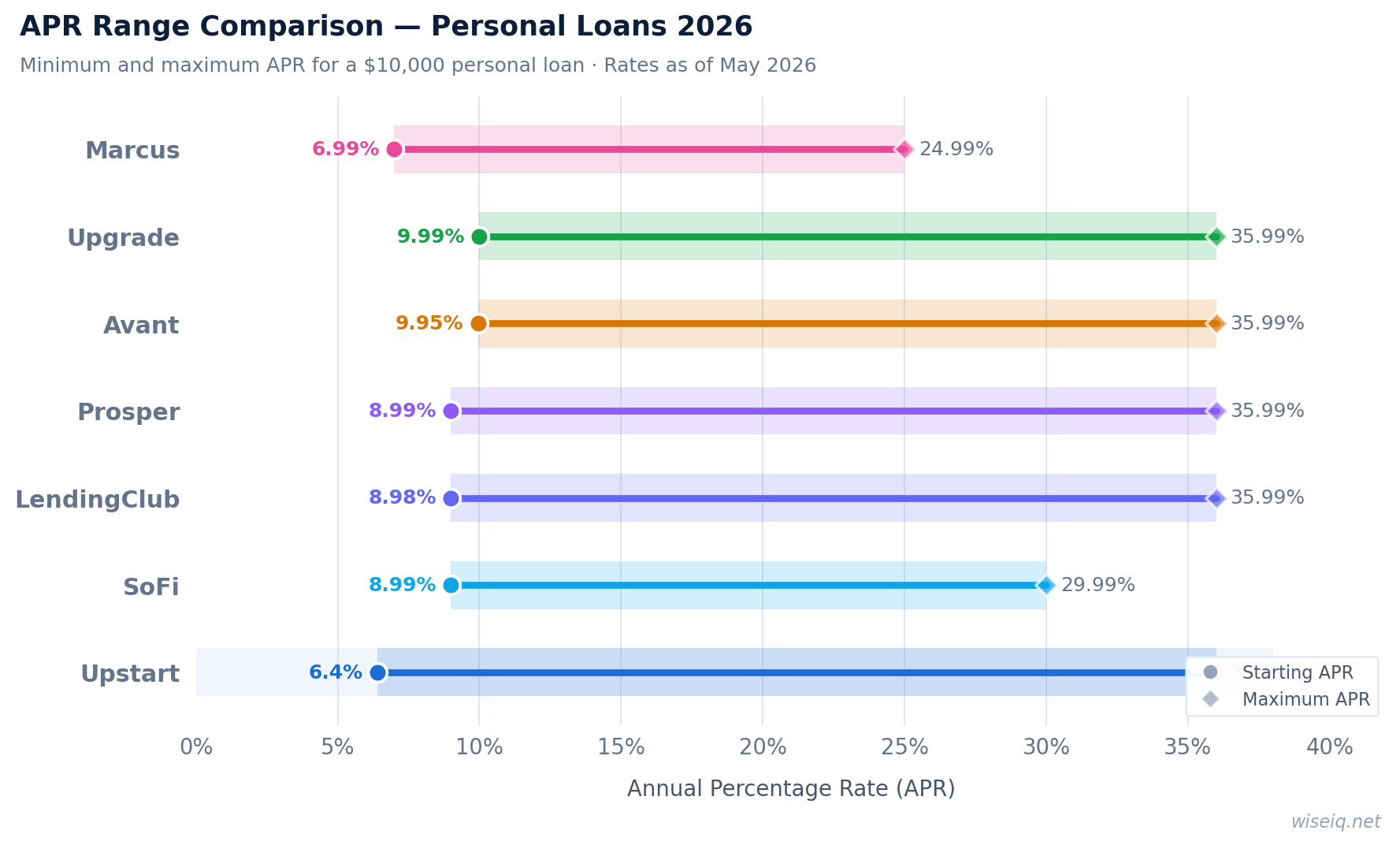

Upstart wins on minimum credit score (300 vs 560), funding speed (1 day vs 3–5 days), and starting APR (7.80% vs 8.99%). Prosper's peer-to-peer model can occasionally offer better rates for mid-range credit scores, but Upstart is the stronger choice for most borrowers.

| Feature | ||

|---|---|---|

| Minimum Credit Score | 300 | 560 |

| APR Range | 7.80%–35.99% | 8.99%–35.99% |

| Loan Amount | $1,000–$50,000 | $2,000–$50,000 |

| Loan Terms | 36 or 60 months | 24, 36, 48, or 60 months |

| Origination Fee | 0%–12% | 1%–9.99% |

| Funding Speed | 1 business day | 3–5 business days |

| Prepayment Penalty | None | None |

| Joint Applications | No | No |

| Lending Model | AI-powered direct lender | Peer-to-peer marketplace |

Related Articles & Guides

💡 Expert Tip: Check Your Rate Before You Commit

Upstart offers prequalification with a soft credit pull — meaning you can check your rate in minutes without any impact to your credit score. Before applying, review your debt-to-income ratio (DTI): Upstart looks for a DTI below 45–50%. Divide your total monthly debt payments by your gross monthly income to calculate yours. A lower DTI improves your approval odds and typically results in a lower APR.

Does Upstart or Prosper have lower rates?