Table of Contents

Securing a $20,000 personal loan can be a significant financial decision that empowers you to consolidate high-interest debt, fund a major home renovation, or cover unexpected medical expenses. With a fixed interest rate and predictable monthly payments, a personal loan offers a structured way to borrow money without putting your assets at risk, as most personal loans are unsecured.

When searching for the best large personal loans, it is crucial to compare offers from multiple lenders. Interest rates, origination fees, and repayment terms can vary widely based on your credit profile. By taking the time to shop around, you can find a loan that fits your budget and helps you achieve your financial goals efficiently. In this comprehensive guide, we will explore everything you need to know about obtaining a $20K loan, from qualifying requirements to the top lenders in the market.

Upstart

Upstart is our top choice for a $20,000 personal loan, especially for borrowers with less-than-perfect credit. Their AI-driven underwriting model considers factors beyond your credit score, such as education and employment history, potentially offering better rates and higher approval chances.

Is a $20,000 personal loan right for you?

Before committing to a $20,000 personal loan, it is essential to evaluate whether it aligns with your financial situation. A personal loan provides a lump sum of money upfront, which you repay in fixed monthly installments over a set period, typically ranging from two to seven years. This predictability makes it an excellent tool for budgeting, as your payment will not fluctuate like it might with a credit card.

However, borrowing $20,000 is a substantial commitment. You must ensure that your monthly budget can comfortably accommodate the new loan payment. If you are using the loan for debt consolidation, it only makes sense if the new interest rate is significantly lower than what you are currently paying on your existing debts. Additionally, you should be disciplined enough not to rack up new debt on the credit cards you just paid off.

Consider alternatives as well. If you are a homeowner with significant equity, a home equity loan or line of credit (HELOC) might offer lower interest rates, though they require you to use your home as collateral. For smaller expenses, a 0% introductory APR credit card could be a cheaper option if you can pay off the balance before the promotional period ends. Ultimately, a $20,000 personal loan is best suited for borrowers who need a fixed repayment schedule and do not want to risk their assets.

How to qualify for a $20K loan

Qualifying for a $20,000 personal loan requires meeting specific criteria set by lenders to ensure you have the ability to repay the debt. While requirements vary by institution, the primary factors lenders evaluate include your credit score, debt-to-income (DTI) ratio, and income level.

Credit Score: Your credit score is one of the most critical factors in determining your eligibility and the interest rate you will receive. To qualify for a $20,000 loan, most lenders require a minimum credit score of 580 to 600. However, to secure the most favorable rates, a good to excellent credit score (670 or higher) is typically necessary. Borrowers with lower scores may still qualify but will likely face higher APRs and origination fees.

Debt-to-Income (DTI) Ratio: Lenders calculate your DTI ratio by dividing your total monthly debt payments by your gross monthly income. This metric helps them assess whether you can comfortably manage an additional loan payment. Generally, lenders prefer a DTI ratio below 36%, though some may accept ratios up to 50% depending on other compensating factors, such as a high income or excellent credit score.

Income Requirements: You must demonstrate a stable and sufficient income to repay a $20,000 loan. While some lenders do not disclose a strict minimum income requirement, they will verify your employment and income through pay stubs, W-2s, or tax returns. A higher income not only improves your chances of approval but can also help you secure a lower interest rate.

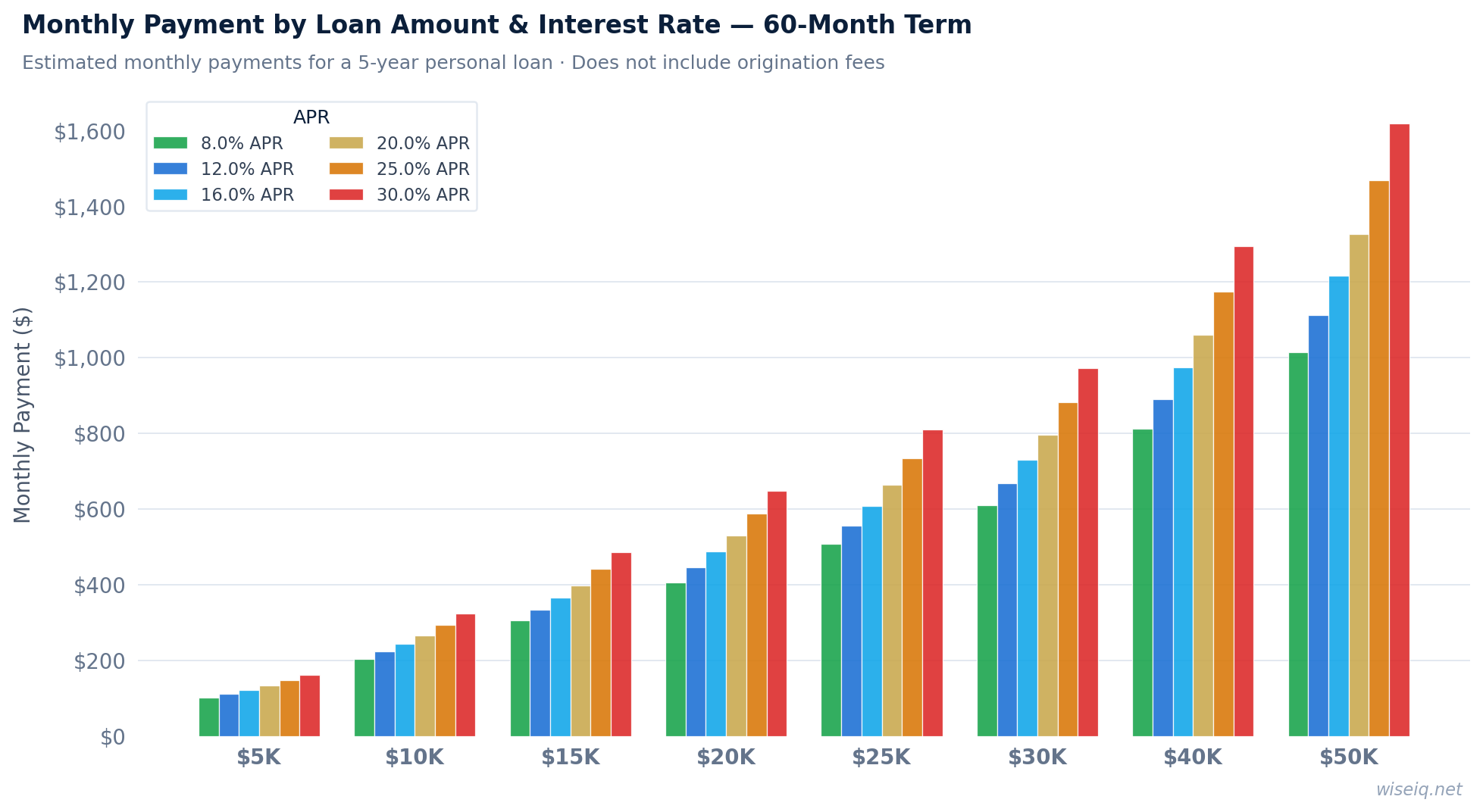

Monthly payment table

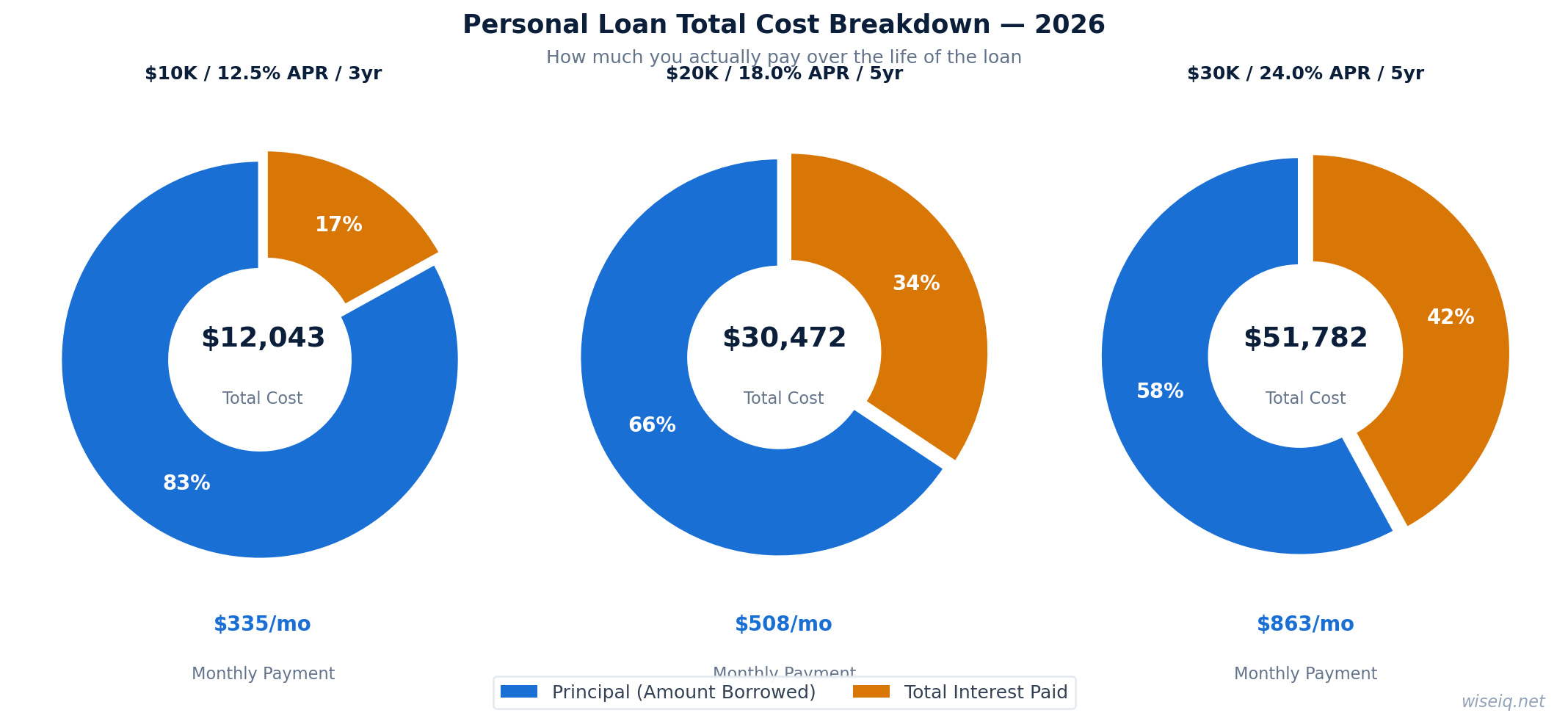

Understanding how different interest rates and loan terms affect your monthly payment is crucial when taking out a $20,000 personal loan. A shorter term will result in higher monthly payments but less total interest paid over the life of the loan. Conversely, a longer term lowers your monthly payment but increases the total cost of borrowing.

The table below illustrates estimated monthly payments for a $20,000 loan at various APRs for 36-month and 60-month terms. Note that these calculations do not include potential origination fees, which could reduce the actual loan amount you receive or increase your total loan balance.

| APR | Monthly Payment (36 Months) | Monthly Payment (60 Months) |

|---|---|---|

| 6.00% | $608 | $387 |

| 10.00% | $645 | $425 |

| 15.00% | $693 | $476 |

| 20.00% | $743 | $530 |

| 25.00% | $795 | $587 |

Best lenders for $20K

Finding the right lender for your $20,000 personal loan depends on your unique financial profile and priorities. Some lenders excel in offering low rates to highly qualified borrowers, while others specialize in fast funding or flexible underwriting for those with less-than-perfect credit. Here are our top picks for the best lenders offering $20K loans in 2026.

1. Upstart

Upstart stands out as our top recommendation, particularly for borrowers who may not have an extensive credit history or have a lower credit score. Upstart uses an innovative AI-driven underwriting model that considers alternative data, such as your education and employment history, rather than relying solely on your FICO score. This approach can lead to higher approval rates and potentially lower APRs for eligible applicants. They offer loans from $1,000 to $50,000 with funding as fast as one business day.

Pros

- AI underwriting considers education and job history

- Minimum credit score of just 580

- Fast funding, often within 1 business day

- No prepayment penalties

Cons

- Origination fees can be as high as 12%

- Maximum APR is relatively high at 35.99%

- Only offers 36- or 60-month terms

2. LendingClub

LendingClub is a solid choice for borrowers looking to consolidate debt. They offer a feature where they can pay your creditors directly, simplifying the consolidation process. LendingClub also allows joint applications, which can help you qualify for a larger loan amount or a better rate if your co-borrower has a strong credit profile.

3. SoFi

SoFi is an excellent option for borrowers with good to excellent credit. They offer competitive interest rates, no mandatory fees (including no origination fees or late fees), and high loan amounts up to $100,000. SoFi also provides unique member benefits, such as unemployment protection, which can pause your payments if you lose your job through no fault of your own.

4. Prosper

Prosper is a peer-to-peer lending platform that connects borrowers with individual investors. They offer loans up to $50,000 and allow joint applications. Prosper is a good option for borrowers with fair credit, as their minimum credit score requirement is typically around 600. However, they do charge origination fees, which can impact the total cost of your loan.

5. Upgrade

Upgrade is known for its accessibility, accepting borrowers with credit scores as low as 560. They offer fast funding and a variety of loan terms. Upgrade also provides free credit monitoring tools and educational resources to help borrowers improve their financial health. Like Upstart and Prosper, Upgrade charges an origination fee.

Lender Comparison Table

| Lender | APR Range | Min. Credit Score | Origination Fee | Funding Time |

|---|---|---|---|---|

| Upstart | 6.40% - 35.99% | 580 | 0% - 12% | 1 Business Day |

| LendingClub | 8.98% - 35.99% | 600 | 3% - 8% | 1-2 Business Days |

| SoFi | 8.99% - 29.99% | 680 | 0% (Optional) | 1-3 Business Days |

| Prosper | 8.99% - 35.99% | 600 | 1% - 9.99% | 1-3 Business Days |

| Upgrade | 8.49% - 35.99% | 560 | 1.85% - 9.99% | 1 Business Day |

What to use a $20K loan for

A $20,000 personal loan is highly versatile and can be used for a wide variety of purposes. Because it is an unsecured loan, the lender does not dictate exactly how you must spend the funds, giving you the flexibility to address your most pressing financial needs. Here are some of the most common and practical uses for a $20K loan.

Debt Consolidation: One of the most popular uses for a personal loan is consolidating high-interest debt, such as credit card balances. By taking out a $20,000 loan at a lower interest rate, you can pay off multiple credit cards, leaving you with a single, manageable monthly payment. This strategy can save you thousands of dollars in interest and help you become debt-free faster. For more information, check out our guide to the best personal loans for debt relief.

Home Renovation: If you are looking to upgrade your living space, a $20,000 loan can cover significant home improvement projects, such as remodeling a kitchen, updating a bathroom, or replacing a roof. Unlike a home equity loan, a personal loan for home renovation does not require you to use your house as collateral, making it a less risky option for funding upgrades.

Major Car Repairs: Unexpected vehicle breakdowns can be incredibly costly. If your car requires a new engine, transmission, or other major repairs that exceed your emergency savings, a personal loan can provide the necessary funds quickly, ensuring you can get back on the road without delay.

Medical Bills: Even with health insurance, out-of-pocket medical expenses can quickly accumulate. A $20,000 personal loan can help cover the costs of surgeries, dental work, fertility treatments, or unexpected medical emergencies, allowing you to focus on recovery rather than financial stress.

Wedding Expenses: The average cost of a wedding can easily exceed $20,000. While it is generally advisable to save for a wedding in advance, a personal loan can help bridge the gap if you need additional funds to cover venue deposits, catering, or other significant expenses for your special day. If you need more funds, you might also consider a $25,000 personal loan or a $30,000 personal loan.

How to apply step-by-step

Applying for a $20,000 personal loan is a straightforward process, especially with online lenders. By following these steps, you can streamline your application and increase your chances of approval.

Step 1: Check your credit score. Before applying, review your credit report and score to understand where you stand. This will help you identify which lenders you are most likely to qualify for and give you an idea of the interest rates you can expect. If your score is lower than desired, take steps to improve it, such as paying down existing debt or correcting any errors on your report.

Step 2: Determine your budget. Calculate how much you can afford to pay each month. Use a personal loan calculator to estimate your monthly payments based on different loan terms and interest rates. Ensure that the new loan payment fits comfortably within your monthly budget without causing financial strain.

Step 3: Prequalify with multiple lenders. Many lenders offer a prequalification process that allows you to see estimated rates and terms without affecting your credit score. This typically involves a soft credit pull. Prequalify with at least three to five lenders to compare offers and find the most competitive rate.

Step 4: Gather necessary documentation. Once you have chosen a lender, you will need to submit a formal application. Be prepared to provide documentation to verify your identity, income, and employment. Common documents include a government-issued ID, recent pay stubs, W-2 forms, and bank statements.

Step 5: Submit your application and await approval. Complete the formal application process, which will involve a hard credit inquiry that may temporarily lower your credit score by a few points. After submitting your application, the lender will review your information. If approved, carefully review the loan agreement, including the APR, fees, and repayment terms, before signing. Once you accept the loan, the funds are typically deposited into your bank account within one to three business days.

Frequently Asked Questions

- Consumer Financial Protection Bureau (CFPB). "What is a personal loan?"

- Federal Reserve. "Consumer Credit - G.19."

- Upstart. "Personal Loans." Accessed May 2026.