Table of Contents

Choosing between personal loan providers can be a daunting task, especially when two prominent lenders like Upstart and SoFi offer compelling options. Both cater to different borrower profiles and financial needs, making a direct comparison essential for anyone seeking the best personal loan in 2026. This comprehensive guide will break down the key differences, advantages, and disadvantages of Upstart vs SoFi, helping you make an informed decision.

Whether you have fair credit and are looking for an AI-powered underwriting approach or possess excellent credit and prioritize features like unemployment protection and no origination fees, understanding the nuances of each lender is crucial. We'll delve into their APRs, loan amounts, credit score requirements, and unique offerings to determine which personal loan is better suited for your specific situation.

Upstart Personal Loan

Upstart vs SoFi — Quick Verdict

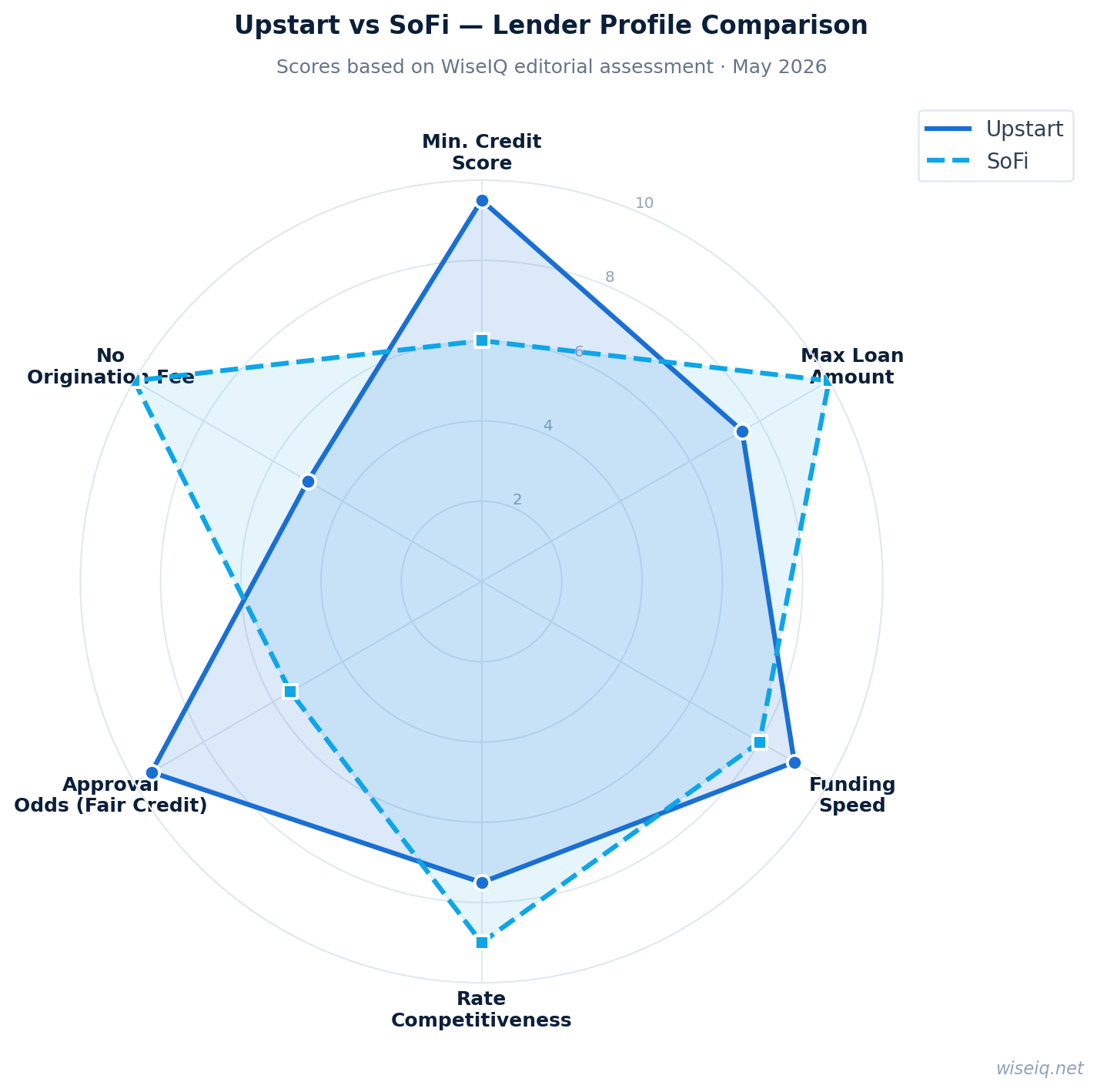

When comparing Upstart vs SoFi, the quick verdict depends heavily on your credit profile. Upstart generally wins for borrowers with fair to average credit scores (typically 580+), leveraging its AI-driven underwriting model that considers more than just your credit score, such as education and employment history. This can make loans accessible to a broader range of applicants who might be overlooked by traditional lenders.

Conversely, SoFi emerges as the stronger choice for individuals with excellent credit (typically 650+) and those who prioritize a no origination fee structure. SoFi's competitive rates and additional benefits like unemployment protection make it a premium option for highly qualified borrowers seeking larger loan amounts and longer terms.

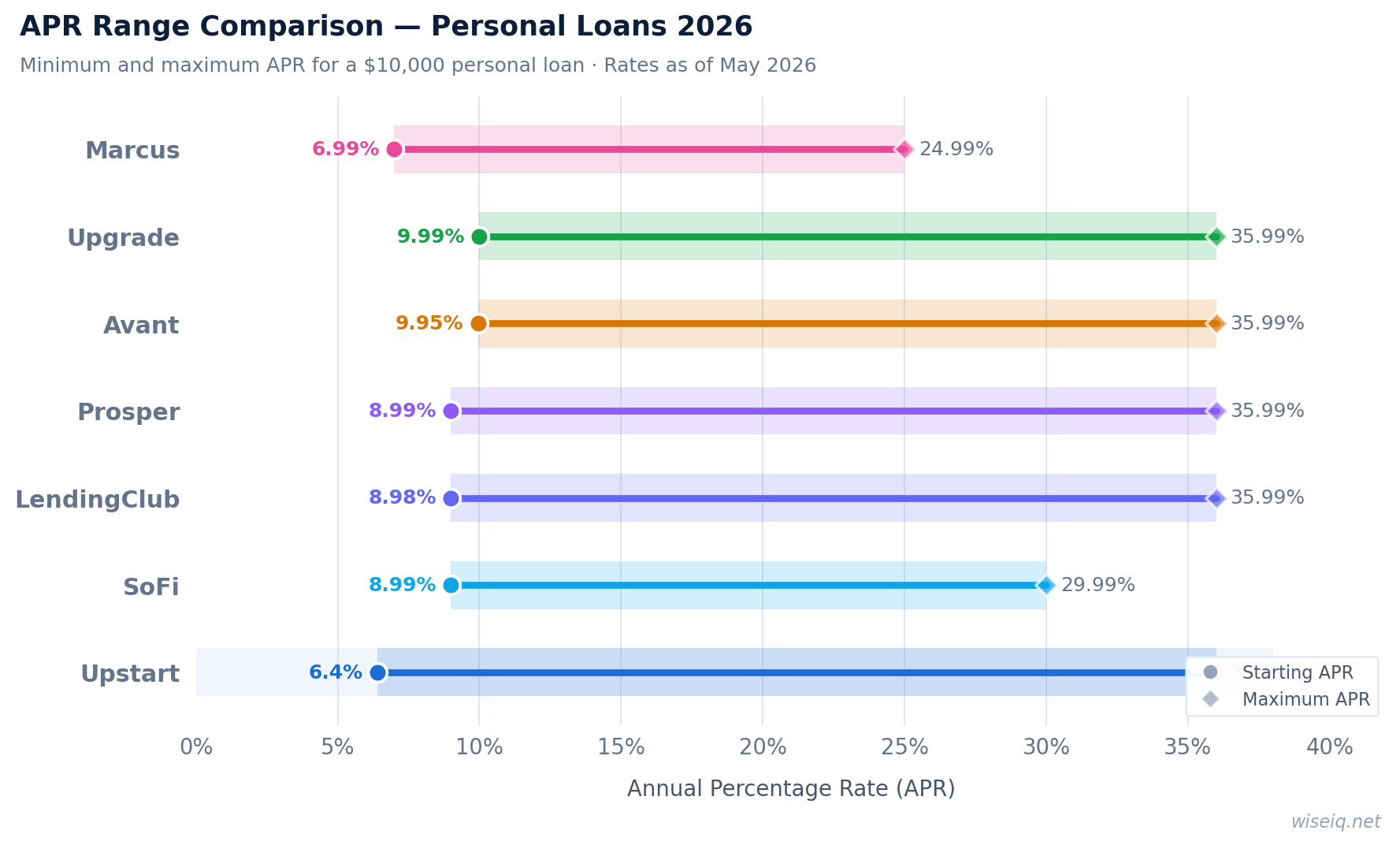

Side-by-Side Comparison Table

| Feature | Upstart | SoFi |

|---|---|---|

| APR Range | 6.40%–35.99% | 8.99%–29.99% |

| Loan Amounts | $1,000–$50,000 | $5,000–$100,000 |

| Minimum Credit Score | 580 | 650 |

| Origination Fee | 0%–12% | 0% |

| Loan Terms | 36 or 60 months | 36, 48, 60, 72, or 84 months |

| Funding Time | As fast as 1 business day | As fast as 1 business day |

| Unemployment Protection | No | Yes |

| BBB Rating | A+ | A+ |

Upstart Overview

Upstart has carved a niche in the personal loan market by focusing on a broader assessment of creditworthiness beyond traditional credit scores. Their innovative AI-powered underwriting model considers factors like education, area of study, and employment history, which can be particularly beneficial for younger borrowers or those with limited credit history. This approach allows Upstart to approve a significant number of applicants who might otherwise be denied by conventional lenders.

With loan amounts ranging from $1,000 to $50,000 and APRs from 6.40% to 35.99%, Upstart offers flexibility for various financial needs. While they do charge an origination fee (0%–12%), the potential for approval with a lower credit score (minimum 580) makes them a strong contender for individuals looking to consolidate debt, cover unexpected expenses, or fund personal projects. Funding can be as fast as one business day, providing quick access to funds when needed.

Pros

- Considers education and employment history

- Lower minimum credit score requirement (580)

- Fast funding (as soon as 1 business day)

- No prepayment penalties

Cons

- Charges origination fees (0%–12%)

- Higher maximum APR compared to SoFi

- No co-signer or joint loan options

SoFi Overview

SoFi, short for Social Finance, is renowned for its comprehensive suite of financial products, including personal loans tailored for borrowers with strong credit profiles. A key differentiator for SoFi is its commitment to charging no origination fees, which can lead to significant savings over the life of the loan. This, combined with competitive APRs (8.99%–29.99%) and larger loan amounts ($5,000–$100,000), makes SoFi an attractive option for well-qualified borrowers.

Beyond favorable rates and terms, SoFi also stands out with its unemployment protection program. This valuable feature offers temporary payment relief in the event of job loss, providing a crucial safety net for borrowers. With a minimum credit score requirement typically around 650, SoFi targets financially responsible individuals seeking substantial loans and additional member benefits.

Who Should Choose Upstart?

Who Should Choose Upstart?

- Borrowers with Fair to Average Credit: If your credit score is around 580 to 660, Upstart's AI-driven underwriting may offer you a better chance of approval.

- Limited Credit History: Younger professionals or those new to credit can benefit from Upstart's consideration of education and employment.

- Smaller Loan Needs: For loan amounts between $1,000 and $5,000, Upstart provides accessible options.

- Quick Funding: If you need funds as fast as one business day, Upstart can deliver.

Who Should Choose SoFi?

Who Should Choose SoFi?

- Borrowers with Excellent Credit: If your credit score is 650 or higher, SoFi offers highly competitive rates and terms.

- No Origination Fees: For those who want to avoid upfront costs, SoFi's 0% origination fee is a significant advantage.

- Larger Loan Amounts: If you need a loan between $5,000 and $100,000, SoFi can accommodate larger financial needs.

- Unemployment Protection: The added security of unemployment protection is a major benefit for many borrowers.

- Longer Loan Terms: SoFi offers more flexible repayment terms, including options up to 84 months.

Verdict

In the battle of Upstart vs SoFi, there's no single winner; rather, the best choice depends on your individual financial circumstances and credit profile. Upstart shines as an innovator, opening doors for borrowers with less-than-perfect credit by looking beyond traditional metrics. Their AI model provides opportunities for those with fair to average credit scores, making personal loans more accessible.

SoFi, on the other hand, caters to the prime borrower, offering highly competitive rates, no origination fees, and valuable perks like unemployment protection. If you have excellent credit and are seeking a larger loan with a robust safety net, SoFi is likely the superior option. Ultimately, both lenders provide excellent services within their respective target markets, and comparing their offerings against your personal needs is the key to making the right decision.