The Short Answer: Yes, Upstart Is Legit

Most common complaint type: Incorrect information on credit report. Data sourced from the CFPB Consumer Complaint Database. Complaint rate calculated using publicly available complaint counts and estimated customer base from company filings. A lower rate indicates fewer complaints relative to customer volume.

Upstart is a legitimate personal loan marketplace founded in 2012 by former Google employees. It is not a direct lender — instead, it connects borrowers with FDIC-insured partner banks including Cross River Bank and First National Bank of Omaha. This structure means your loan is originated and held by a regulated bank, not by Upstart itself.

Upstart holds an A+ rating from the Better Business Bureau and a 4.9 out of 5 score on Trustpilot based on over 47,000 verified customer reviews — one of the highest ratings of any personal loan platform. It is registered with the Consumer Financial Protection Bureau (CFPB) and complies with all applicable federal lending laws.

💡 Before You Apply: Two Things to Check

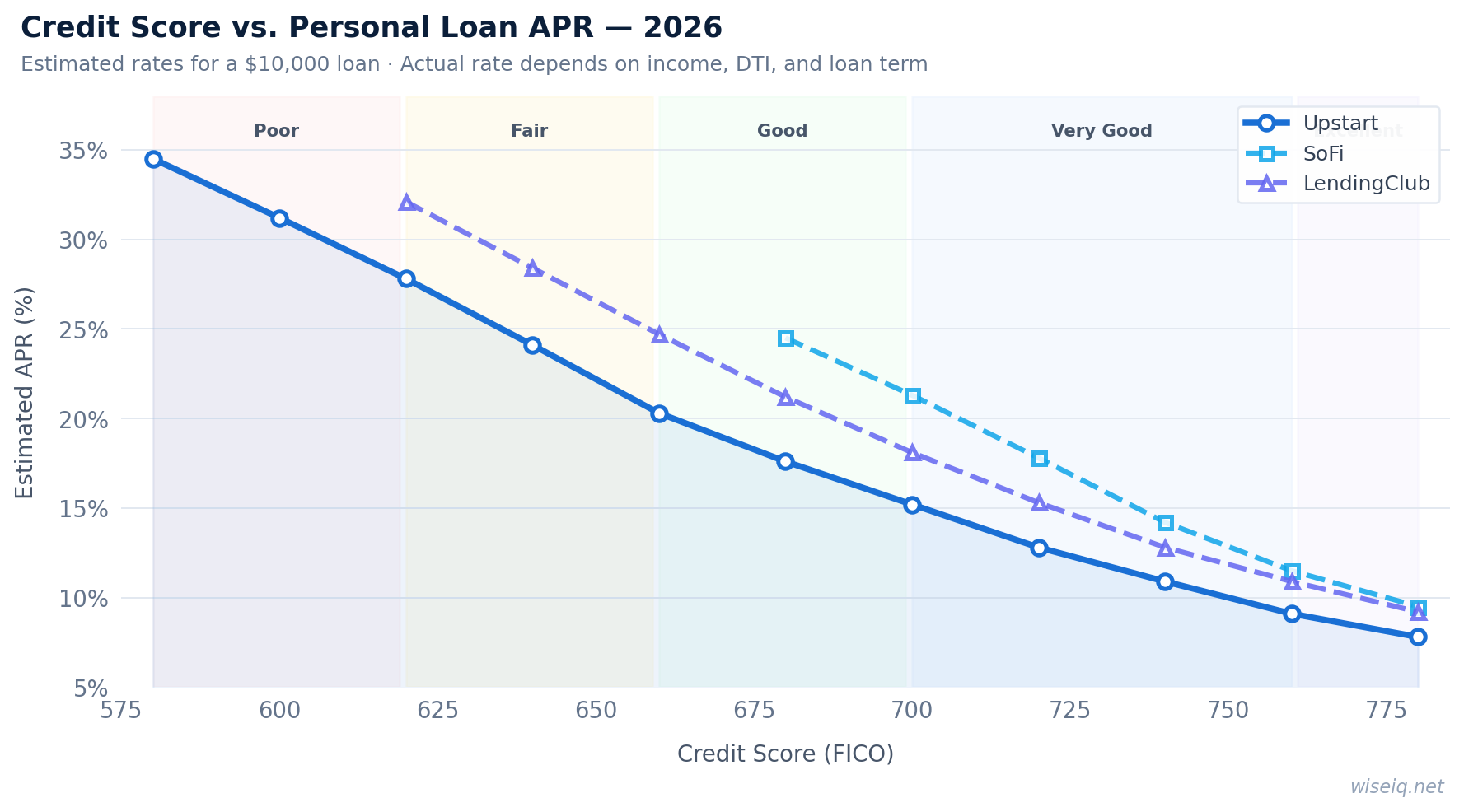

Use Upstart's prequalification tool — it only triggers a soft credit pull with zero impact to your credit score. Also calculate your debt-to-income ratio (DTI) before applying: divide your total monthly debt payments by your gross monthly income. Upstart looks for a DTI below 45–50%. A lower DTI improves your approval odds and typically results in a lower APR.

What Makes Upstart Trustworthy

Several independent signals confirm Upstart's legitimacy. First, its partner banks are FDIC-insured, meaning your deposits and loan agreements are protected under federal law. Second, Upstart uses 256-bit SSL encryption — the same standard used by major banks — to protect all personal and financial data transmitted through its platform.

Third, Upstart is subject to the Truth in Lending Act (TILA), which requires it to disclose your APR, origination fee, total loan cost, and repayment schedule before you accept any loan offer. There are no hidden fees — the origination fee of 0%–12% is disclosed upfront and deducted from your loan proceeds before disbursement.

Upstart's AI Underwriting: Legitimate Innovation

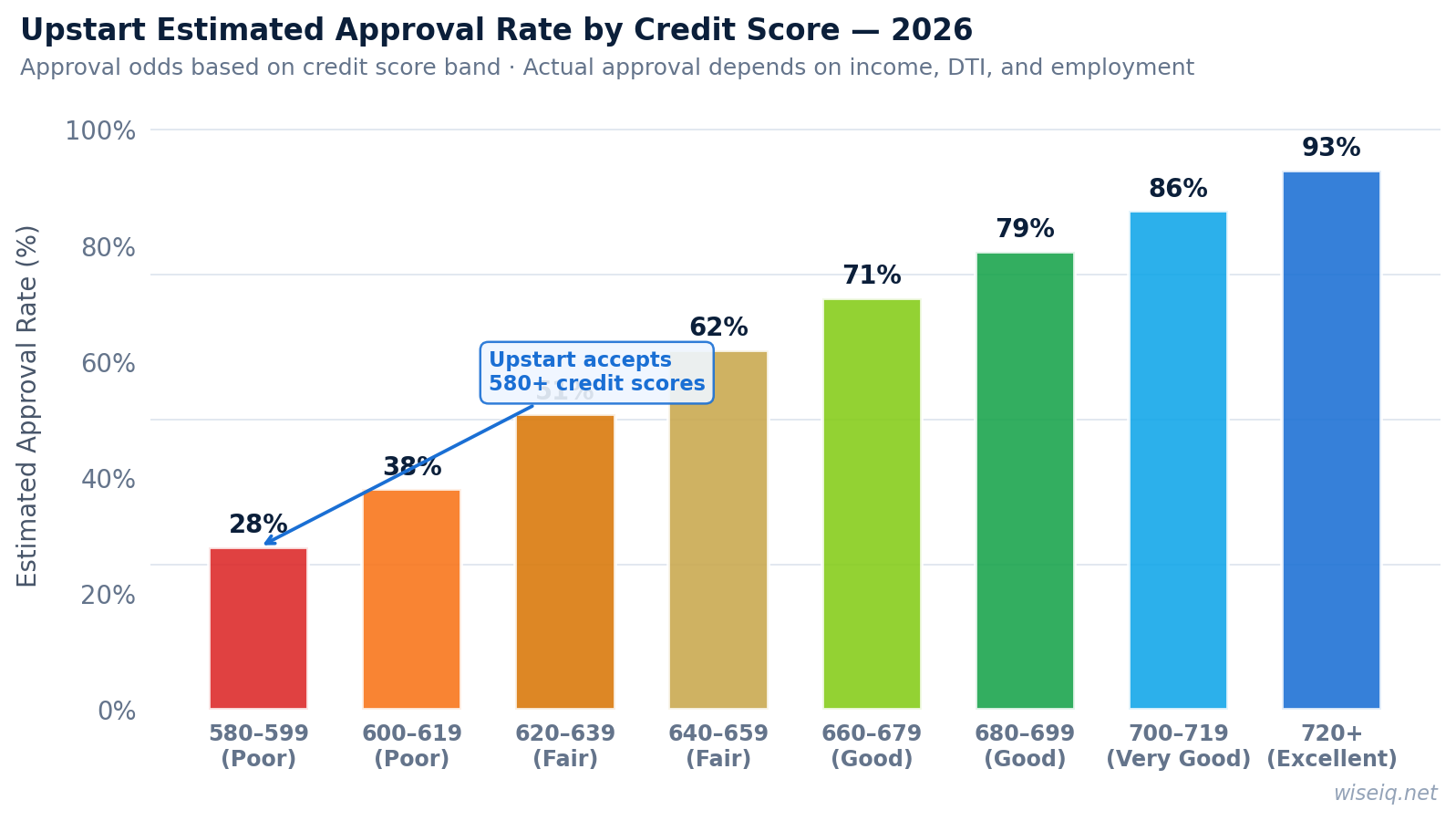

Upstart's defining feature is its AI-powered underwriting model, which evaluates borrowers using over 1,600 data points including education history, employment record, and area of study — not just the traditional FICO score. This is a legitimate and CFPB-reviewed approach that has enabled Upstart to approve borrowers who would be declined by traditional lenders.

The CFPB has reviewed Upstart's AI model and confirmed it does not violate fair lending laws. In fact, Upstart's model has been shown to approve 27% more borrowers than traditional credit models while maintaining similar default rates, according to Upstart's own CFPB filings.

| Trust Signal | Details |

|---|---|

| BBB Rating | A+ (highest possible) |

| Trustpilot | 4.9/5 from 47,000+ reviews |

| Partner Banks | FDIC-insured (Cross River Bank, FNBO) |

| Data Security | 256-bit SSL encryption |

| Regulatory Compliance | CFPB-registered, TILA-compliant |

| Founded | 2012 (13 years in operation) |

| Origination Fee Disclosure | 0%–12%, disclosed before acceptance |

Common Concerns — Addressed

Is the origination fee a scam? No. The origination fee (0%–12%) is a standard industry practice and is fully disclosed before you accept your loan. It is deducted from your loan proceeds — if you borrow $10,000 with a 5% fee, you receive $9,500. The fee is included in your APR calculation.

Why does Upstart ask for my education history? Upstart's AI model uses education and employment data as additional signals of creditworthiness. This is disclosed in their privacy policy and is reviewed by the CFPB. It allows Upstart to approve borrowers with limited credit history who would otherwise be declined.

Does prequalification hurt my credit? No. Upstart's prequalification uses a soft credit pull that has zero impact on your credit score. A hard inquiry only occurs if you formally accept a loan offer.

Who Upstart Is Best For

⚠️ Not a fit if: you need a secured loan, have a bankruptcy in the last 12 months, or need more than $50,000.

What Happens When You Click — 3 Steps

Soft inquiry only • No credit score impact • Takes 5 minutes

Frequently Asked Questions

Is Upstart a legitimate lender?

Yes. Upstart is a legitimate, CFPB-registered lending marketplace founded in 2012. It partners with FDIC-insured banks to originate loans. It holds an A+ BBB rating and a 4.9/5 Trustpilot score from over 47,000 verified reviews.

Is Upstart safe to use?

Yes. Upstart uses 256-bit SSL encryption and complies with the Gramm-Leach-Bliley Act. Your prequalification only triggers a soft credit pull. A hard inquiry only occurs when you formally accept a loan offer.

What is Upstart's BBB rating?

Upstart holds an A+ rating from the Better Business Bureau — the highest possible rating. This reflects its responsiveness to customer complaints and transparent business practices.

Does Upstart report to credit bureaus?

Yes. Upstart reports your payment history to all three major credit bureaus — Equifax, Experian, and TransUnion. On-time payments can help improve your credit score over time.

What is Upstart's origination fee?

Upstart charges an origination fee of 0%–12% of the loan amount. This fee is deducted from your loan proceeds before disbursement and is included in your APR calculation. It is fully disclosed before you accept any loan offer.

Related Upstart Guides

Disclaimer: Rates and terms are accurate as of May 2026. WiseIQ is not a lender. All loan decisions are made by Upstart's partner banks. Check your rate directly with Upstart for personalised terms.