For many individuals, securing a personal loan with a 660 credit score can feel like an uphill battle. Traditional lenders often rely heavily on your FICO score, which can limit options for those with fair credit. However, Upstart has revolutionized the lending landscape with its innovative AI underwriting model. This approach allows them to assess a broader range of factors beyond just your credit history, including your education, employment history, and income potential. If you're wondering, "Can I get an Upstart loan with a 660 credit score?", the answer is often yes, and this guide will walk you through how.

Upstart’s unique methodology means that even if you’re considered a near-prime borrower by conventional standards, you might still qualify for favorable terms. They aim to provide access to affordable credit for a wider population, focusing on your future potential rather than solely your past financial behavior. This can be a game-changer for those looking for a fair credit personal loan to consolidate debt, cover unexpected expenses, or fund a significant purchase.

Expert Tip: Boost Your Approval Odds

Even with a 660 credit score, you can improve your approval odds by ensuring your debt-to-income ratio is low, you have a stable employment history, and you clearly articulate the purpose of your loan. Consider using Upstart's prequalification tool to see your estimated rates without a hard credit inquiry.

How Upstart's AI Underwriting Works for a 660 Credit Score

Upstart’s distinctive lending model is built on the premise that a credit score alone doesn’t tell the whole story of a borrower’s creditworthiness. For someone with a 660 credit score, this is particularly beneficial. Instead of solely relying on traditional metrics, Upstart leverages advanced machine learning to analyze over 1,600 data points. These include:

- Education-based lending: Your academic background, including the university you attended and your degree, can positively influence your application.

- Employment history: A stable job with consistent income demonstrates your ability to repay the loan.

- Non-traditional credit factors: Upstart considers factors like rent payments, utility bills, and even your bank transaction history, which might not appear on a standard credit report.

This comprehensive assessment allows Upstart to identify creditworthy individuals who might be overlooked by traditional lenders due to a less-than-perfect FICO score. The result is often a more personalized offer, potentially with a lower annual percentage rate (APR) than you might expect from other lenders for a fair credit personal loan.

Key Benefits of an Upstart Loan with Fair Credit

Choosing Upstart for a personal loan when you have a 660 credit score comes with several distinct advantages:

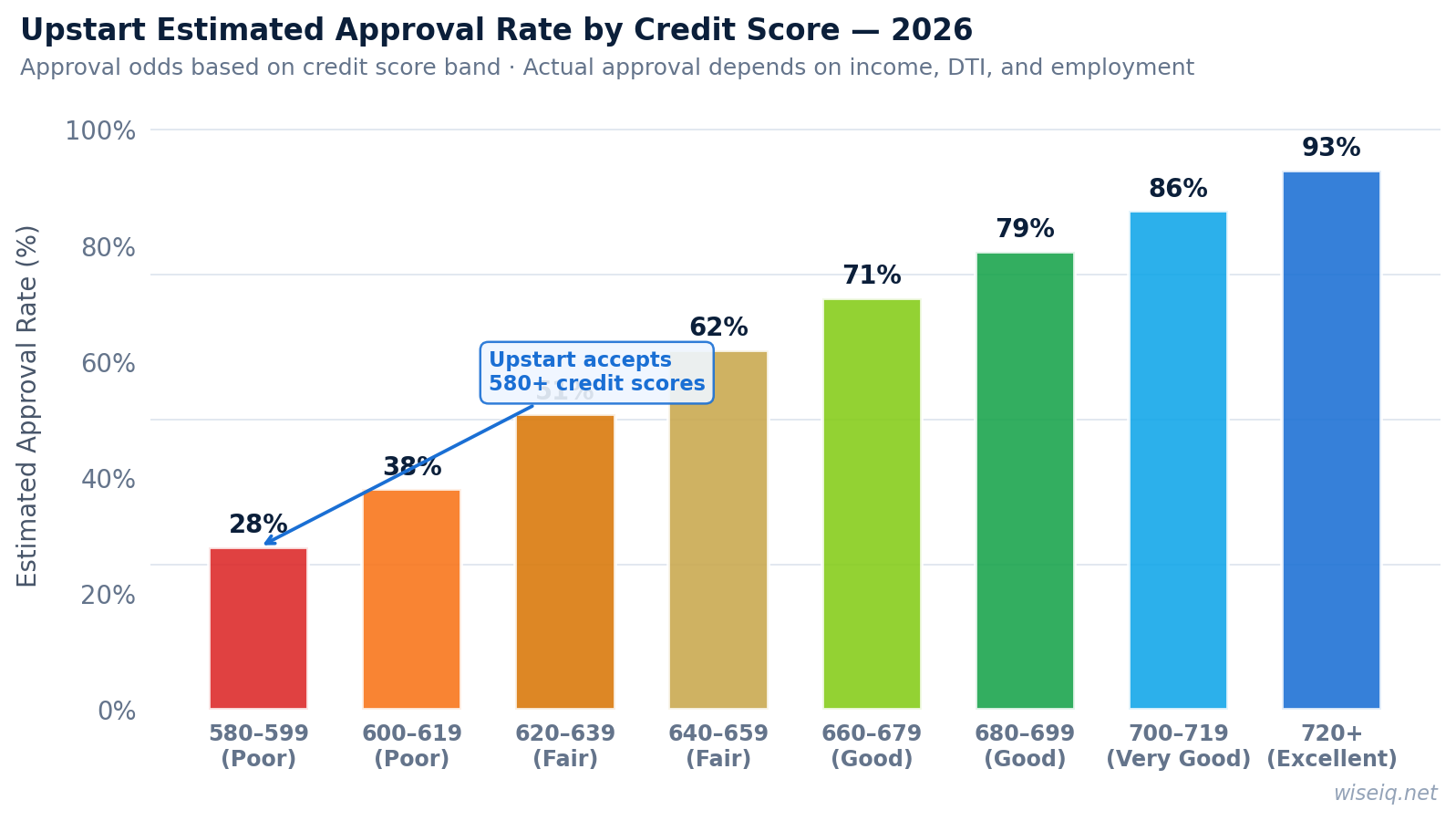

- Higher Approval Rates: Upstart approves 27% more applicants than traditional lenders, often extending offers to those with lower FICO scores.

- Competitive APRs: Despite a fair credit score, Upstart’s AI can identify you as a lower risk, potentially offering an expected APR range that is more favorable than other subprime options.

- Fast Funding: Once approved, many borrowers experience next-day funding, providing quick access to necessary funds.

- No Prepayment Penalty: Upstart does not charge a prepayment penalty, allowing you to save on interest by paying off your loan early.

- Simple Prequalification: You can check your rates with a soft credit pull, which won't impact your 660 credit score. A hard credit inquiry only occurs if you accept a loan offer.

These benefits make Upstart an attractive option for individuals focused on credit building or those who need a personal loan but are constrained by their current credit profile.

Understanding Upstart Loan Rates and Terms

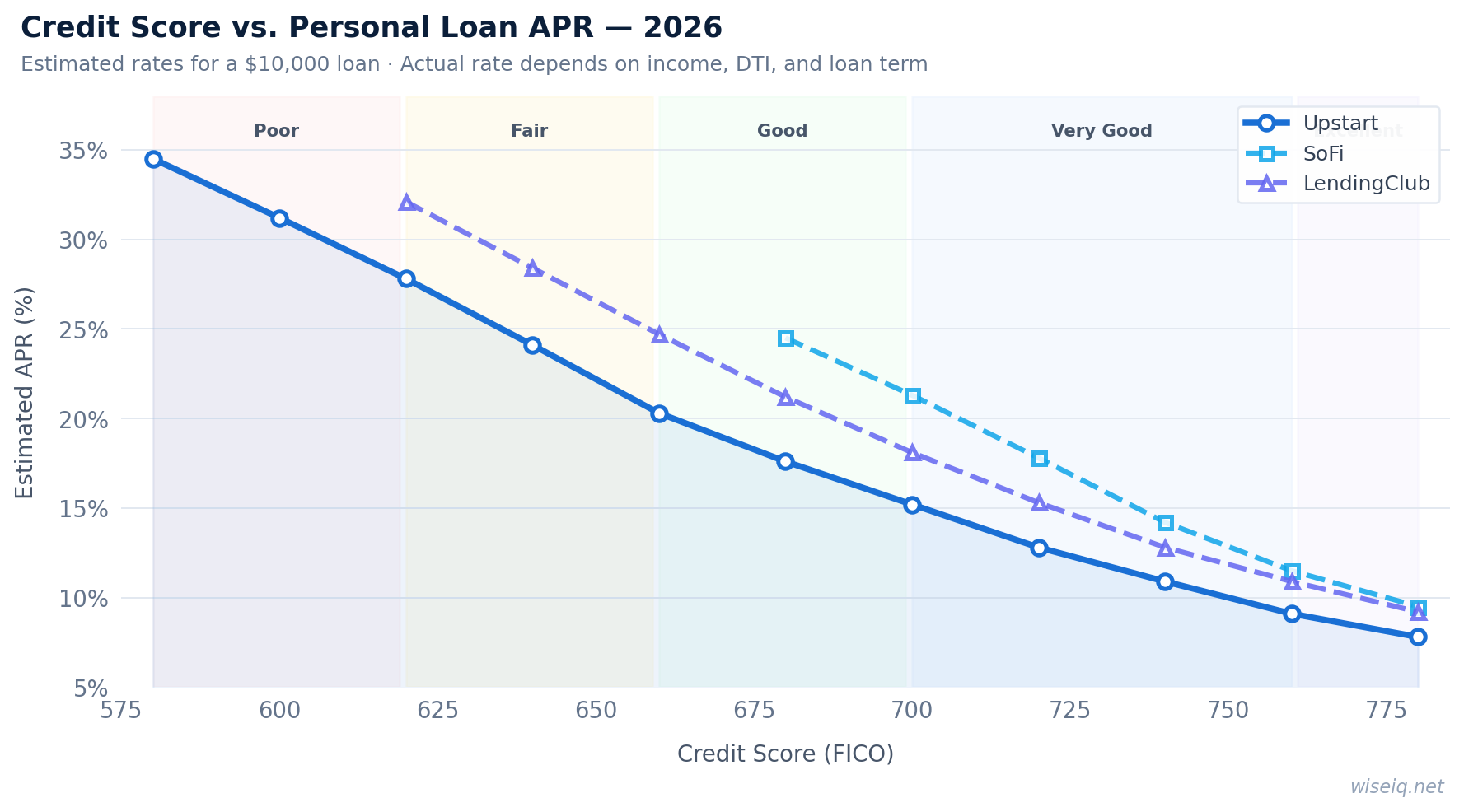

When considering an Upstart loan with a 660 credit score, it s crucial to understand the potential rates and terms. Upstart offers a broad APR range from 6.40% to 35.99%. While a 660 credit score places you in the fair credit category, Upstart's model aims to provide rates that accurately reflect your overall risk, not just your FICO score.

The loan term options are typically 36 or 60 months. Your chosen loan term will influence your monthly payment and the total interest paid over the life of the loan. It's important to balance a manageable monthly payment with the desire to pay off the loan quickly to minimize interest costs. Upstart also charges an origination fee, which can range from 0% to 12% of the loan amount. This fee is deducted from the loan proceeds before you receive them, so factor this into your total borrowing needs.

Upstart Loan Example for a 660 Credit Score

To illustrate, let's consider a hypothetical scenario for a borrower with a 660 credit score:

| Loan Amount | APR (Estimated) | Loan Term | Origination Fee | Monthly Payment (Estimated) | Total Interest Paid (Estimated) |

|---|---|---|---|---|---|

| $15,000 | 18.50% | 36 Months | 5% ($750) | $545 | $4,620 |

| $15,000 | 19.00% | 60 Months | 5% ($750) | $390 | $8,400 |

Rates verified May 2026. These are illustrative examples; your actual rates and terms may vary based on your specific financial profile.

Eligibility and Requirements for Upstart Loans

While a 660 credit score is a good starting point, Upstart considers several other factors for eligibility. To qualify for an Upstart personal loan, you generally need to meet the following criteria:

- Be at least 18 years old (19 in Alabama and Nebraska).

- Be a U.S. citizen or permanent resident.

- Have a valid email address.

- Have a verifiable full-time job or a full-time job offer starting within six months, or a regular part-time job, or other source of regular income.

- Have a U.S. bank account.

- Have a minimum FICO score of 300 (or no FICO score if Upstart can verify your income and employment through other means). Note that while a 300 FICO is the minimum, a 660 credit score significantly improves your chances.

- Not have any bankruptcies or public records on your credit report.

Upstart's emphasis on non-traditional underwriting means that even if your credit history is thin or you're a subprime borrower according to traditional models, your educational attainment and stable employment can play a significant role in your approval. This makes Upstart particularly appealing for recent graduates or those who are new to credit.

Comparing Upstart with Other Lenders for a 660 Credit Score

When you have a 660 credit score, finding the right personal loan can involve comparing various lenders. Traditional banks and credit unions often have stricter credit score requirements, making it difficult for fair credit borrowers to qualify for competitive rates. Online lenders, like Upstart, have emerged as strong alternatives due to their more flexible underwriting models.

Upstart's focus on AI underwriting and alternative credit data sets it apart. While other lenders might offer loans to fair credit borrowers, their rates could be higher, or they might require a co-signer. Upstart's ability to assess your future earning potential and stability can result in a more favorable expected APR range and better overall loan terms.

Alternatives to Consider

If Upstart doesn't fit your needs, or you want to explore all your options, consider these alternatives:

- Credit Unions: Often offer more personalized service and may be more willing to work with members who have fair credit.

- Other Online Lenders: Many online lenders specialize in fair or bad credit loans, but always compare their APRs, fees, and terms carefully.

- Secured Personal Loans: If you have collateral, a secured loan can offer lower interest rates, but you risk losing the asset if you default.

Always perform a prequalification with multiple lenders to compare offers without impacting your credit score. This allows you to see the actual rates and terms you might receive before committing to a hard credit inquiry.

Maximizing Your Approval Odds and Getting the Best Rates

Even with a 660 credit score, there are steps you can take to improve your chances of approval and secure the most favorable terms on an Upstart loan:

- Improve Your Credit Utilization: Lowering your credit utilization ratio (the amount of credit you're using compared to your total available credit) can positively impact your credit score.

- Reduce Your Debt-to-Income Ratio: A lower debt-to-income ratio indicates that you have more disposable income to put towards loan payments, making you a less risky borrower.

- Ensure Accurate Application Information: Double-check all information on your application to avoid delays or denials due to errors.

- Highlight Your Education and Employment: Since Upstart values these factors, ensure your application clearly reflects your educational achievements and stable employment history.

- Prequalify First: Always use Upstart's prequalification tool to get an idea of your potential rates and terms before a full application. This is a soft credit pull and won't harm your credit score.

By proactively managing these aspects of your financial profile, you can present yourself as a more attractive borrower to Upstart and potentially unlock better loan offers, even with a 660 credit score.

Frequently Asked Questions About Upstart Loans with a 660 Credit Score

Is a 660 credit score good enough for an Upstart loan?

Yes, a 660 credit score is often considered 'fair' credit, and Upstart is known for its inclusive lending model. While traditional lenders might be hesitant, Upstart's AI underwriting considers more than just your FICO score, including your education, employment history, and other non-traditional credit factors. This approach can significantly improve your approval odds even with a 660 credit score.

What is the typical APR range for an Upstart loan with a 660 credit score?

Upstart's APRs range from 6.40% to 35.99%. For borrowers with a 660 credit score, the expected APR range might be on the higher end compared to those with excellent credit, but still competitive given the risk profile. The exact annual percentage rate you receive will depend on your overall financial profile, including your debt-to-income ratio, loan term, and the results of your prequalification.

How does Upstart's AI underwriting help borrowers with a 660 credit score?

Upstart's AI underwriting model goes beyond traditional credit scores. It analyzes thousands of data points, including your education, area of study, employment history, and income potential. For individuals with a 660 credit score, this means that positive aspects of their financial and educational background can offset a less-than-perfect credit score, potentially leading to approval and better rates than they might find elsewhere.

What documents do I need to apply for an Upstart loan with a 660 credit score?

Typically, you'll need to provide proof of identity (government-issued ID), proof of income (pay stubs, bank statements), and details about your education and employment. While a 660 credit score is acceptable, having all your documentation ready can streamline the application process and help Upstart assess your financial stability more accurately.

Can I prequalify for an Upstart loan without affecting my 660 credit score?

Yes, Upstart offers a prequalification process that involves a soft credit pull. This allows you to check your potential rates and loan options without impacting your 660 credit score. A hard credit inquiry is only performed if you proceed with a full application after reviewing your offers.

What are the loan terms available for Upstart loans?

Upstart typically offers loan terms of 3 or 5 years (36 or 60 months). The specific loan term you qualify for will depend on your creditworthiness and the loan amount. Longer terms generally result in lower monthly payments but higher overall interest paid.

Does Upstart charge an origination fee?

Yes, Upstart charges an origination fee that ranges from 0% to 12% of the loan amount. This fee is deducted from your loan proceeds before they are disbursed. The exact origination fee depends on your credit profile and the terms of your loan offer.

Disclaimer: The information provided on this page is for informational purposes only and does not constitute financial advice. Always consult with a qualified financial professional before making any financial decisions. Loan approval and actual rates depend on your creditworthiness and other factors.