Table of Contents

Navigating the world of personal finance can be challenging, especially when your credit score isn't perfect. If you have a personal loan 620 credit score, you might be wondering about your options. The good news is that a 620 FICO score, while considered fair credit, doesn't automatically disqualify you from securing a personal loan. Many lenders specialize in working with borrowers who have less-than-perfect credit, offering pathways to financial solutions.

This comprehensive guide will explore the best strategies and lenders for obtaining a personal loan with a 620 credit score in 2026. We'll delve into what APRs you can expect, how to improve your chances of approval, and whether waiting to boost your score is a wise move. Our goal is to provide you with the knowledge and resources to make informed decisions about your financial future, helping you find the best options available.

Upstart: Best for Fair Credit Borrowers

Upstart stands out for its innovative approach to lending, utilizing AI underwriting to assess more than just your credit score. This makes it an excellent option for those with a personal loan 620 credit score, as they consider factors like education and employment history.

Can you get a personal loan with a 620 credit score?

Absolutely. A personal loan 620 credit score falls into the "fair" credit category according to FICO. While this isn't considered prime, it's far from impossible to secure a loan. Many lenders are willing to work with borrowers in this range, understanding that a credit score doesn't always tell the whole financial story. These lenders often look beyond just your FICO 620 score, considering other aspects of your financial health.

The key is knowing where to look and understanding what lenders prioritize. Some financial institutions specialize in non-traditional underwriting, which means they use alternative data points to assess your creditworthiness. This can include your education, employment history, and even banking transactions, offering a more holistic view of your ability to repay a loan. This approach can significantly improve your chances of approval even with a fair credit score.

Best lenders for 620 credit score — Upstart #1

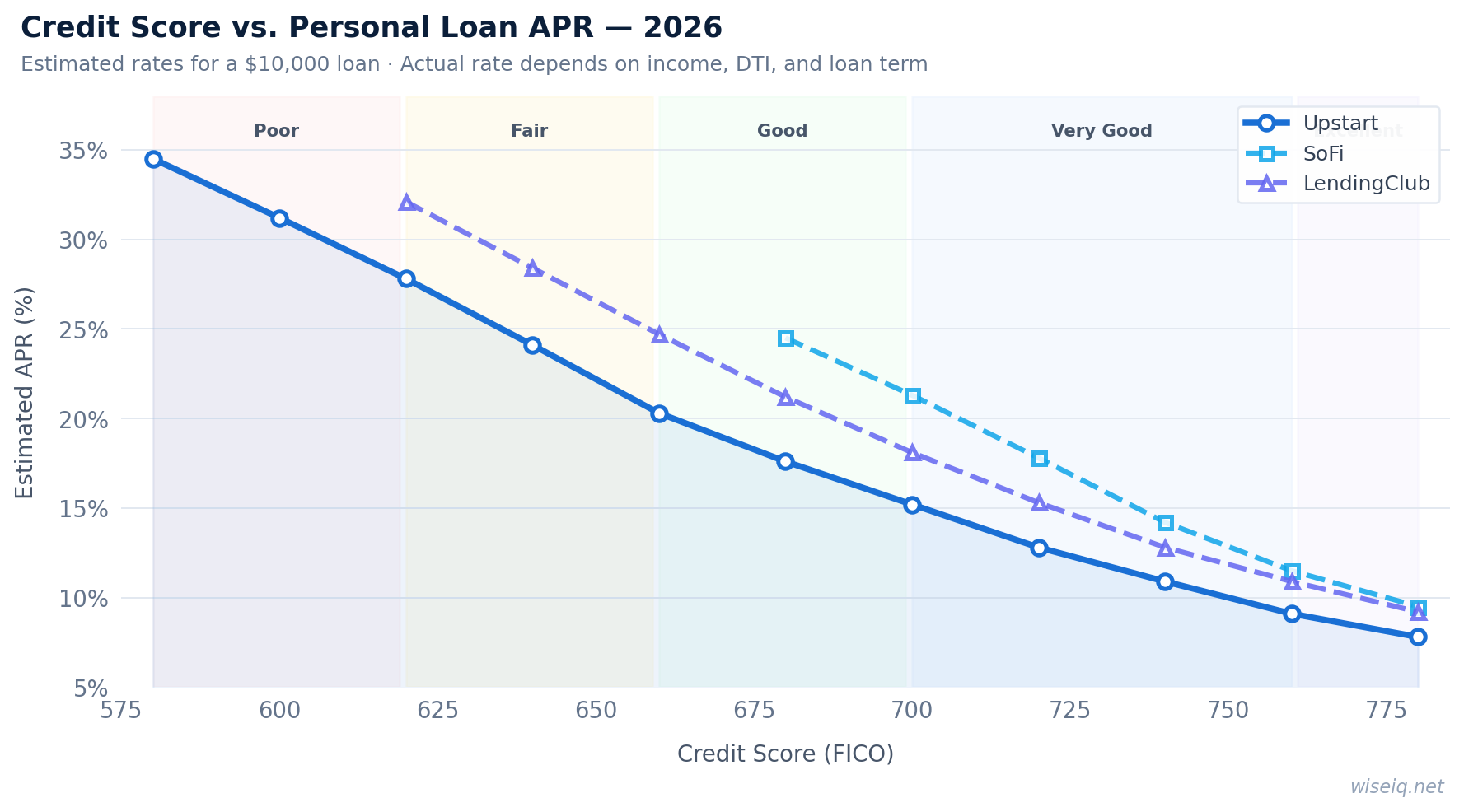

When seeking a personal loan 620 credit score, certain lenders stand out due to their flexible eligibility criteria and competitive offerings for fair credit borrowers. Upstart is consistently ranked as a top choice, primarily because of its innovative AI-driven underwriting model. Unlike traditional lenders that heavily rely on credit scores, Upstart considers factors like your education, area of study, and job history, which can be a significant advantage if your credit history is limited or imperfect.

Beyond Upstart, other lenders also cater to individuals with a 620 credit score. These often include online lenders and credit unions that may offer more personalized service and potentially lower rates than large banks. It's crucial to compare offers from multiple lenders to find the best terms, including interest rates, fees, and repayment schedules. Always look for lenders that offer prequalification with a soft credit pull, as this allows you to check your potential rates without impacting your credit score.

Comparison Table: Lenders for a 620 Credit Score

| Lender | Min. Credit Score | APR Range | Max Amount |

|---|---|---|---|

| Upstart | 580 | 6.40%–35.99% | $50,000 |

| Avant | 580 | 9.95%–35.99% | $35,000 |

| LendingPoint | 600 | 7.99%–35.99% | $36,500 |

| OneMain Financial | No minimum | 18.00%–35.99% | $20,000 |

What APR to expect with a 620 score

When you have a personal loan 620 credit score, the Annual Percentage Rate (APR) you can expect will generally be higher than for borrowers with excellent credit. Typically, individuals with a 620 FICO score can anticipate APRs ranging from 15% to 28%. This range reflects the increased risk lenders perceive when extending credit to fair credit borrowers. However, it's important to remember that this is a general guideline, and your actual APR will depend on several factors.

Factors influencing your APR include the loan amount, the loan term, your debt-to-income ratio, and the specific lender's policies. Some lenders might offer slightly lower rates if you have a strong income or a low debt burden, even with a 620 credit score. Always review the loan offer details carefully, paying close attention to the APR, any origination fees, and other associated costs to understand the true cost of borrowing.

How to improve your odds at 620

Even with a personal loan 620 credit score, there are several proactive steps you can take to significantly improve your chances of loan approval and potentially secure more favorable terms. One of the most effective strategies is to utilize prequalification. Many online lenders offer a prequalification process that involves a soft credit pull, which doesn't harm your credit score. This allows you to see potential loan offers and compare rates without commitment.

Another crucial step is to ensure your debt-to-income (DTI) ratio is as low as possible. Lenders view a lower DTI as a sign of responsible financial management. If possible, pay down existing debts before applying for a new loan. Additionally, having a stable employment history and a consistent income can reassure lenders. If your credit history is thin, consider adding a co-signer with good credit, as this can significantly boost your application.

Should you wait to improve your score first?

The decision to wait and improve your credit score before applying for a personal loan 620 credit score depends largely on your immediate financial needs and the urgency of the loan. If you have an immediate financial emergency, waiting might not be an option. However, if your need for funds is not time-sensitive, taking a few months to boost your FICO 620 score could result in substantial savings over the life of the loan.

Even a small increase in your credit score can move you into a better credit tier, qualifying you for lower interest rates and more flexible terms. Strategies to improve your score include paying all bills on time, reducing credit card balances, and avoiding new credit applications. If you can realistically raise your score by 30-50 points within a few months, the financial benefits of a lower APR could outweigh the inconvenience of waiting.

How to build credit while repaying your loan

A personal loan, even one obtained with a personal loan 620 credit score, can be a powerful tool for building and improving your credit history. The most critical factor in credit building is consistent, on-time payments. Every payment you make on time demonstrates financial responsibility to credit bureaus, which positively impacts your FICO score.

Beyond timely payments, a personal loan can also help diversify your credit mix. Having a mix of credit types, such as installment loans (like personal loans) and revolving credit (like credit cards), is generally viewed favorably by credit scoring models. As you successfully repay your loan, your credit utilization ratio may also improve, especially if you are simultaneously managing other debts responsibly. This consistent positive activity will gradually increase your credit score, opening doors to better financial products in the future.