In This Guide

Large personal loans — generally defined as unsecured personal loans of $10,000 or more — give borrowers the financial firepower to tackle major expenses without putting up collateral. Whether you are consolidating high-interest credit card debt, financing a home renovation, covering unexpected medical bills, or funding a major life event, a large personal loan can be a cost-effective alternative to credit cards, HELOCs, or home equity loans.

The challenge is finding the right lender. APRs on large personal loans range from under 7% for well-qualified borrowers to nearly 36% for those with fair credit. Origination fees, loan terms, and minimum credit score requirements vary significantly across lenders. This guide compares the top options for 2026 and explains exactly how to qualify — including how Upstart's AI underwriting model opens the door for borrowers with fair credit scores as low as 580.

What Counts as a Large Personal Loan?

There is no official threshold, but in practice, most lenders and financial analysts consider a large personal loan to be any unsecured installment loan of $10,000 or more. The upper end of the market sits at $50,000 for most lenders, though some — like SoFi — extend up to $100,000 for highly qualified borrowers. The key distinction is that these are unsecured loans: no collateral is required, meaning your home, car, or other assets are not at risk if you default.

Large personal loans are typically used for expenses that are too big for a credit card but do not justify the complexity and risk of a secured loan. Common uses include major home renovations, debt consolidation of multiple high-interest balances, large medical or dental procedures, weddings, and business startup costs. Because they are unsecured, large personal loans carry higher interest rates than secured alternatives like HELOCs, but they fund faster and involve far less paperwork.

Best Lenders for Large Personal Loans in 2026

We evaluated the top personal loan lenders on loan amounts, APR ranges, minimum credit score requirements, origination fees, funding speed, and unique features. Here are our top picks:

Upstart — Best for Fair Credit & AI Underwriting

Upstart is our top pick for large personal loans because it uses artificial intelligence to evaluate more than just your FICO score. Its model considers education level, area of study, employment history, and income trajectory — giving borrowers with fair credit scores (580–669) a realistic path to a large loan that most traditional lenders would decline. Upstart offers loans up to $50,000 with funding as fast as one business day.

Pros

- AI underwriting considers non-traditional credit factors

- Lowest minimum credit score (580) among major lenders

- Fast funding — often 1 business day

- No prepayment penalty

- Soft credit pull for prequalification

Cons

- Origination fee up to 12% (deducted from loan proceeds)

- Only 36 or 60-month loan terms

- Higher APRs for fair credit borrowers

- No joint loan option

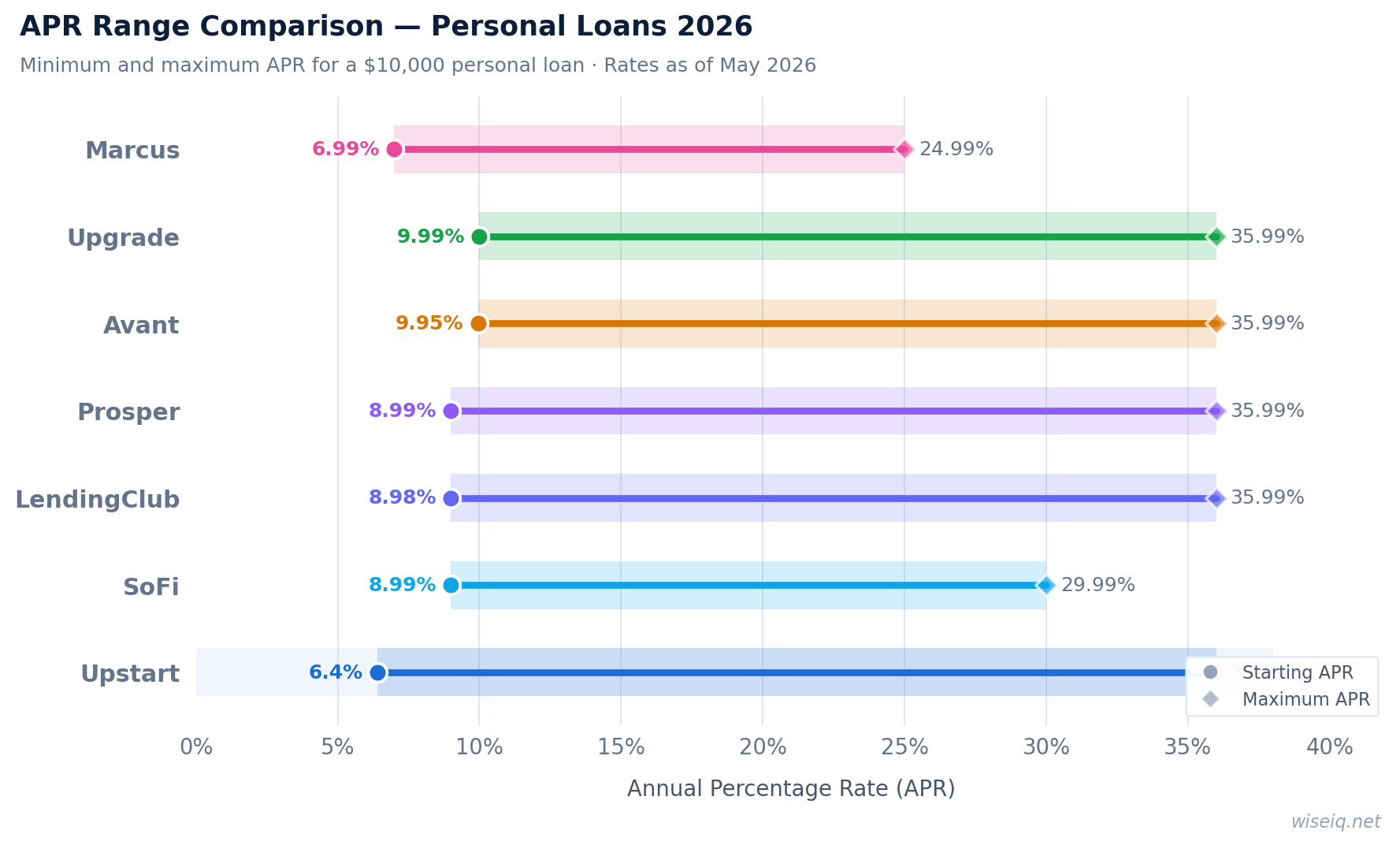

Full Lender Comparison Table

| Lender | Loan Amounts | APR Range | Min. Credit Score | Origination Fee | Funding Time |

|---|---|---|---|---|---|

| Upstart | $1,000–$50,000 | 6.40%–35.99% | 580 | 0%–12% | 1 business day |

| LendingClub | $1,000–$40,000 | 8.30%–36.00% | 600 | 3%–8% | 2–4 business days |

| SoFi | $5,000–$100,000 | 8.99%–29.99% | 680 | 0% | 1–3 business days |

| Prosper | $2,000–$50,000 | 8.99%–35.99% | 640 | 1%–9.99% | 1–3 business days |

| Upgrade | $1,000–$50,000 | 9.99%–35.99% | 580 | 1.85%–9.99% | 1–4 business days |

How to Qualify for a Large Personal Loan

Qualifying for a large personal loan requires demonstrating to the lender that you can comfortably repay the debt. Lenders evaluate several interconnected factors, and understanding each one helps you position your application for the best possible outcome.

Credit Score

Your FICO score is the starting point for most lenders. Upstart and Upgrade accept borrowers with scores as low as 580, while SoFi requires 680 and Prosper requires 640. For the best rates on a large loan, a score of 700 or higher is strongly recommended. Borrowers with 740+ typically qualify for APRs in the single digits. If your score is below 620, consider large personal loans for fair credit or a personal loan with a 580 credit score for lender-specific guidance.

Debt-to-Income Ratio (DTI)

Your debt-to-income ratio compares your total monthly debt payments to your gross monthly income. Most lenders prefer a DTI below 43%, and the best rates go to borrowers under 36%. To calculate your DTI, add up all monthly debt payments (mortgage or rent, car loans, student loans, credit card minimums, and the new loan payment) and divide by your gross monthly income. A lower DTI signals to lenders that you have sufficient cash flow to handle the new obligation without financial strain.

Income and Employment

Lenders want to see stable, verifiable income. Most require documentation such as recent pay stubs, W-2s, or tax returns. Self-employed borrowers typically need two years of tax returns. Upstart's AI model also considers your employment history and career trajectory, which can benefit recent graduates or borrowers who have recently changed jobs for a higher-paying role.

Large Personal Loans by Credit Score

Your credit score tier significantly affects both your approval odds and the APR you will receive. Here is what to expect across the main credit score ranges:

Fair Credit (580–669)

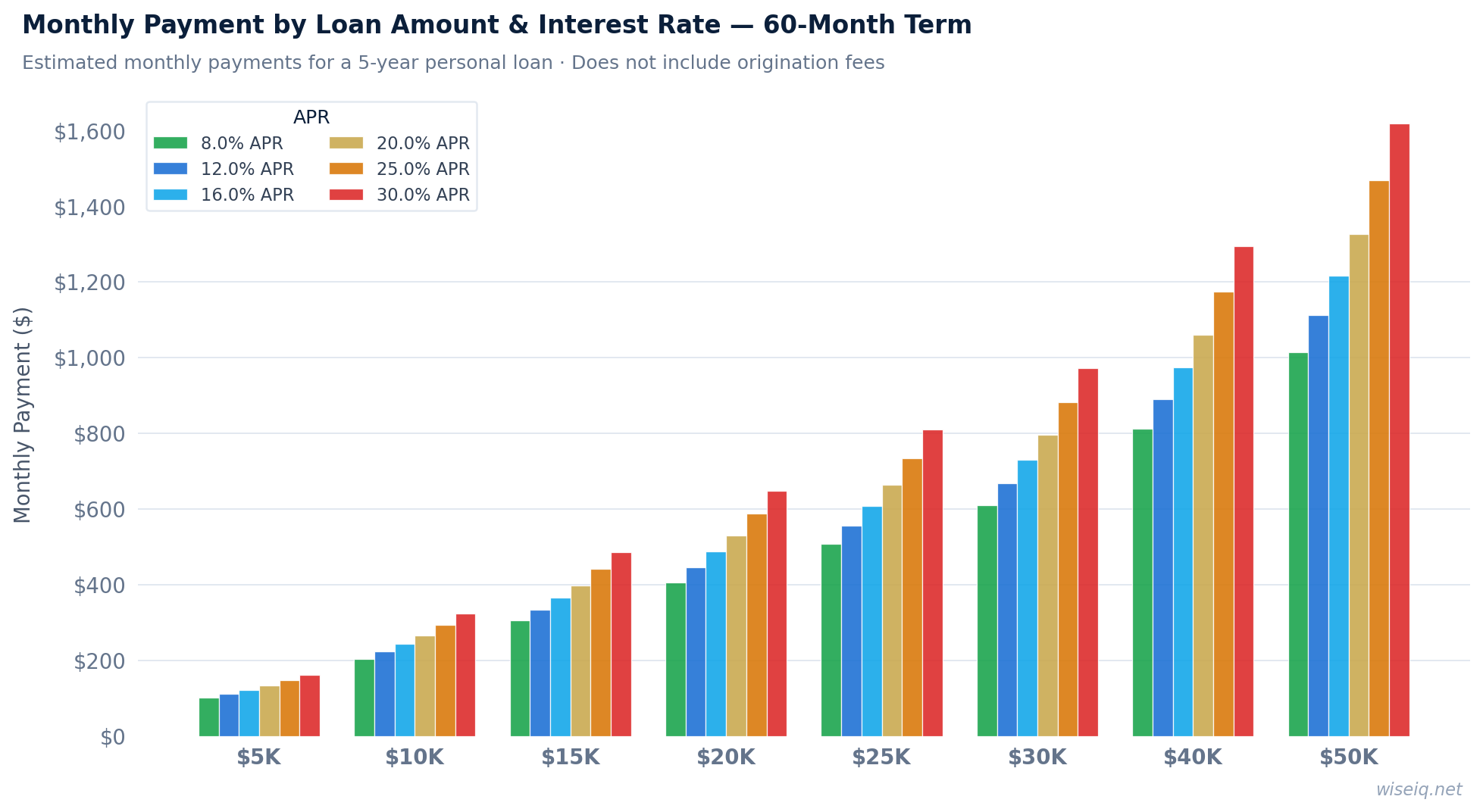

Borrowers in the fair credit range have the fewest lender options for large loans, but Upstart and Upgrade both accept 580+ scores. Expect APRs in the 20%–35% range, and origination fees at the higher end of each lender's scale. For a $20,000 loan at 25% APR over 60 months, the monthly payment is approximately $587. Explore personal loans with a 620 credit score for more detail on this tier.

Good Credit (670–739)

Good credit opens up the full lender marketplace. APRs typically fall in the 12%–20% range for this tier. LendingClub, Prosper, and Upgrade all become competitive options alongside Upstart. A $30,000 loan at 15% APR over 60 months carries a monthly payment of about $714.

Very Good to Excellent Credit (740+)

Borrowers with 740+ credit scores qualify for the lowest APRs — often 7%–12% — and have access to the full range of lenders including SoFi, which offers up to $100,000. At 8% APR over 60 months, a $50,000 loan costs approximately $1,013 per month. This tier also qualifies for the lowest origination fees or no origination fee at all (SoFi charges 0%).

Best Uses for Large Personal Loans

Large personal loans are most valuable when used for expenses that generate a return — financial, practical, or quality-of-life — that justifies the cost of borrowing. The following uses represent the strongest case for a large personal loan:

- Debt consolidation: Replacing multiple high-interest credit card balances with a single lower-rate installment loan reduces your total interest cost and simplifies repayment. See our guide to personal loans for debt consolidation.

- Home renovation: Kitchen remodels, bathroom upgrades, and additions increase your home's value and improve your living space. A $25,000 kitchen renovation can add $15,000–$20,000 in resale value. See personal loans for home renovation.

- Medical expenses: Large unexpected medical bills — surgery, fertility treatments, dental work — can be financed at a lower rate than medical credit cards. See personal loans for medical bills.

- Wedding financing: The average U.S. wedding costs $30,000. A personal loan at 12% APR is significantly cheaper than carrying the balance on a credit card at 22%+. See personal loans for weddings.

- Business startup: For borrowers who cannot qualify for a business loan, a personal loan can fund initial inventory, equipment, or working capital.

How a Large Personal Loan Affects Your Credit Score

Taking out a large personal loan has both short-term and long-term effects on your credit profile. Understanding these effects helps you time your application strategically and manage your credit during repayment.

Short-Term: Hard Inquiry and New Account

When you formally apply for a personal loan, the lender performs a hard credit inquiry, which typically reduces your FICO score by 2–5 points. This effect is temporary and usually disappears within 12 months. Opening a new account also lowers your average account age, which can cause a small additional dip. Most lenders offer a soft credit pull for prequalification — use this to compare rates before committing to a hard inquiry.

Long-Term: Payment History and Credit Mix

Payment history is the single largest factor in your FICO score (35%). Making every payment on time on a large personal loan builds a strong positive payment history that compounds over the life of the loan. Adding an installment loan also diversifies your credit mix — if you previously only had revolving credit (credit cards), adding an installment loan can improve your score over time.

Large Personal Loan vs. HELOC vs. Home Equity Loan

When you need a large sum of money, three common options compete: an unsecured personal loan, a home equity line of credit (HELOC), and a home equity loan. Each has distinct trade-offs:

| Feature | Large Personal Loan | HELOC | Home Equity Loan |

|---|---|---|---|

| Collateral | None (unsecured) | Your home | Your home |

| Interest rate | Fixed, 6.40%–35.99% | Variable, typically 7%–12% | Fixed, typically 7%–10% |

| Funding speed | 1–3 business days | 2–6 weeks | 2–4 weeks |

| Risk if you default | Credit damage only | Foreclosure risk | Foreclosure risk |

| Home equity required | No | Yes (15–20%+) | Yes (15–20%+) |

| Best for | Fast funding, no home equity, debt consolidation | Ongoing expenses, flexible draw | Large one-time expense, lower rate |

The personal loan wins on speed and safety. The HELOC and home equity loan win on interest rate — but only if you have sufficient home equity and are comfortable using your home as collateral. For borrowers who rent, have limited equity, or need funds in days rather than weeks, a large personal loan is the clear choice.