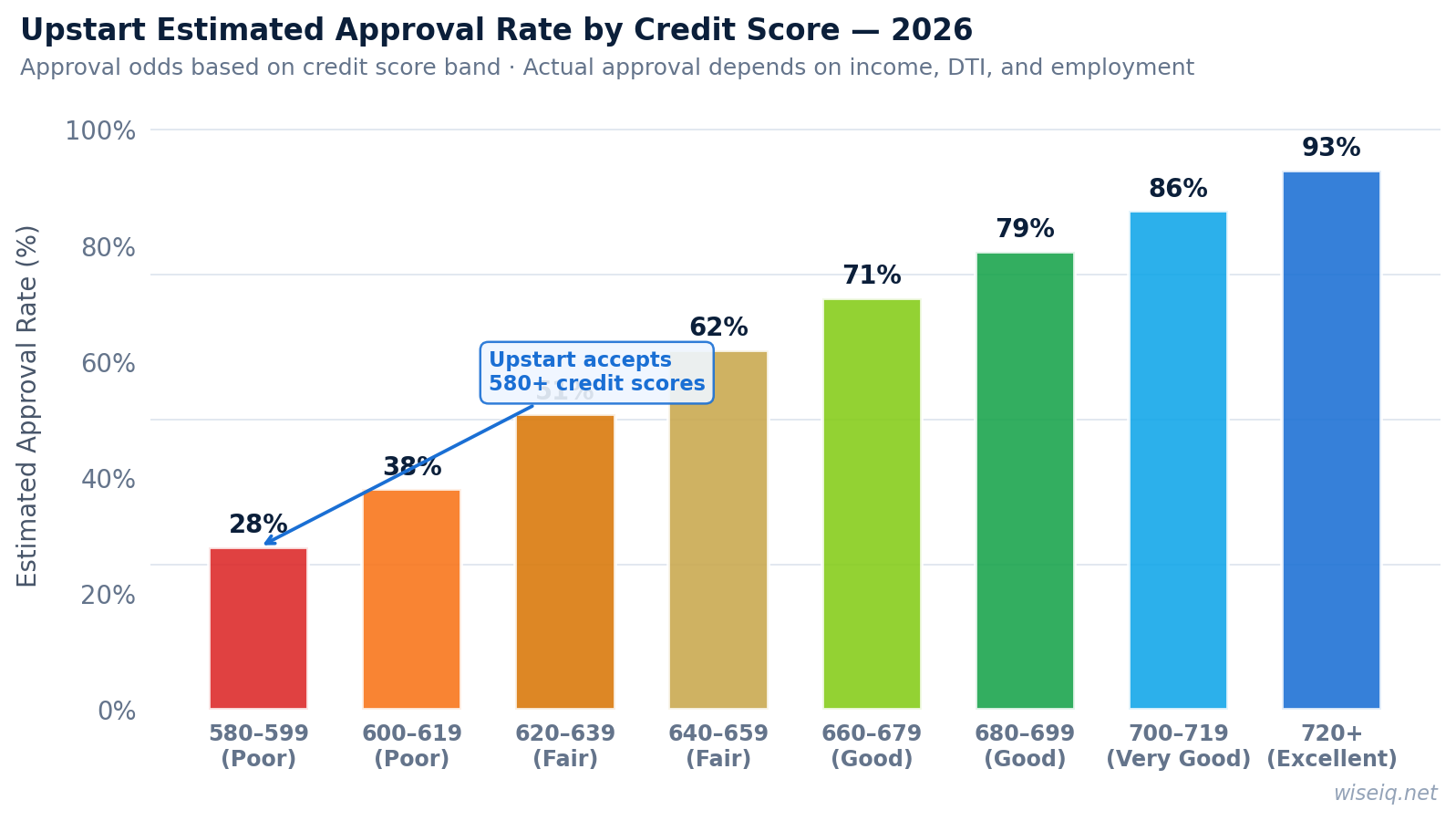

Important: Upstart Requires a Minimum 580 Credit Score

Despite the name of this page, Upstart is not a lender for scores below 580. Their AI model considers education and employment history, but the hard floor is 580. If your score is currently below that, applying will result in a decline.

Upstart is the right choice if your score is 580–740 — especially if you have a thin credit file, are a recent graduate, or have steady income but an imperfect history. If you're below 580, the options below are more likely to approve you.

Upstart personal loans are designed for borrowers with bad credit or no credit history. No minimum credit score — AI-based approval considers your full financial picture.

6.20%Starting APR

$1,000 – $50,000Typical Loan Range

1 DayTime to Fund

Advertiser Disclosure: WiseIQ is reader-supported. When you apply through links on this page, we may earn a commission at no extra cost to you. Learn more.

Having bad credit doesn't mean you can't get a personal loan — it means you need to find the right lender. Upstart is one of the few legitimate lenders with no minimum credit score requirement. Their AI-based underwriting model looks beyond your credit score to consider your education, employment history, and income.

WiseIQ Expert Tip

Financial decisions made with complete information consistently outperform those made under pressure or with incomplete data. Take time to compare at least 3 options before committing.

What "Bad Credit" Means for Upstart

Rates verified May 2026 · Updated weekly

Credit Score Range

Category

Upstart Eligibility

300 – 579

Poor / Bad

✅ May qualify

580 – 619

Fair

✅ Good odds

620 – 659

Fair / Near Prime

✅ Strong odds

660 – 719

Good

✅ Very likely

720+

Very Good / Excellent

✅ Best rates

No credit history

Thin file

✅ May qualify

Upstart Approval Rate by Credit Score: Estimated approval odds across credit score bands. Actual approval depends on income, DTI, and employment history.

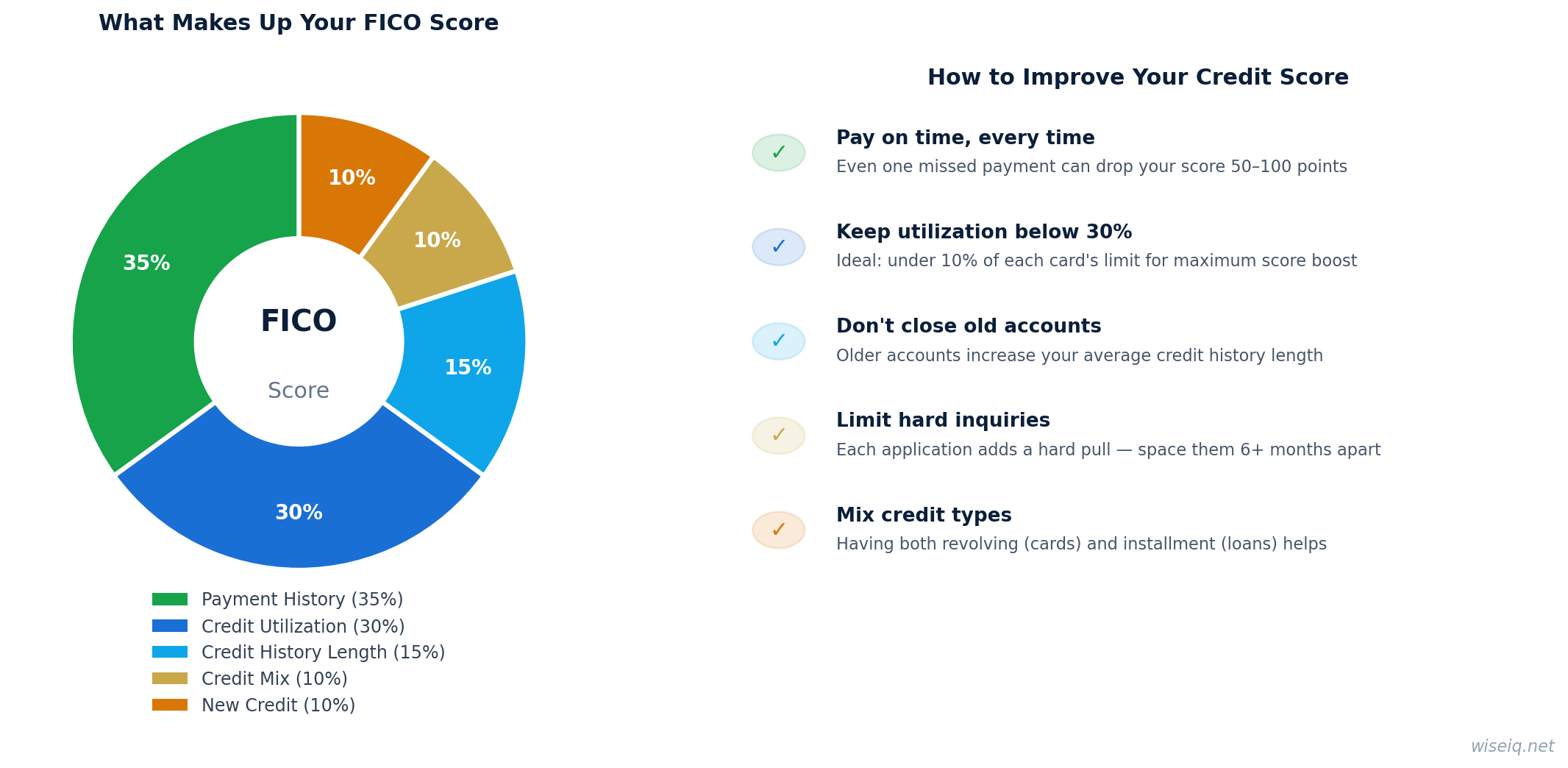

What Makes Up Your FICO Score: Payment history (35%) and credit utilization (30%) are the two most impactful factors.

How Upstart Evaluates Bad Credit Borrowers

Upstart's AI model considers over 1,000 data points beyond your credit score, including:

{"".join([f'

{item}

' for item in ["Education level & field of study", "Employment history & job stability", "Income & income potential", "Area of residence", "Debt-to-income ratio", "Savings & financial behavior"]])}

✅

Who Upstart Is Best For

Credit Score

580 – 740+

Fair to good credit accepted

Min. Income

$12,000/yr

Employment or regular income

Loan Amount

$1,000 – $50,000

Personal loans only

Best For

Thin credit files

Education & job history count

⚠️ Not a fit if: you need a secured loan, have a bankruptcy in the last 12 months, or need more than $50,000.

🔍

What Happens When You Click — 3 Steps

1

2-minute rate check — no hard pull

Upstart runs a soft credit inquiry only. Your score is not affected. You'll see your personalised APR and loan options immediately.

2

Review your offer and accept

Compare loan terms, pick your repayment period (3 or 5 years), and accept. Only at this point does Upstart run a hard pull.

3

Funds in as fast as 1 business day

Most borrowers receive funds within 1–3 business days after final approval. Direct deposit to your bank account.

Upstart offers prequalification with a soft credit pull — meaning you can check your rate in minutes without any impact to your credit score. Before applying, review your debt-to-income ratio (DTI): Upstart looks for a DTI below 45–50%. Divide your total monthly debt payments by your gross monthly income to calculate yours. A lower DTI improves your approval odds and typically results in a lower APR.

🎯

Not sure which option is right for you?

Answer 3 quick questions and get a personalized recommendation in seconds.

We monitor rates across 50+ lenders and alert you when better options become available for your profile.

No spam. Unsubscribe anytime. We never sell your data.

W

WiseIQ Editorial Team

Reviewed by Certified Financial Planners & Industry Experts

Our editorial team consists of financial writers, CFPs, and former banking professionals dedicated to providing accurate, unbiased financial guidance. All content is fact-checked and updated regularly. Learn about our editorial standards →

Frequently Asked Questions

What is the minimum credit score for Upstart? +

Upstart has no official minimum credit score requirement. They use AI-based underwriting that considers your education, employment history, and income in addition to your credit profile.

Can I get an Upstart loan with a 500 credit score? +

Upstart does not publish a hard minimum, but borrowers with scores as low as 300 have been approved. Your approval odds and rate depend on your full financial profile, not just your credit score.

What APR can I expect with bad credit? +

Borrowers with lower credit scores typically receive higher APRs. Upstart's range is 6.20% to 35.99%. Borrowers with bad credit should expect rates in the 25–35% range, though your education and employment history can help lower your rate.

Will applying for an Upstart loan hurt my credit score? +

Checking your rate causes only a soft pull (no impact). Submitting a full application causes a hard pull, which may temporarily lower your score by a few points.

What can I do to improve my chances of approval? +

To improve your approval odds: provide accurate income information, include all sources of income, have a stable employment history, and keep your debt-to-income ratio below 50%.

WiseIQ may earn a referral fee from some lenders on this page. This does not influence our editorial ratings or recommendations. Our reviews are independently researched and editorially independent. Updated April 08, 2026.

✅ No minimum credit score

✅ AI-powered approval (uses education + work history)

✅ Funds in as little as 1 business day

✅ $1,000 – $75,000 loan amounts

✅ 3 or 5 year terms

✅ No prepayment penalty

⚠️ Origination fee: 0% – 12%

✅ Rated 'Excellent' on Trustpilot

People Also Ask

Most personal loan lenders require a minimum score of 580–640. The best rates (under 10% APR) typically require a score of 720+. Some lenders like Upstart consider education and employment history alongside credit scores.

Online lenders like Upstart can approve and fund loans in as little as 1–3 business days. Traditional banks may take 1–2 weeks. Pre-qualification takes just minutes and doesn't affect your credit score.

The average personal loan APR is 11–12% for borrowers with good credit. Rates range from 6% for excellent credit to 36% for poor credit. Always compare at least 3 lenders before accepting an offer.

Yes — lenders like Upstart, Avant, and OneMain Financial specialize in loans for borrowers with scores below 640. Expect higher rates (20–36% APR) and consider a co-signer to improve your terms.