When seeking a personal loan with a 680 credit score, you're positioned as a near-prime borrower, which opens up a wider array of lending options compared to those with lower scores. A 680 FICO score typically falls within the 'Good' credit range, signifying a responsible credit history and making you an attractive candidate for many lenders. This guide will explore the best personal loan options available for individuals with a 680 credit score, detailing what to expect in terms of interest rates, approval odds, and key factors to consider when applying.

Expert Tip

Always prequalify with multiple lenders. This process involves a soft credit pull, which won't impact your credit score, and allows you to compare potential loan offers, including estimated APRs and loan terms, without commitment. This is crucial for finding the most favorable terms for your personal loan.

Understanding Your 680 Credit Score and Loan Eligibility

A 680 credit score is often considered the good credit threshold, indicating that you manage your finances responsibly. Lenders view this score favorably, suggesting a lower risk of default. However, while a 680 score improves your approval odds, lenders will also evaluate other aspects of your financial profile. Key factors include your debt-to-income ratio, which measures your monthly debt payments against your gross monthly income, and your credit utilization, which is the amount of revolving credit you're using compared to your total available credit. Keeping these ratios healthy can further strengthen your application.

How to Secure the Best Personal Loan with a 680 Credit Score

-

Check Your Credit Report:

Before applying, obtain a copy of your credit report from all three major bureaus (Equifax, Experian, and TransUnion). Review it for any errors or inaccuracies that could be negatively impacting your score. Disputing and correcting these can potentially boost your score further.

-

Calculate Your Debt-to-Income Ratio:

Lenders use your debt-to-income (DTI) ratio to assess your ability to manage monthly payments. A lower DTI indicates less risk. Aim for a DTI below 36%, though some lenders may approve higher ratios depending on other factors.

-

Prequalify with Multiple Lenders:

As mentioned, prequalification is a powerful tool. It allows you to see potential loan offers, including the annual percentage rate (APR), loan term, and estimated monthly payment, without affecting your credit score. This is a soft credit pull and is highly recommended.

-

Compare Loan Offers:

Don't settle for the first offer. Compare interest rates, origination fees, repayment schedules, and any prepayment penalties across different lenders. Look for transparent terms and competitive rates.

-

Gather Necessary Documentation:

Once you choose a lender, you'll need to provide documentation such as proof of income, identification, and bank statements. Having these ready can expedite the application process.

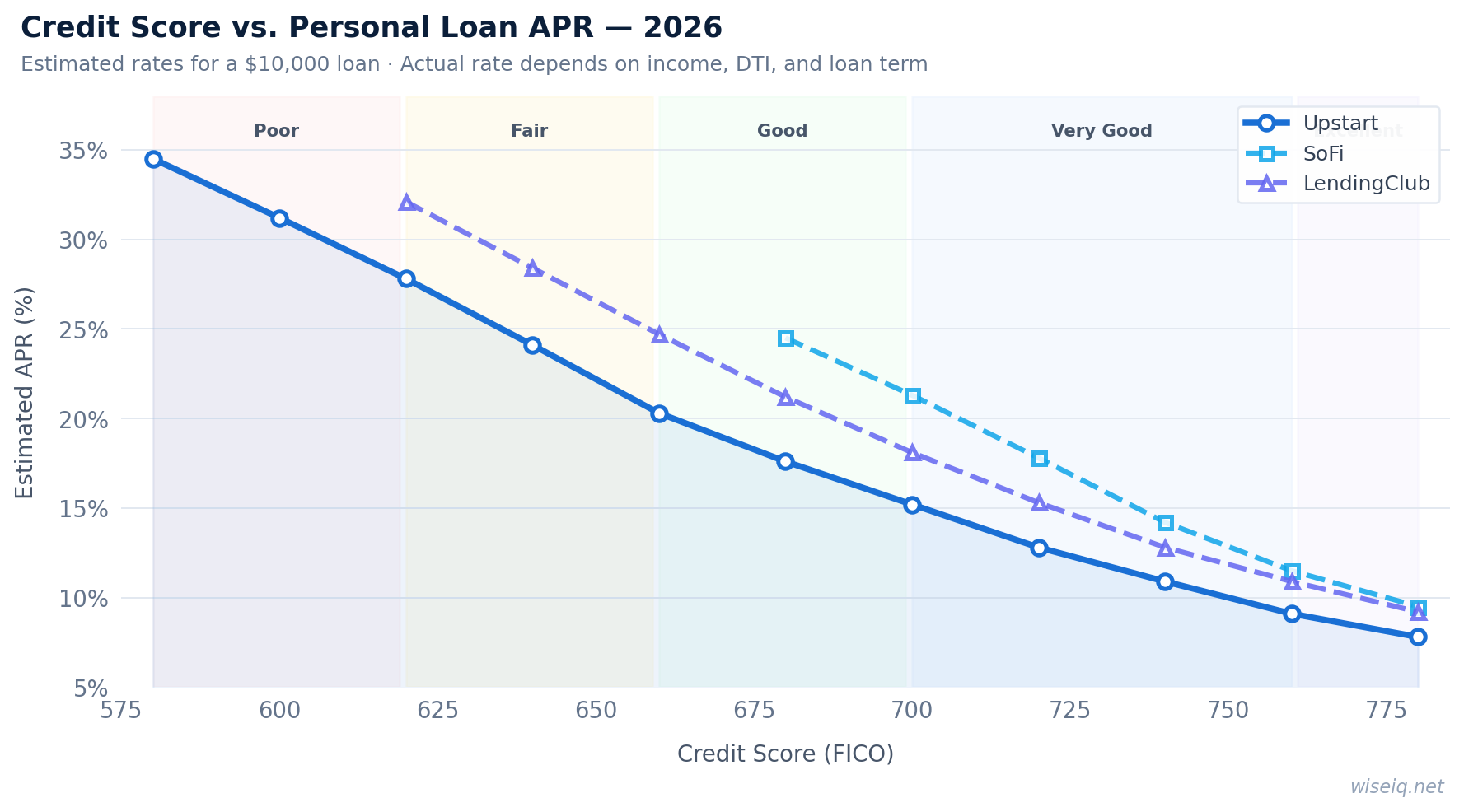

Top Lenders for a Personal Loan with a 680 Credit Score

Several lenders are known for offering competitive personal loans to borrowers with a 680 credit score. Here’s a look at some of the best options and what they offer:

| Lender | APR From | Loan Amount Range | Key Features |

|---|---|---|---|

| Upstart | 6.40% | $1,000 - $50,000 | AI underwriting, education-based lending, no prepayment penalty, next-day funding. |

| SoFi | 8.99% | $5,000 - $100,000 | No origination fees, unemployment protection, career support. |

| Marcus by Goldman Sachs | 6.99% | $3,500 - $40,000 | No fees, personalized payment options, on-time payment reward. |

| LightStream | 7.49% | $5,000 - $100,000 | Excellent credit required for lowest rates, no fees, rate beat program. |

| Payoff (by Happy Money) | 5.99% | $5,000 - $40,000 | Focus on credit card consolidation, direct payment to creditors, no late fees. |

Rates verified May 2026

Frequently Asked Questions

What is a good credit score for a personal loan?

Generally, a FICO score of 670 or higher is considered good. With a 680 credit score, you are in a favorable position to qualify for personal loans with competitive interest rates and terms.

Can I get a personal loan with a 680 credit score with no origination fee?

While many lenders charge an origination fee, some lenders offer personal loans with no origination fees, especially to borrowers with good credit scores like 680. It's important to compare offers from various lenders to find one that best suits your needs.

How does a soft credit pull affect my credit score?

A soft credit pull, often used for prequalification, does not affect your credit score. It allows lenders to review your creditworthiness without leaving a mark on your credit report. A hard credit inquiry, however, occurs when you formally apply for a loan and can temporarily lower your score by a few points.

What is the average APR for a personal loan with a 680 credit score?

The average APR for a personal loan with a 680 credit score can vary widely depending on the lender, loan term, and your overall financial profile. However, borrowers with a 680 score can typically expect APRs ranging from 6% to 25%. Prequalifying with multiple lenders will give you a clearer idea of the rates you qualify for.

What is debt-to-income ratio and why is it important?

Your debt-to-income (DTI) ratio is a percentage that compares your total monthly debt payments to your gross monthly income. Lenders use DTI to assess your ability to manage monthly payments and take on additional debt. A lower DTI indicates less risk and can improve your chances of loan approval and securing better terms.

How can I improve my 680 credit score further?

To improve your 680 credit score, focus on making all payments on time, keeping your credit utilization low (ideally below 30%), and avoiding opening too many new credit accounts at once. Regularly checking your credit report for errors and disputing them can also help.

Are there alternatives to personal loans for a 680 credit score?

Yes, alternatives include balance transfer credit cards (if you have high-interest credit card debt), home equity loans or lines of credit (if you own a home), or borrowing from friends or family. Each option has its own pros and cons, so consider your financial situation carefully.

Related Guides

- Upstart Review 2026

- Best Personal Loans 2026

- Personal Loan 660 Credit Score

- Personal Loan Rates by Credit Score

- Upstart Loan 700 Credit Score

- Personal Loans for Bad Credit

Disclaimer: The information provided on this page is for informational purposes only and does not constitute financial advice. Please consult with a qualified financial professional before making any financial decisions.