Table of Contents

Planning a wedding is an exciting journey, but it often comes with significant financial considerations. A personal loan for wedding expenses can be a viable option for couples looking to finance their special day without draining their savings or relying on high-interest credit cards. This guide explores whether a wedding loan is right for you, breaks down average wedding costs in 2026, and provides insights into securing the best rates.

WiseIQ is committed to helping you make informed financial decisions. We’ve researched top lenders and compiled essential information to help you navigate the complexities of wedding financing. Whether you need to cover a venue deposit, catering costs, or even honeymoon financing, understanding your options is the first step towards a stress-free celebration.

Upstart Personal Loans for Weddings

Upstart stands out as a top lender for wedding loans, offering competitive rates and a unique AI-powered underwriting process that considers more than just your credit score. This can be particularly beneficial for those with limited credit history but strong educational and employment backgrounds.

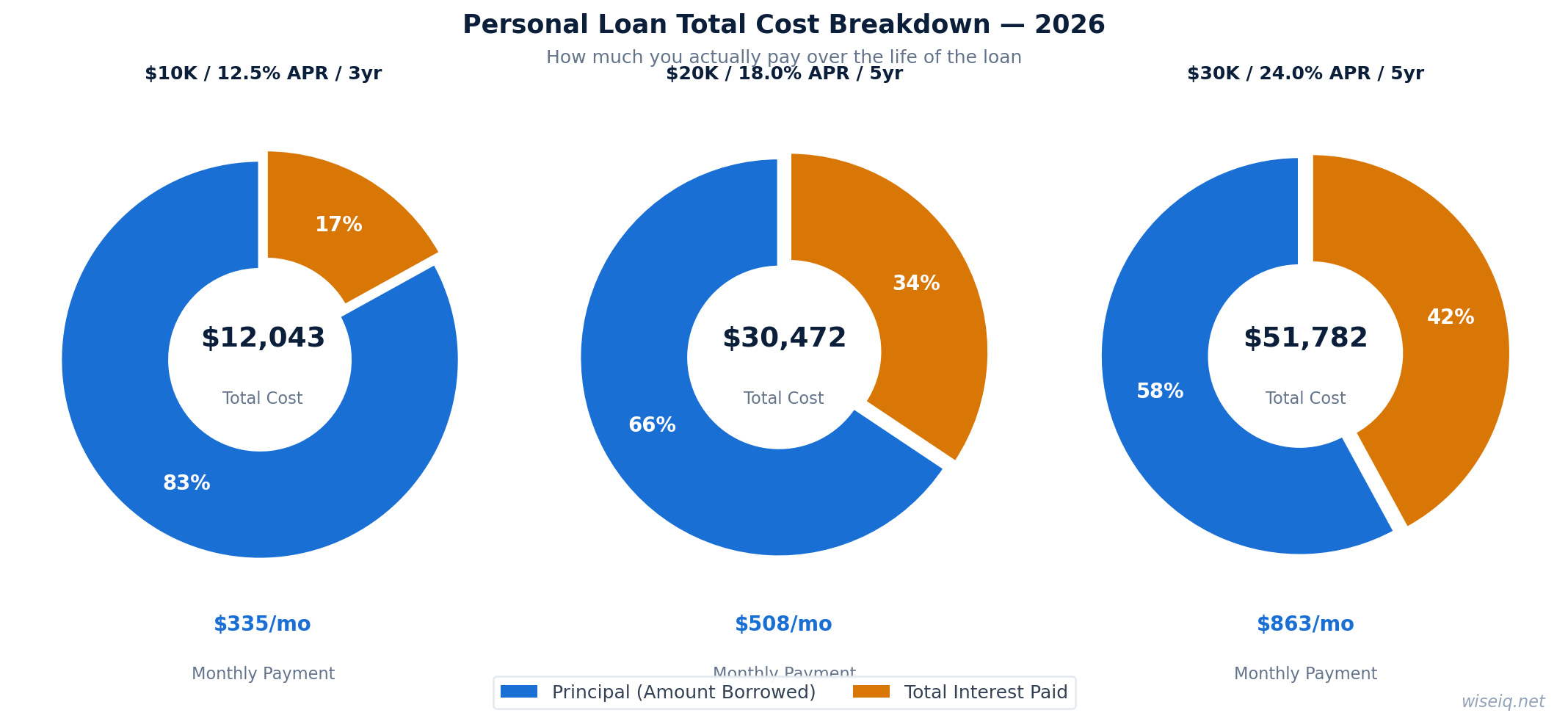

Should you take a personal loan for your wedding?

Deciding whether to take out a personal loan for your wedding is a significant financial decision that requires careful consideration. While a wedding loan can provide the necessary funds to create your dream day, it’s essential to weigh the benefits against the potential drawbacks. A personal loan offers predictable monthly payments and a fixed interest rate, making it easier to budget and plan for repayment. This can be particularly appealing if you want to avoid the high-interest rates often associated with credit cards or prefer not to ask family for financial assistance.

However, taking on debt for a wedding means starting your married life with a financial obligation. It’s crucial to ensure that the monthly payments are manageable within your budget and that you have a solid plan for repayment. Consider your current financial situation, your credit score, and the overall cost of the loan, including any origination fees. Exploring all your wedding financing options will help you make the best choice for your future.

Average wedding costs in 2026

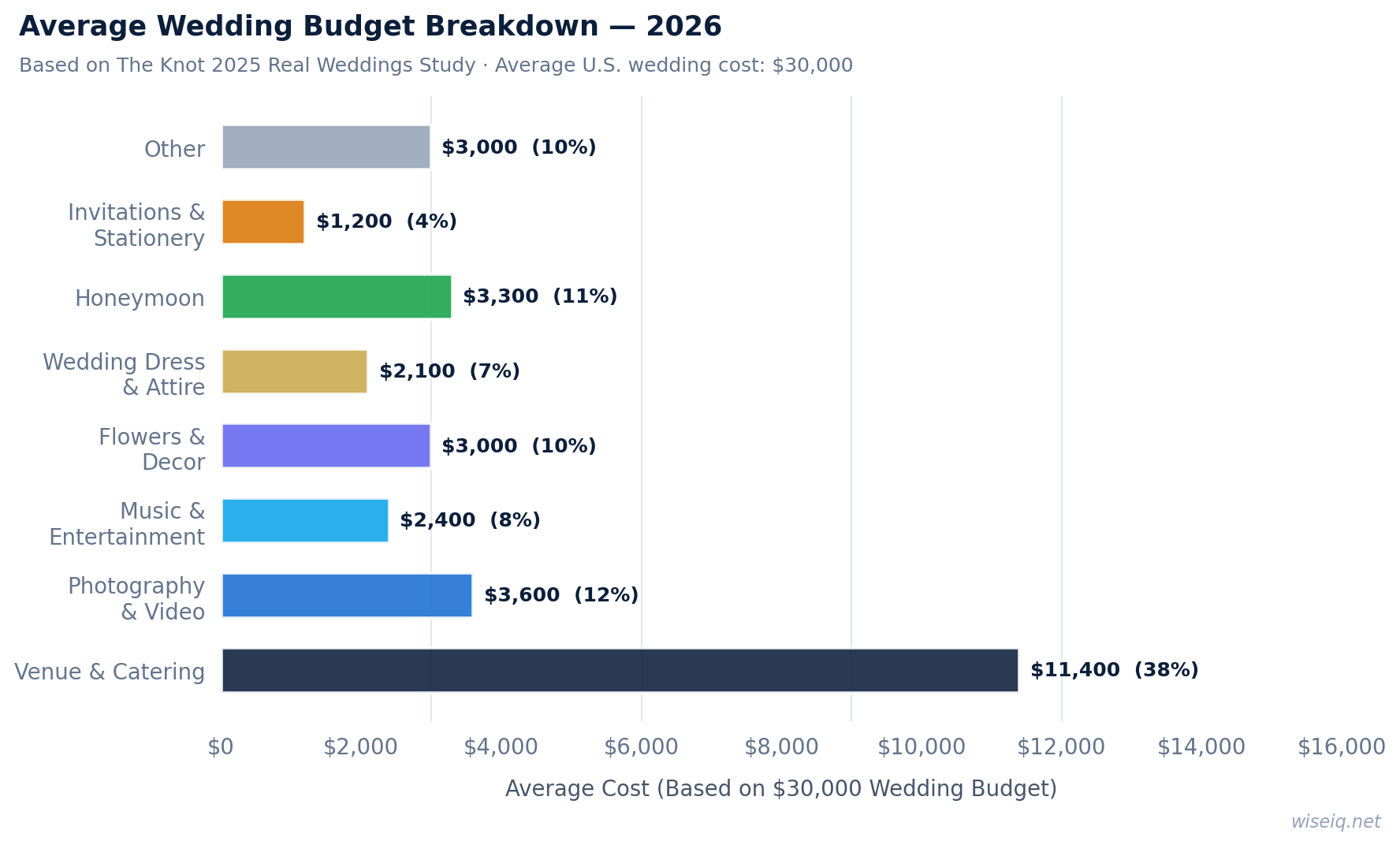

Understanding the average wedding costs in 2026 can help you set a realistic wedding budget and determine how much you might need to borrow. The national average cost for a wedding is projected to be around $30,000, but this can vary significantly based on location, guest count, and personal preferences. Key expenses typically include the venue, catering, photography, and attire.

| Category | Average Cost (2026) |

|---|---|

| National Average Wedding | $30,000 |

| Venue | $12,000 |

| Catering (per person) | $8,000 (total, based on average guest count) |

| Photography | $3,000 |

| Wedding Dress | $2,000 |

| Wedding Planner | $1,500 - $5,000 |

| Music (DJ/Band) | $1,000 - $4,000 |

| Flowers | $1,000 - $3,000 |

| Rings | $5,000 - $10,000+ |

| Honeymoon | $3,000 - $10,000+ |

These figures are averages, and your actual costs may be higher or lower. For instance, a lavish wedding in a major city will likely exceed the national average, while a more intimate celebration could cost less. When considering a bridal loan, factor in all potential expenses, including unexpected ones, to ensure you borrow an adequate amount.

Best wedding loan lenders — Upstart #1

When seeking the best personal loan for wedding expenses, it ’s crucial to compare various lenders. Upstart consistently ranks as a top choice due to its innovative approach to underwriting. Unlike traditional lenders that primarily focus on credit scores, Upstart considers factors like education, employment history, and area of study, which can be advantageous for individuals with limited credit history but strong earning potential.

Upstart offers competitive APRs and loan amounts ranging from $1,000 to $50,000, making it suitable for a wide range of wedding budgets. Their fast funding process, often as quick as one business day, can be a lifesaver for last-minute expenses or unexpected costs. Additionally, Upstart has no prepayment penalties, allowing you to save on interest if you can pay off your loan early. This flexibility, combined with their transparent fee structure, makes Upstart a strong contender for your wedding financing needs.

How to qualify

Qualifying for a personal loan for wedding expenses typically involves meeting certain criteria set by lenders. While requirements can vary, most lenders look for a combination of a good credit score, stable income, and a manageable debt-to-income ratio. For a lender like Upstart, a minimum credit score of 580 is generally required, but their AI-powered model allows for a more holistic review of your financial profile.

To improve your chances of qualification, consider the following:

- Check your credit score: Before applying, obtain your credit report and score. Address any inaccuracies and work on improving your score if it's below the lender's minimum.

- Stable employment: Lenders prefer borrowers with a consistent employment history and a reliable source of income, demonstrating your ability to repay the loan.

- Debt-to-income ratio: A lower debt-to-income ratio indicates that you have less existing debt relative to your income, making you a less risky borrower.

- Co-signer: If your credit history is limited or your score is not ideal, a co-signer with good credit can significantly improve your chances of approval and potentially secure a lower interest rate.

Remember that each lender has unique criteria, so it's wise to pre-qualify with multiple lenders to compare offers without impacting your credit score.

Wedding loan vs credit card vs family loan comparison

When considering how to finance your wedding, it's essential to compare a personal loan for wedding expenses with other common options like credit cards and family loans. Each method has distinct advantages and disadvantages that can impact your financial well-being.

| Feature | Personal Wedding Loan | Credit Card | Family Loan |

|---|---|---|---|

| Interest Rates | Fixed, generally lower than credit cards | Variable, often very high | Often 0% or low interest, flexible |

| Repayment Terms | Fixed monthly payments over a set period (e.g., 3-5 years) | Minimum payments, can lead to long-term debt | Flexible, can be informal or structured |

| Impact on Credit | Can improve credit with on-time payments; hard inquiry upon application | Can negatively impact credit if balances are high; high utilization hurts score | No direct impact on credit score |

| Fees | Origination fees, late payment fees | Annual fees, late payment fees, balance transfer fees | Typically no fees |

| Relationship Impact | Professional transaction | Professional transaction | Can strain personal relationships if not repaid |

| Funding Speed | Relatively fast (1-5 business days) | Instant access to credit limit | Immediate, depending on family's liquidity |

A personal loan offers a structured repayment plan and often lower interest rates than credit cards, making it a more predictable option for wedding financing. Credit cards can be tempting for their immediate access to funds, but their high variable interest rates can quickly lead to accumulating debt. Borrowing from family can offer flexibility and lower costs, but it carries the risk of straining personal relationships if repayment terms are not clear or met.

Tips to reduce wedding costs while still borrowing smart

Even with a personal loan for wedding expenses, finding ways to reduce overall costs can significantly ease your financial burden. Smart budgeting and strategic planning can help you create a memorable day without overspending. Here are some tips:

- Prioritize your spending: Identify the most important aspects of your wedding and allocate a larger portion of your budget to those areas. Cut back on less critical elements.

- Consider off-peak dates: Venues and vendors often offer lower rates during off-peak seasons or on weekdays.

- Reduce the guest list: A smaller guest list directly translates to lower costs for catering, invitations, and favors.

- DIY elements: Consider taking on some tasks yourself, such as creating invitations, decorations, or even baking your own cake, to save on vendor costs.

- Shop around for vendors: Get multiple quotes for every service, from photographers to florists, to ensure you're getting the best value.

- Negotiate: Don't be afraid to negotiate prices with vendors. Many are willing to work within your budget.

- Borrow only what you need: If you opt for a bridal loan, borrow only the amount necessary to cover your expenses. Avoid borrowing extra for non-essential items.

- Understand loan terms: Fully comprehend the interest rate, repayment schedule, and any fees associated with your wedding loan to avoid surprises.

By implementing these strategies, you can manage your wedding budget effectively and ensure your personal loan for wedding financing is used wisely.

Frequently Asked Questions about Wedding Loans

Should I take out a personal loan for my wedding?

A personal loan for your wedding can be a good option if you have a clear repayment plan and a good credit score to secure favorable rates. It allows you to consolidate wedding expenses into one predictable monthly payment.

What are the average wedding costs in 2026?

In 2026, the national average cost for a wedding is around $30,000. Major expenses include venue ($12,000), catering ($8,000), photography ($3,000), and the wedding dress ($2,000).

How can I qualify for a wedding loan?

To qualify for a wedding loan, lenders typically look for a good credit score (often 580+), a stable income, and a low debt-to-income ratio. Some lenders, like Upstart, also consider education and employment history.

What are the alternatives to a wedding loan?

Alternatives to a wedding loan include using credit cards, borrowing from family, or saving up. Each has pros and cons regarding interest rates, repayment terms, and impact on relationships.

How can I reduce wedding costs while still borrowing smart?

To reduce wedding costs, consider off-peak dates, smaller guest lists, or DIY elements. When borrowing, compare rates from multiple lenders, understand all fees, and borrow only what you truly need.