Table of Contents

When considering a personal loan, understanding the differences between lenders like Upstart vs Avant is crucial. Both offer accessible personal loans, but they cater to slightly different borrower profiles and financial situations. This comprehensive guide will delve into the specifics of each lender, helping you determine which personal loan option is better suited for your needs in 2026.

Whether you're looking for competitive rates, flexible repayment terms, or options for less-than-perfect credit, a detailed comparison of Upstart and Avant will provide the insights you need to make an informed decision. We'll examine their APRs, loan amounts, credit score requirements, and unique features to highlight their strengths and weaknesses.

Upstart Personal Loans

Upstart stands out with its innovative AI-driven underwriting model, which considers more than just your credit score. By evaluating factors like education and employment history, Upstart can offer competitive rates to a broader range of borrowers, including those with limited credit history.

Quick Verdict: Upstart vs Avant

In the head-to-head battle of Upstart vs Avant, Upstart often takes the lead for borrowers with better credit profiles or those with strong educational and employment backgrounds, thanks to its AI underwriting model that can offer more favorable rates. However, Avant shines as a more accessible option for individuals with very bad credit, particularly those with scores below 580, offering a pathway to personal loans where other lenders might decline.

Ultimately, the better choice depends on your individual financial situation, credit history, and specific borrowing needs. Both lenders provide valuable services, but their target demographics and lending criteria differ significantly.

Side-by-Side Comparison: Upstart vs Avant

To help you quickly grasp the key differences between these two popular personal loan providers, here's a detailed side-by-side comparison table:

| Feature | Upstart | Avant |

|---|---|---|

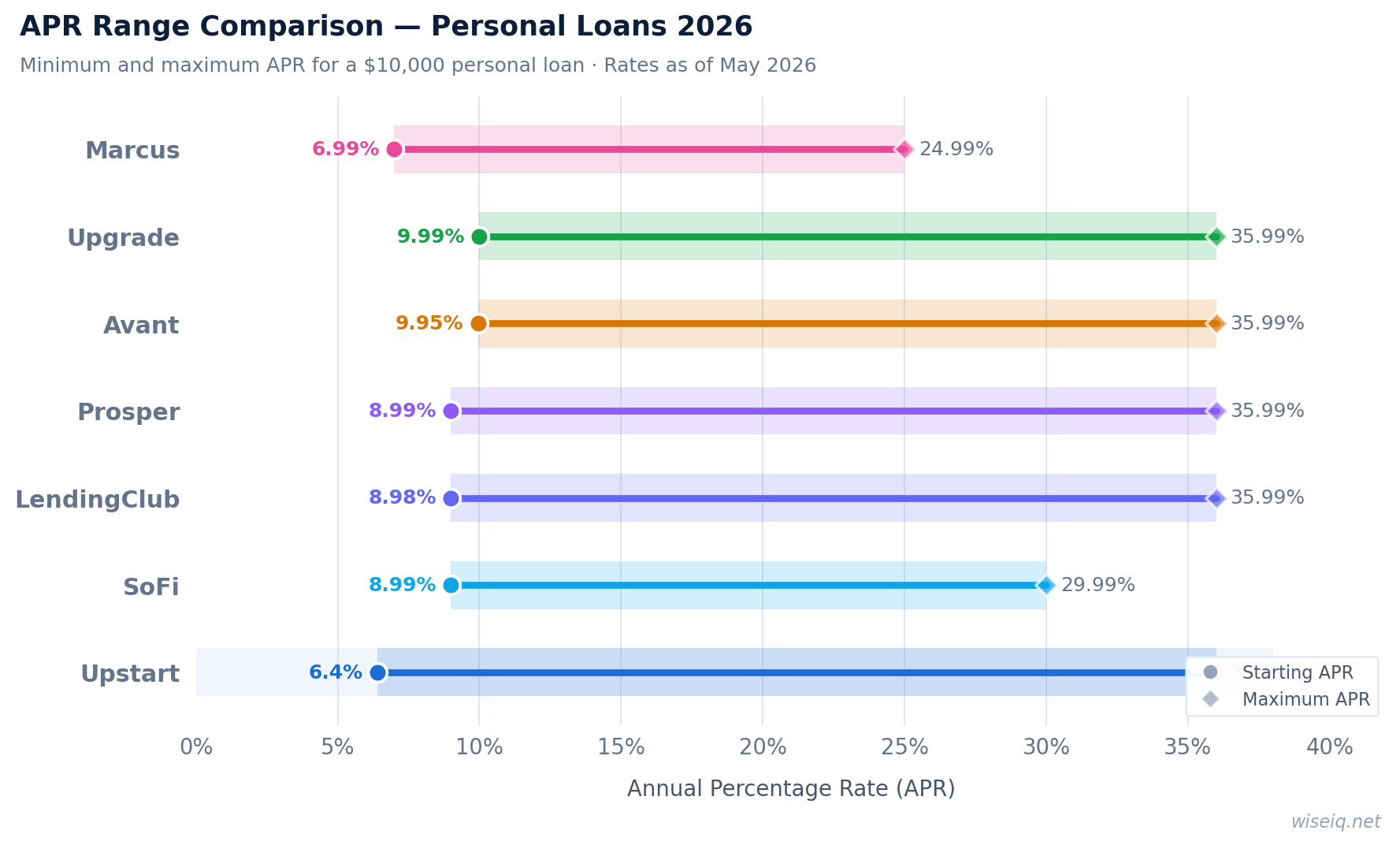

| APR Range | 6.40%–35.99% | 9.95%–35.99% |

| Loan Amounts | $1,000–$50,000 | $2,000–$35,000 |

| Min. Credit Score | 580 | 550 |

| Origination Fee | 0%–12% | Up to 9.99% |

| Loan Terms | 36 or 60 months | 24 to 60 months |

| Funding Time | As fast as 1 business day | 1-2 business days |

| BBB Rating | A+ | A- |

Upstart Overview

Upstart has revolutionized the personal loan market with its unique approach to underwriting. Instead of relying solely on traditional credit scores, Upstart utilizes artificial intelligence to assess a broader range of factors, including education, area of study, and employment history. This allows them to approve a higher percentage of applicants, particularly those with limited credit history but strong earning potential.

With loan amounts ranging from $1,000 to $50,000 and competitive APRs starting as low as 6.40%, Upstart offers flexible options for various financial needs. The application process is entirely online, and many borrowers receive funds as fast as one business day. There are no prepayment penalties, giving borrowers the flexibility to pay off their loans early and save on interest.

Pros of Upstart

- AI-driven underwriting considers more than just credit score

- Potentially lower APRs for qualified borrowers

- Fast funding, often within one business day

- No prepayment penalties

- Available for borrowers with limited credit history

Cons of Upstart

- High maximum APRs (up to 35.99%)

- Origination fees can be as high as 12%

- Not available in all states

- Minimum credit score of 580 still required

Avant Overview

Avant specializes in personal loans for individuals with fair to good credit, including those with scores as low as 550. This makes Avant a viable option for borrowers who might struggle to qualify with more traditional lenders. They offer loan amounts between $2,000 and $35,000, with APRs ranging from 9.95% to 35.99%.

Avant's application process is straightforward and can be completed online. Funds are typically disbursed within one to two business days after approval. While Avant does charge an administration fee (origination fee) of up to 9.99%, they provide a clear repayment schedule and transparent terms. Avant is a solid choice for debt consolidation, home improvement, or unexpected expenses, especially for those with less-than-perfect credit.

Pros of Avant

- Accessible for borrowers with credit scores as low as 550

- Quick online application and funding process

- Clear repayment terms

- Good option for debt consolidation

- Flexible loan amounts up to $35,000

Cons of Avant

- Higher minimum APR compared to Upstart

- Origination fees up to 9.99%

- Not available in all states

- Maximum loan amount is lower than some competitors

Who Should Choose Upstart?

You should consider Upstart if you have a credit score of 580 or higher and a strong educational or employment background. Their AI underwriting model can be particularly beneficial if you have a limited credit history but demonstrate strong financial potential. Upstart is also a good choice if you're looking for potentially lower interest rates and need funds quickly, as they offer funding as fast as one business day.

Upstart is ideal for individuals who are confident in their ability to repay and want a lender that looks beyond just a FICO score. If you're seeking a loan for debt consolidation, a major purchase, or an unexpected expense and believe your overall financial picture is stronger than your credit score suggests, Upstart could be the better option.

Who Should Choose Avant?

Avant is an excellent option for borrowers with credit scores as low as 550, making it more accessible for those with very bad credit. If you've been turned down by other lenders due to your credit history, Avant might be able to provide the personal loan you need. They offer a straightforward application process and quick funding, which can be crucial in urgent financial situations.

Choose Avant if you need a loan between $2,000 and $35,000 and prioritize accessibility over the absolute lowest possible APR. Avant is a reliable choice for managing unexpected expenses, consolidating high-interest debt, or funding home improvements when your credit score is a primary concern.

Verdict: Upstart vs Avant

In summary, both Upstart and Avant offer valuable personal loan products, but they cater to different segments of the market. Upstart excels with its innovative AI underwriting, potentially providing lower rates for those with good credit and strong financial indicators beyond their score. Avant, on the other hand, is a lifeline for borrowers with lower credit scores, offering a more inclusive lending approach.

For the best personal loan, carefully evaluate your credit score, financial history, and how quickly you need funds. Consider checking your rates with both lenders to see which one offers the most favorable terms for your unique situation. Remember, the best personal loan is the one that best fits your financial needs and repayment capabilities.

Frequently Asked Questions about Upstart vs Avant

What are the main differences between Upstart and Avant personal loans?

Upstart considers more than just credit scores, using AI to evaluate education and employment, potentially offering lower APRs for those with limited credit history. Avant focuses more on traditional credit scores, catering to borrowers with fair to good credit, and may be more accessible for those with slightly lower scores.

Which lender offers better interest rates, Upstart or Avant?

Upstart generally offers a wider range of APRs starting lower (6.40%) compared to Avant (9.95%). However, the actual rate you receive depends on your creditworthiness and other factors.

What credit score do I need for Upstart vs Avant?

Upstart typically requires a minimum credit score of 580. Avant is known to work with borrowers with credit scores as low as 550, making it an option for those with very bad credit.

Can I get a personal loan quickly from Upstart or Avant?

Both Upstart and Avant are known for fast funding. Upstart can fund loans as fast as one business day, while Avant also offers quick disbursement, often within one to two business days after approval.

Do Upstart or Avant charge origination fees?

Yes, both lenders charge origination fees. Upstart's origination fees range from 0% to 12%, while Avant's can be up to 9.99%. These fees are typically deducted from your loan proceeds.