Table of Contents

- Is a $25,000 personal loan right for you?

- How to qualify — DTI under 45%, stable income, credit score 580+

- Monthly payment table: at 6%, 10%, 15%, 20%, 25% APR for 36 and 60 months

- Best lenders for $25K — Upstart #1, LendingClub, SoFi, Prosper, Upgrade

- Best uses: home renovation, debt consolidation, business startup, medical, wedding

- Step-by-step application guide

Navigating the world of personal finance can be complex, especially when considering a significant financial commitment like a $25,000 personal loan. This comprehensive guide from WiseIQ is designed to help you understand every aspect of securing such a loan, from eligibility requirements to finding the best lenders and making informed decisions about its use. Our goal is to empower you with the knowledge to confidently pursue your financial objectives, whether it's consolidating high-interest debt, funding a major life event, or undertaking a home improvement project.

A $25,000 personal loan offers a versatile solution for various financial needs, providing a fixed sum that you repay over a set period with predictable monthly payments. Unlike secured loans, personal loans are typically unsecured, meaning they don't require collateral. This guide will delve into how to qualify, what interest rates to expect, and highlight top lenders like Upstart, LendingClub, and SoFi, ensuring you have all the information needed to make the best choice for your financial future.

Upstart: Best for Fair Credit & AI Underwriting

Upstart stands out as a top lender for $25,000 personal loans, especially for those with fair credit. Their innovative AI-powered underwriting model goes beyond traditional credit scores, considering factors like education and employment history to give you a more personalized rate. This approach can make it easier for a wider range of applicants to qualify for competitive rates.

Pros

- AI-powered underwriting for broader eligibility

- Fast funding, often within one business day

- No prepayment penalties

- Considers education and employment history

Cons

- Higher APRs for lower credit scores

- Origination fees can be up to 12%

- Not available in all states

Is a $25,000 personal loan right for you?

A $25,000 personal loan can be a powerful financial tool, offering a lump sum of money that can be used for a variety of purposes. Whether you're looking to consolidate high-interest debt, finance a major home improvement project, or cover unexpected expenses, a loan of this size can provide the necessary capital. However, it's important to assess if taking on this level of debt aligns with your financial situation and goals.

Before committing to a $25,000 personal loan, consider your current income, existing debts, and credit score. Lenders will evaluate these factors to determine your eligibility and the interest rate you'll receive. A well-managed personal loan can improve your financial standing, but a poorly managed one can lead to increased financial strain. This guide will help you navigate the process, from qualification to finding the best lenders and understanding repayment.

How to qualify — DTI under 45%, stable income, credit score 580+

Qualifying for a $25,000 personal loan involves meeting specific criteria set by lenders. While requirements can vary, common factors include your debt-to-income (DTI) ratio, income stability, and credit score. A strong financial profile increases your chances of approval and securing a favorable interest rate.

Most lenders prefer a DTI ratio under 45%, meaning your total monthly debt payments should not exceed 45% of your gross monthly income. A stable employment history and sufficient income to comfortably repay the loan are also critical. For credit scores, a minimum of 580 is often required, though higher scores will unlock better loan terms. Lenders like Upstart may also consider factors beyond traditional credit scores, such as education and employment history, to provide a more holistic assessment.

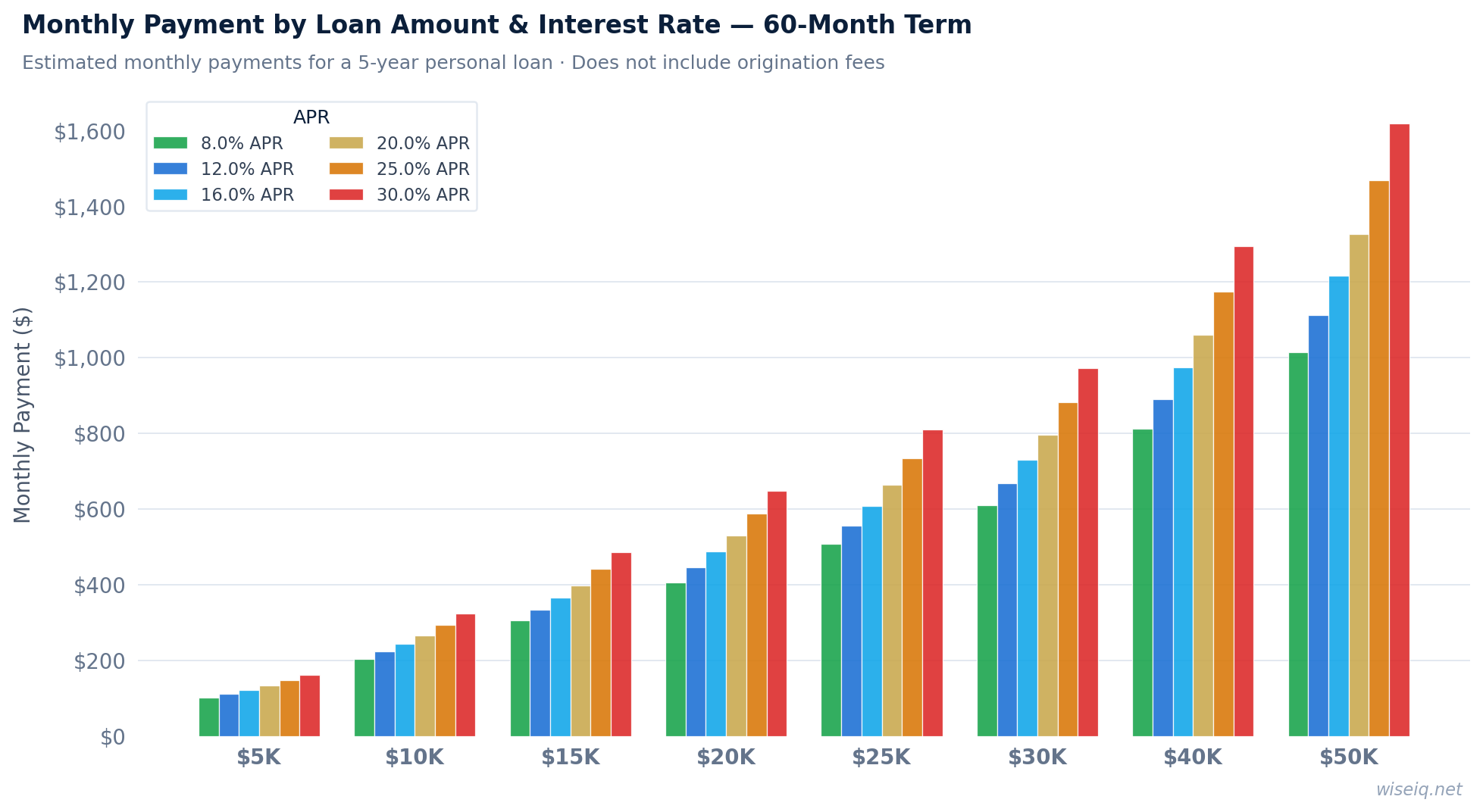

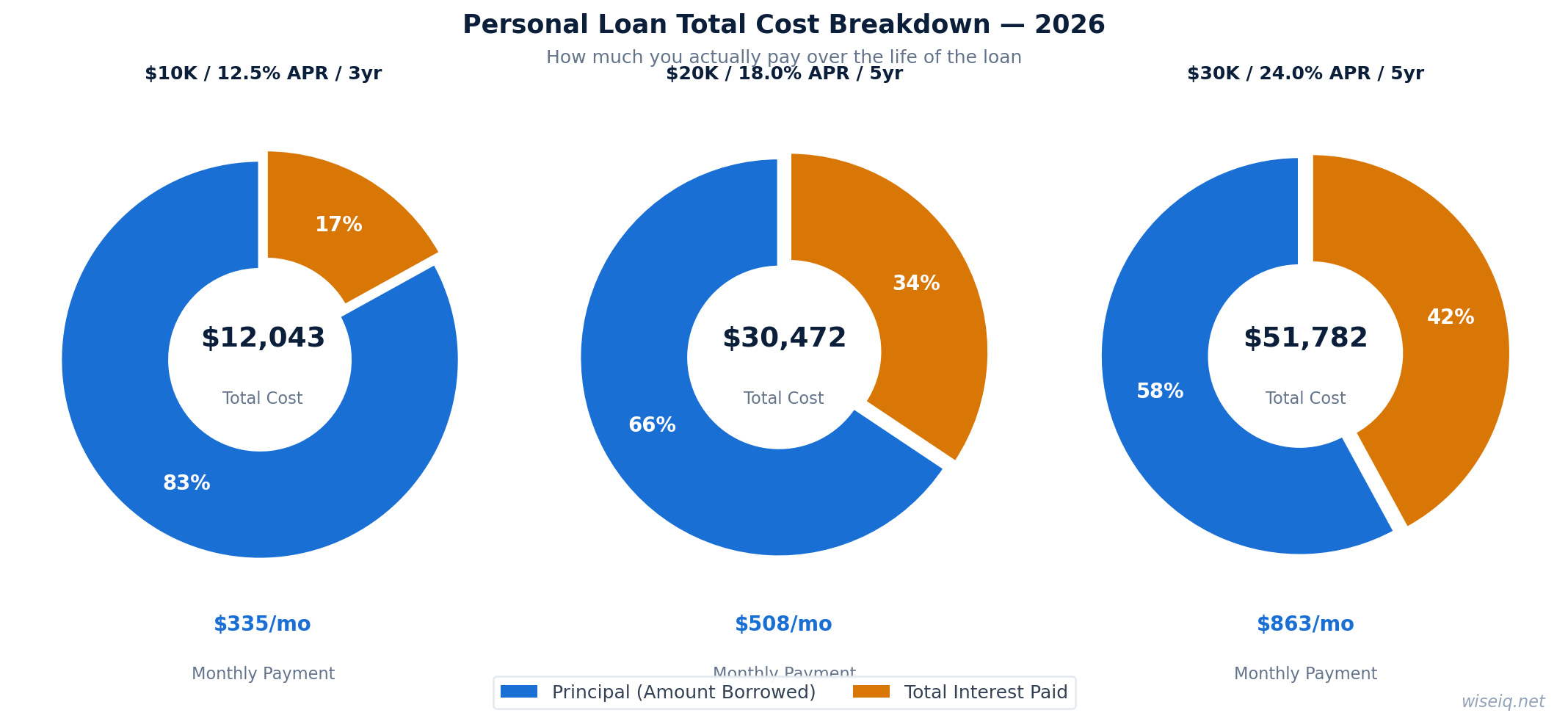

Monthly payment table: at 6%, 10%, 15%, 20%, 25% APR for 36 and 60 months

Understanding your potential monthly payments is crucial when considering a $25,000 personal loan. The amount you pay each month will depend on the interest rate (APR) and the loan term. Below is a table illustrating estimated monthly payments for a $25,000 loan at various APRs and terms.

| APR | 36 Months | 60 Months |

|---|---|---|

| 6% | $760.55 | $483.32 |

| 10% | $806.68 | $531.18 |

| 15% | $866.63 | $594.75 |

| 20% | $929.09 | $662.35 |

| 25% | $994.00 | $733.78 |

Note: These figures are estimates and do not include potential origination fees or other charges. Your actual monthly payment may vary based on the lender and your specific loan terms.

Best uses: home renovation, debt consolidation, business startup, medical, wedding

A $25,000 personal loan can be a powerful financial tool, offering a lump sum of money that can be used for a variety of purposes. Whether you're looking to consolidate high-interest debt, finance a major home improvement project, or cover unexpected expenses, a loan of this size can provide the necessary capital. However, it's important to assess if taking on this level of debt aligns with your financial situation and goals.

Before committing to a $25,000 personal loan, consider your current income, existing debts, and credit score. Lenders will evaluate these factors to determine your eligibility and the interest rate you'll receive. A well-managed personal loan can improve your financial standing, but a poorly managed one can lead to increased financial strain. This guide will help you navigate the process, from qualification to finding the best lenders and understanding repayment.

Step-by-step application guide

Qualifying for a $25,000 personal loan involves meeting specific criteria set by lenders. While requirements can vary, common factors include your debt-to-income (DTI) ratio, income stability, and credit score. A strong financial profile increases your chances of approval and securing a favorable interest rate.

Most lenders prefer a DTI ratio under 45%, meaning your total monthly debt payments should not exceed 45% of your gross monthly income. A stable employment history and sufficient income to comfortably repay the loan are also critical. For credit scores, a minimum of 580 is often required, though higher scores will unlock better loan terms. Lenders like Upstart may also consider factors beyond traditional credit scores, such as education and employment history, to provide a more holistic assessment.

Best lenders for $25K — Upstart #1, LendingClub, SoFi, Prosper, Upgrade

When seeking a $25,000 personal loan, comparing lenders is essential to find the best rates and terms. Here's a comparison of top lenders, including our featured choice, Upstart:

| Lender Name | APR | Min Credit | Origination Fee | Funding Time |

|---|---|---|---|---|

| Upstart | 6.40%–35.99% | 580 | 0%–12% | as fast as 1 business day |

| LendingClub | 8.30%–35.89% | 600 | 3%–6% | ~4 days |

| SoFi | 8.99%–29.99% | 680 | 0% | ~2 days |

| Prosper | 6.99%–35.99% | 640 | 2.41%–5% | ~5 days |

| Upgrade | 8.49%–35.99% | 620 | 2.9%–8% | ~4 days |

Note: APRs and terms are subject to change and depend on your creditworthiness. It's always recommended to check directly with each lender for the most current information.

Frequently Asked Questions

What is a $25,000 personal loan?

A $25,000 personal loan is an unsecured installment loan that provides a lump sum of money, which you repay over a fixed period with regular, typically monthly, payments. It can be used for various purposes, such as debt consolidation, home improvements, or unexpected expenses.

What credit score do I need for a $25,000 personal loan?

While requirements vary by lender, a credit score of 580 or higher is generally recommended to qualify for a $25,000 personal loan. Lenders like Upstart may consider other factors beyond just your credit score, such as your education and employment history.

How quickly can I get a $25,000 personal loan?

Many online lenders, including Upstart, can approve and fund a $25,000 personal loan as fast as one business day after your application is complete and approved. Traditional banks or credit unions might take longer.

Can I get a $25,000 personal loan with bad credit?

It can be challenging to get a $25,000 personal loan with bad credit, but not impossible. Some lenders specialize in loans for borrowers with less-than-perfect credit, often considering factors beyond just your credit score. However, you may face higher interest rates and fees.

What are the best uses for a $25,000 personal loan?

A $25,000 personal loan can be used for a variety of purposes, including debt consolidation, home renovation, financing a business startup, covering medical expenses, or funding a wedding. It's best to use it for purposes that offer a clear financial benefit or address an urgent need.