Table of Contents

A personal loan for debt consolidation can be a powerful tool to regain control of your finances, especially if you're struggling with multiple high-interest debts like credit card balances. By combining several debts into a single new loan, you can simplify your monthly payments, potentially secure a lower interest rate, and work towards a clearer payoff timeline. This guide will walk you through how these loans work, when they make financial sense, and how to choose the best lender for your situation in 2026.

Navigating various debts can be overwhelming, but a well-chosen debt consolidation loan offers a strategic path to financial relief. It's not just about making payments easier; it's about reducing the total interest you pay and improving your debt-to-income ratio, which can positively impact your credit over time. Let's explore how to leverage this financial strategy effectively.

Upstart Personal Loan for Debt Consolidation

Upstart stands out for its innovative AI-powered underwriting, which considers more than just your credit score. This can be a game-changer for those with limited credit history but strong educational and employment backgrounds, making it easier to qualify for a personal loan for debt consolidation.

Advertiser Disclosure: We may earn a commission if you apply through our link.

How Debt Consolidation Loans Work

A debt consolidation loan is essentially a new personal loan that you use to pay off several existing debts. Instead of managing multiple payments to different creditors each month, you make one single monthly payment to your new loan provider. The primary goal is often to secure a lower interest rate than what you're currently paying on your high-interest debt, such as credit card debt, which can lead to significant total interest savings.

When you apply for a personal loan for debt consolidation, lenders evaluate your creditworthiness, including your credit score, income, and debt-to-income ratio. If approved, the loan funds are typically disbursed directly to your creditors, or sometimes to you, to pay off the specified debts. This process simplifies your financial obligations and can provide a clear payoff timeline, helping you become debt-free faster.

When a Consolidation Loan Makes Sense

A debt consolidation loan is particularly beneficial when you have a good credit score that allows you to qualify for a lower Annual Percentage Rate (APR) than your current average interest rate on existing debts. It's also ideal if you prefer the simplicity of a single monthly payment and are committed to not accumulating new high-interest debt.

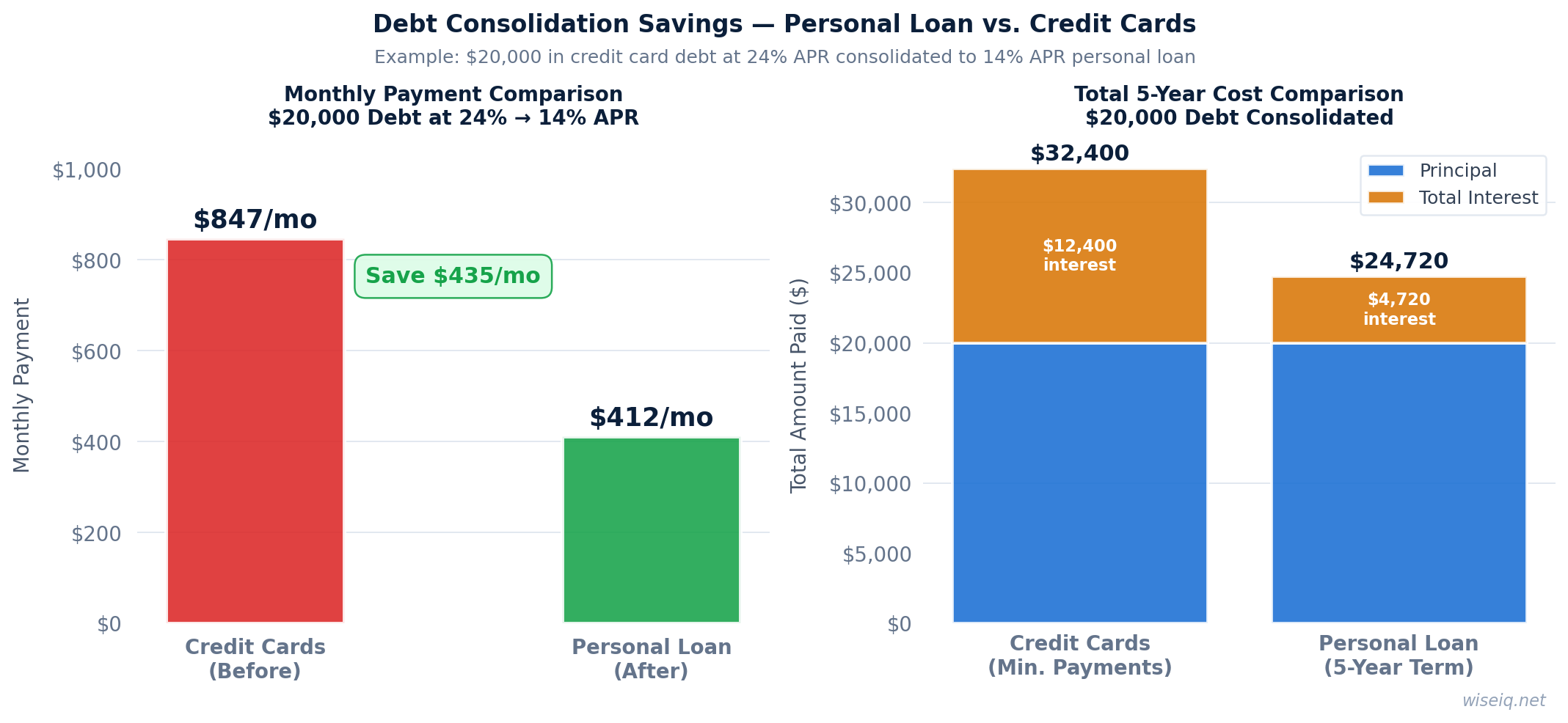

Interest Savings Example: Credit Card vs. Personal Loan

Imagine you have $20,000 in credit card debt with an average APR of 22%. If you were to pay this off over 60 months, your total interest paid could be substantial. Now, consider consolidating this with a personal loan at a 12% APR over the same 60-month term. The difference in monthly payments and total interest savings can be dramatic:

- Credit Card ($20,000 at 22% APR, 60 months): Approx. $556 monthly payment, ~$13,360 total interest.

- Personal Loan ($20,000 at 12% APR, 60 months): Approx. $445 monthly payment, ~$6,700 total interest.

In this scenario, a personal loan for debt consolidation could save you over $6,600 in total interest and reduce your monthly payment by over $100.

Best Debt Consolidation Lenders

While Upstart is our top pick due to its innovative underwriting, several other lenders offer competitive personal loans for debt consolidation. When evaluating lenders, consider factors like APR range, loan amounts, minimum credit score requirements, origination fees, and funding speed. It's always wise to compare offers from multiple lenders to find the best fit for your financial situation.

Look for lenders that are transparent about their terms and fees, and read customer reviews to gauge their service quality. Some lenders specialize in borrowers with excellent credit, offering the lowest rates, while others cater to those with fair or average credit, providing more accessible options.

How to Qualify for a Debt Consolidation Loan

Qualifying for a personal loan for debt consolidation typically involves meeting certain criteria set by lenders. These often include:

- Credit Score: A higher credit score generally leads to better interest rates. While some lenders like Upstart consider scores as low as 580, many prefer scores in the good to excellent range (670+).

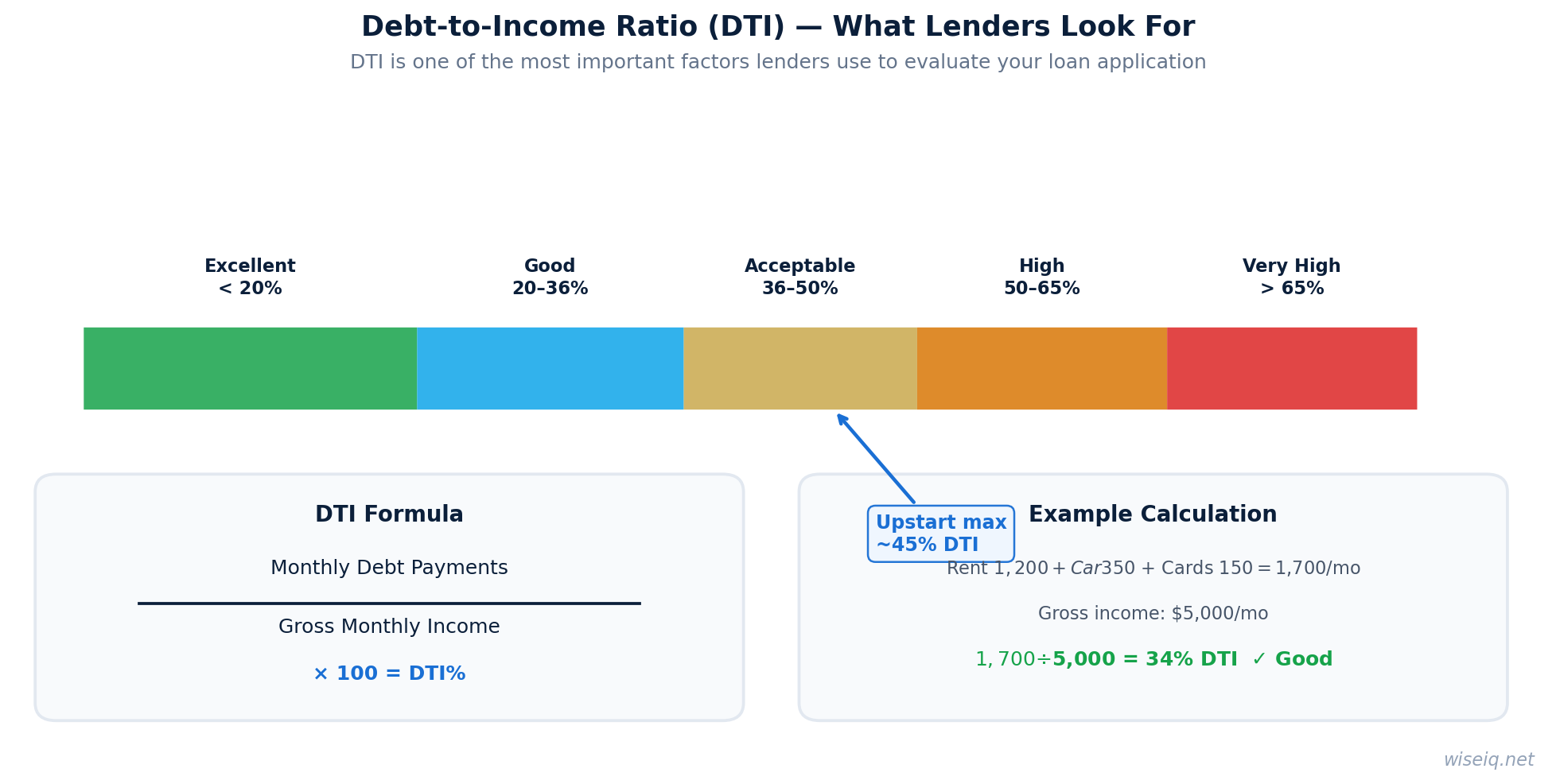

- Debt-to-Income (DTI) Ratio: Lenders assess your DTI to ensure you can comfortably afford the new loan payments. A lower DTI indicates less risk.

- Income and Employment History: Stable income and consistent employment demonstrate your ability to repay the loan.

- Credit History: A history of responsible credit use, even with some high-interest debt, can be favorable.

It's important to check your credit report for errors before applying and consider steps to improve your credit score if needed. A strong application can significantly impact the loan terms you're offered.

Debt Consolidation vs. Balance Transfer vs. Debt Management Plan

When looking to manage or reduce debt, a personal loan for debt consolidation is one of several options. It's crucial to understand how it compares to alternatives like balance transfer credit cards and debt management plans to choose the most suitable strategy for your financial health.

| Feature | Debt Consolidation Loan | Balance Transfer Credit Card | Debt Management Plan (DMP) |

|---|---|---|---|

| Purpose | Combine multiple debts into one loan, often with lower interest. | Move high-interest credit card debt to a new card with a 0% intro APR. | Structured plan to pay off unsecured debt through a credit counseling agency. |

| Interest Rate | Fixed or variable, generally lower than credit cards. | 0% intro APR for a period (e.g., 12-21 months), then a variable rate. | Negotiated lower interest rates with creditors. |

| Eligibility | Good to excellent credit often required for best rates; some lenders for fair credit. | Good to excellent credit typically required. | Available to those struggling with debt, regardless of credit score. |

| Impact on Credit | Initial dip from hard inquiry, then potential improvement with timely payments. | Temporary dip from new account, then potential improvement if managed well. | Can negatively impact credit score initially, but improves with consistent payments. |

| Fees | Origination fees (0-12%) may apply. | Balance transfer fees (3-5%) typically apply. | Monthly fees for the counseling agency. |

| Debt Type | Unsecured debts (credit cards, medical bills, etc.). | Credit card debt only. | Unsecured debts (credit cards, personal loans, etc.). |

Each option has its pros and cons, and the best choice depends on your specific financial situation, credit score, and discipline. A personal loan for debt consolidation offers predictable payments and a clear payoff timeline, while a balance transfer can provide a temporary reprieve from interest if you can pay off the debt within the promotional period. A debt management plan is often a last resort before bankruptcy, offering structured support for those in significant financial distress.

Step-by-Step Guide to Consolidating Debt

Consolidating your debt with a personal loan can be a straightforward process if you follow these steps:

- Assess Your Debt: List all your high-interest debts, including balances, interest rates, and minimum payments. Calculate your total debt and average interest rate.

- Check Your Credit Score: Understand your credit standing, as it will influence the rates you qualify for. Obtain a free credit report to check for accuracy.

- Compare Lenders and Offers: Research various lenders, including Upstart, and compare their APRs, fees, loan terms, and eligibility requirements. Get pre-qualified with multiple lenders to see personalized rates without impacting your credit score.

- Apply for the Loan: Once you've chosen a lender, complete the full application. Be prepared to provide documentation like proof of income, employment, and identity.

- Pay Off Old Debts: If approved, the loan funds will typically be sent directly to your creditors to pay off your existing high-interest debt. Ensure all old accounts are closed or paid in full to avoid accumulating new debt.

- Make New Payments: Begin making consistent, on-time payments to your new debt consolidation loan. This is crucial for improving your credit score and achieving your payoff timeline.

By following these steps, you can effectively use a personal loan for debt consolidation to simplify your finances and work towards a debt-free future. Remember to maintain good financial habits to avoid falling back into debt.