A personal loan 660 credit score is within reach for many borrowers. While a 660 FICO score is considered 'fair,' it opens doors to various lending options that might not be available to those with lower scores. Lenders assess more than just your credit score; they also consider your debt-to-income ratio, employment history, and other financial indicators. Understanding these factors can significantly improve your approval odds and help you secure a favorable annual percentage rate (APR). This comprehensive guide will help you navigate the process, compare top lenders, and make an informed decision about your next personal loan.

Expert Tip: Always prequalification with multiple lenders. This allows you to see potential loan offers and estimated annual percentage rates (APR) without undergoing a hard credit inquiry, which can temporarily affect your FICO score. It's a smart way to compare options and find the best loan term for your financial situation.

Understanding Your 660 Credit Score and Loan Options

A 660 credit score places you in the fair credit category, which means you're seen as a moderate risk by lenders. While you might not qualify for the absolute lowest interest rates, you're far from being a subprime borrower. Many reputable lenders are willing to work with individuals with a 660 credit score, especially if other aspects of your financial profile are strong. These can include a stable employment history, a manageable debt-to-income ratio, and a consistent payment history on existing debts. It's important to remember that every lender has its own underwriting criteria, and some may be more flexible than others, particularly those that utilize non-traditional underwriting methods.

When seeking a personal loan 660 credit score, you'll encounter various types of lenders, including traditional banks, credit unions, and online lenders. Online lenders, such as Upstart, SoFi, and LendingClub, often specialize in serving borrowers across a wider credit spectrum and may offer more competitive rates or flexible terms for fair credit personal loan applicants. They frequently use alternative credit data and AI underwriting to assess creditworthiness beyond just your FICO score, which can be a significant advantage for near-prime borrowers.

Top Lenders for a Personal Loan with a 660 Credit Score

Finding the right lender is crucial when you have a 660 credit score. Here are some of the top options that often cater to fair credit borrowers:

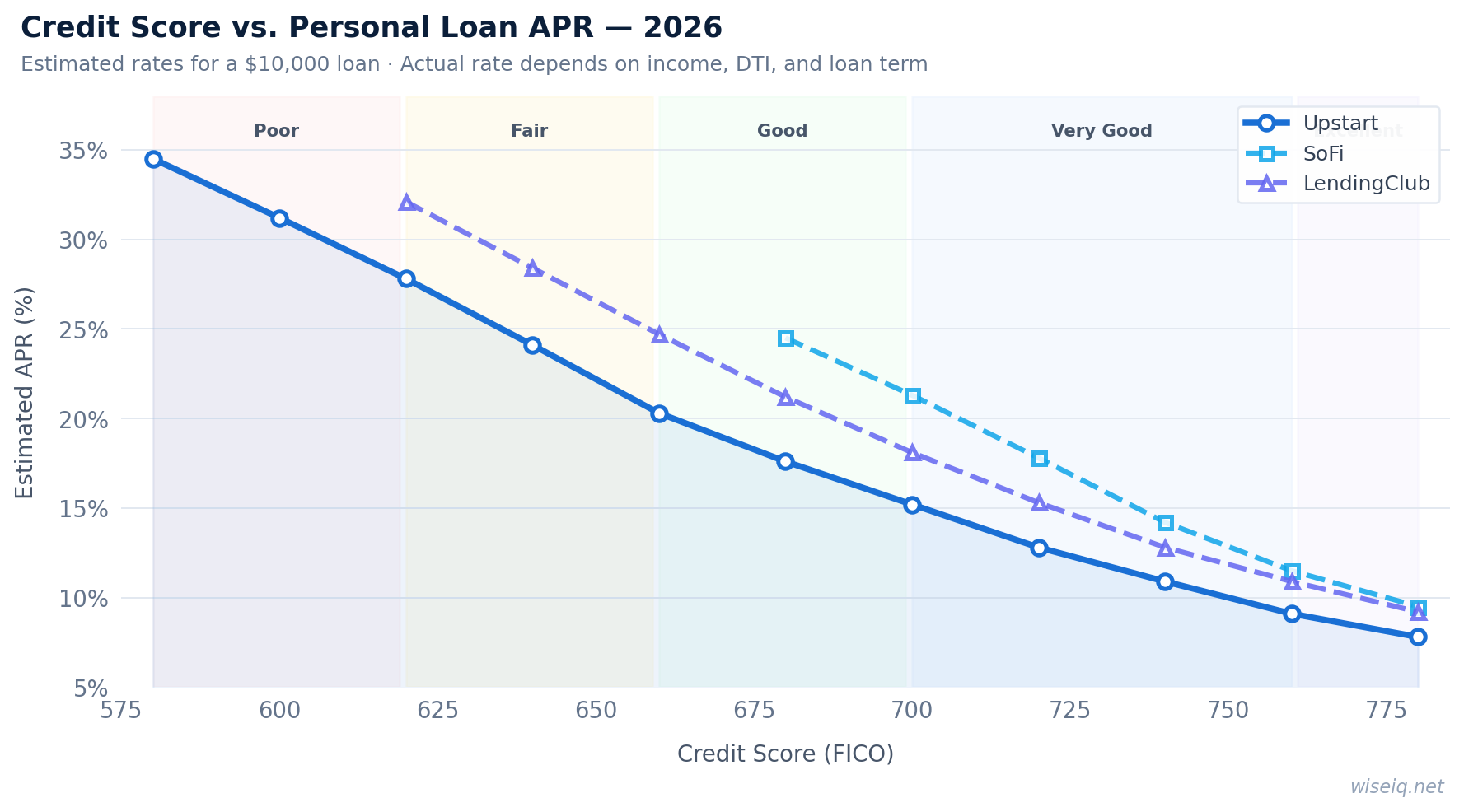

Upstart: AI-Powered Lending for Fair Credit

Upstart stands out for its innovative approach to lending. Instead of relying solely on traditional credit scores, Upstart uses AI underwriting to consider factors like your education, area of study, and employment history. This can significantly improve approval odds for individuals with a 660 FICO score who might be overlooked by conventional lenders. Upstart offers competitive annual percentage rates (APR) and often provides next-day funding, making it a strong contender for those needing quick access to funds. They also boast no prepayment penalty, offering flexibility if you wish to pay off your loan early.

- AI underwriting: Considers more than just your credit score.

- Education-based lending: Factors in your academic and professional background.

- No prepayment penalty: Pay off your loan early without extra fees.

- Next-day funding: Quick access to approved funds.

- APR range: 6.40%–35.99% (as of May 2026).

SoFi: Comprehensive Financial Services

SoFi is another popular choice, known for its wide range of financial products, including personal loans. While SoFi often targets borrowers with good to excellent credit, they do consider applicants with fair credit, especially if they have a strong income and low debt-to-income ratio. SoFi offers competitive rates, no origination fee, and various member benefits. Their prequalification process involves a soft credit pull, allowing you to check your estimated rates without affecting your FICO score.

- No origination fee: Save on upfront costs.

- Competitive APRs: Especially for well-qualified borrowers.

- Member benefits: Access to financial planning and career services.

- Soft credit pull: Check rates without impacting your credit score.

- APR from: 8.99% (as of May 2026).

LendingClub: Peer-to-Peer Lending Pioneer

LendingClub was one of the first peer-to-peer lending platforms and remains a strong option for fair credit borrowers. They connect borrowers with investors, often resulting in more flexible underwriting criteria. While they do charge an origination fee, their rates can be competitive, and they offer a clear loan term structure. LendingClub's focus on a broader range of credit profiles makes it a viable option for those with a 660 credit score looking for a personal loan.

- Peer-to-peer model: Connects borrowers with individual investors.

- Flexible underwriting: May be more lenient than traditional banks.

- Origination fee: Typically 1% to 6% of the loan amount.

- APR from: 9.57% (as of May 2026).

How to Secure the Best Personal Loan with a 660 Credit Score

Even with a 660 credit score, there are steps you can take to improve your chances of approval and secure a lower annual percentage rate (APR). Here's how:

1. Prequalify with Multiple Lenders

As mentioned in our expert tip, prequalification is your best friend. Most online lenders offer a prequalification process that involves a soft credit pull. This allows you to see estimated rates and terms without any impact on your FICO score. By comparing offers from several lenders, you can identify the one that provides the most favorable loan term and monthly payment for your financial situation. Don't limit yourself to just one or two options; explore as many as possible.

2. Improve Your Debt-to-Income Ratio

Your debt-to-income ratio (DTI) is a critical factor for lenders. It's the percentage of your gross monthly income that goes towards debt payments. A lower DTI indicates that you have more disposable income to cover new loan payments, making you a less risky borrower. Before applying, try to pay down some existing debts, especially high-interest credit card balances, to improve your DTI.

3. Highlight Stable Employment and Income

Lenders want to see that you have a consistent and reliable source of income. If you've been at your current job for a significant period, or if you have a strong employment history, make sure to emphasize this in your application. Stable income demonstrates your ability to make regular monthly payments, which can significantly boost your approval odds, even with a fair credit personal loan.

4. Consider a Co-signer (If Applicable)

If you're struggling to get approved or want to secure a lower APR, a co-signer with excellent credit can be a game-changer. A co-signer adds their creditworthiness to your application, reducing the lender's risk. This can lead to better terms and a higher chance of approval for a personal loan 660 credit score.

What to Watch Out For: Origination Fees and Prepayment Penalties

When evaluating personal loan offers, it's essential to look beyond just the advertised APR. Two common fees that can impact the total cost of your loan are origination fees and prepayment penalties.

- Origination Fee: This is an upfront fee charged by the lender for processing your loan. It's typically a percentage of the loan amount (e.g., 1% to 6%) and is often deducted from your loan proceeds before you receive the funds. Always factor this into your total loan cost.

- Prepayment Penalty: Some lenders charge a fee if you pay off your loan early. While many modern lenders, like Upstart, have no prepayment penalty, it's crucial to check the loan agreement to avoid unexpected costs if you plan to accelerate your payments.

Comparing Personal Loan Offers: A Data-Driven Approach

To illustrate how different lenders might compare for a borrower with a 660 credit score, let's look at a hypothetical scenario. Remember that these are illustrative rates and your actual annual percentage rate (APR) will depend on your specific financial profile and the lender's underwriting criteria. Always use prequalification to get personalized offers.

Hypothetical Loan Comparison for a 660 Credit Score

| Lender | Starting APR | Loan Amounts | Origination Fee | Key Feature for 660 Score |

|---|---|---|---|---|

| Upstart | 6.40% | $1,000 - $50,000 | 0% - 12% | AI underwriting, education-based lending |

| SoFi | 8.99% | $5,000 - $100,000 | 0% | No fees, strong income focus |

| LendingClub | 9.57% | $1,000 - $40,000 | 1% - 6% | Peer-to-peer model, flexible criteria |

Rates verified May 2026. Actual rates and terms may vary based on creditworthiness and other factors.

Eligibility and Requirements for a 660 Credit Score Personal Loan

While a 660 credit score is a good starting point, lenders look at a holistic view of your financial health. Here are the typical eligibility criteria and requirements you'll encounter:

- Credit Score: A FICO score of 660 falls into the fair credit range. Lenders will assess your credit history for any negative marks, such as late payments or bankruptcies.

- Income: You'll need to demonstrate a stable and verifiable source of income. Lenders want to ensure you have the capacity to repay the loan.

- Debt-to-Income Ratio (DTI): Your DTI is crucial. A lower ratio indicates less financial strain and a greater ability to handle new debt.

- Employment History: A consistent employment history shows stability. Lenders prefer to see at least a year or two at your current job, or a strong track record in your career field.

- Bank Account: You'll need an active checking account for funds disbursement and monthly payment setup.

- Age and Residency: You must be at least 18 years old and a U.S. citizen or permanent resident.

Some lenders, like Upstart, may also consider non-traditional credit factors, such as your educational background and job history, to provide a more comprehensive assessment of your creditworthiness. This can be particularly beneficial for those with a limited credit history or a fair credit score.

Alternatives to a Traditional Personal Loan for Fair Credit

If a traditional personal loan doesn't quite fit your needs, or if you're looking for other ways to manage your finances with a 660 credit score, consider these alternatives:

- Secured Personal Loans: These loans require collateral, such as a car or savings account. Because the loan is secured, lenders perceive less risk, often leading to lower interest rates and more favorable terms, even for fair credit borrowers.

- Credit Builder Loans: Designed specifically to help you build credit, these loans typically place the loan amount into a locked savings account. As you make payments, your credit score improves, and you gain access to the funds.

- Home Equity Loans or HELOCs: If you're a homeowner, you might be able to tap into your home equity. These often come with lower interest rates due to being secured by your home, but they also carry the risk of foreclosure if you default.

- Borrowing from Friends or Family: While not a formal financial product, this can be a viable option if you have trusted individuals willing to lend you money. Ensure you have a clear repayment agreement to avoid straining relationships.

Related Guides to Help Your Financial Journey

Explore more resources from WiseIQ to help you make informed financial decisions:

- Upstart Review 2026: A deep dive into Upstart's lending model and offerings.

- Best Personal Loans 2026: Our comprehensive guide to top personal loan providers.

- Personal Loan 640 Credit Score: Options for those with a slightly lower fair credit score.

- Personal Loan 680 Credit Score: Exploring opportunities for improving credit profiles.

- Upstart for Debt Consolidation: How Upstart can help you manage and consolidate debt.

- Personal Loan Calculator: Estimate your monthly payments and total interest.

WiseIQ Editorial Team

The WiseIQ Editorial Team is dedicated to providing accurate, unbiased, and actionable financial advice to help you make smarter money decisions. Our content is thoroughly researched and reviewed by financial experts.

Frequently Asked Questions About 660 Credit Score Personal Loans

Can I get a personal loan with a 660 credit score?

Yes, a 660 credit score is generally considered fair credit, and many lenders offer personal loans to borrowers in this range. While you might not qualify for the absolute lowest annual percentage rates (APR), you still have good options. Lenders will also consider other factors like your debt-to-income ratio and employment history.

What is a good interest rate for a 660 credit score personal loan?

For a 660 credit score, expected APR range can vary significantly, but you might see rates starting from around 8% to 15% or higher, depending on the lender, loan term, and your overall financial profile. It's crucial to prequalification with multiple lenders to compare offers without impacting your credit score with a hard credit inquiry.

Which lenders are best for a 660 credit score?

Lenders like Upstart, SoFi, and LendingClub are often good options for borrowers with fair credit. Upstart, in particular, uses AI underwriting and considers non-traditional credit factors, which can be beneficial for those with a 660 FICO score. Always compare offers to find the best loan term and monthly payment for your needs.

What factors do lenders consider besides my 660 credit score?

Beyond your FICO score, lenders evaluate your debt-to-income ratio, employment history, income stability, and other non-traditional credit factors. Some lenders, like Upstart, use AI underwriting to get a more holistic view of your financial health, potentially improving your approval odds even with a fair credit personal loan.

How can I improve my approval odds for a personal loan with a 660 credit score?

To improve your approval odds, focus on reducing your debt-to-income ratio, ensuring stable employment, and making all payments on time to boost your credit building efforts. Prequalification with several lenders allows you to see potential offers without a hard credit inquiry, helping you choose the best fair credit personal loan.

What is the difference between a soft credit pull and a hard credit inquiry?

A soft credit pull is a preliminary check that doesn't affect your credit score and is often used for prequalification. A hard credit inquiry, on the other hand, occurs when you formally apply for a loan and can temporarily lower your FICO score. It's wise to use soft credit pulls to compare offers before committing to a full application.

More Personal Loan Guides

Disclaimer: The information provided on this page is for informational purposes only and does not constitute financial advice. WiseIQ strives to keep information accurate and up-to-date, but rates and terms are subject to change. Always review the lender's terms and conditions before making any financial decisions. Your actual annual percentage rate (APR) will depend on your credit score, loan amount, loan term, and other factors.