Debt consolidation and bankruptcy are both legitimate paths out of overwhelming debt — but they work very differently and have very different long-term consequences. The right choice depends on your total debt amount, your income, and how quickly you need relief.

The avalanche method (paying highest-interest debt first) saves the most money mathematically. The snowball method (smallest balance first) works better for motivation. Choose the one you will actually stick with.

| Factor | Debt Consolidation | Bankruptcy (Chapter 7) | Bankruptcy (Chapter 13) |

|---|---|---|---|

| Credit Score Impact | 5–10 points (temporary) | 130–240 points for 10 years | 130–200 points for 7 years |

| Debt Eliminated | No — restructured | Yes — most unsecured debt | Partial — repayment plan |

| Timeline | 3–5 years to pay off | 3–6 months | 3–5 year repayment plan |

| Cost | Interest on new loan | $1,500–$3,500 attorney fees | $3,000–$5,000 attorney fees |

| Income Requirement | Yes — need to qualify for loan | No (but means test applies) | Yes — need steady income |

| Public Record | No | Yes — permanent public record | Yes — permanent public record |

| Asset Protection | N/A | May lose non-exempt assets | Keep assets; repay over time |

| Best For | Manageable debt with steady income | Overwhelming debt, no income | Overwhelming debt, steady income |

💡 Start With a Free Consultation

Before deciding between consolidation and bankruptcy, get a free consultation from a nonprofit credit counseling agency (NFCC member) or a bankruptcy attorney. Many offer free 30-minute consultations. This is the most important step — the right path depends entirely on your specific numbers.

When to Choose Debt Consolidation

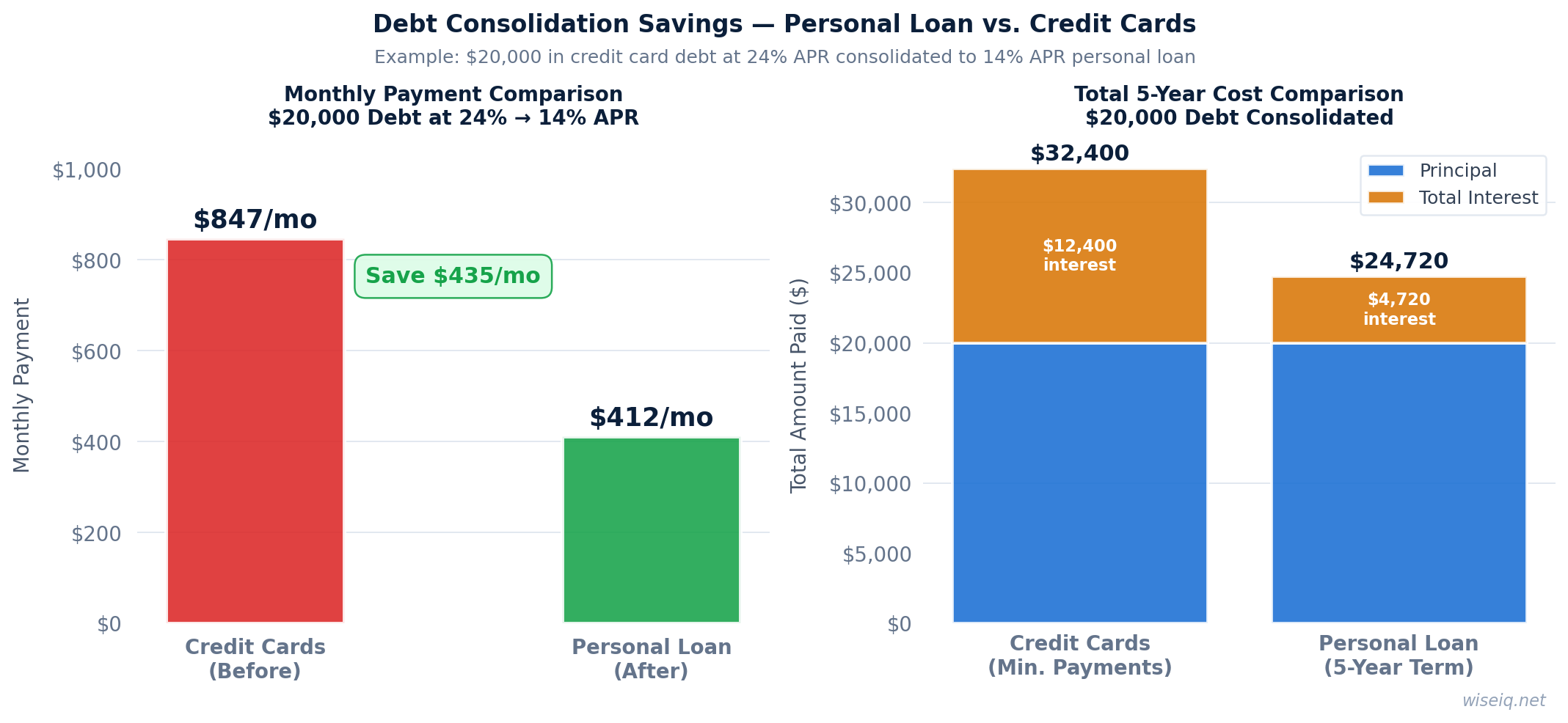

Debt consolidation is the right choice when your total unsecured debt is manageable (under $50,000), you have steady income that can cover a consolidation loan payment, and your credit score is high enough to qualify for a rate lower than your current average. The goal is to simplify multiple payments into one and reduce the total interest you pay.

SoFi Personal Loan — Best for Debt Consolidation (Good Credit)

Upstart — Best for Debt Consolidation (Fair/Bad Credit)

National Debt Relief — Best for Debt Settlement

Related Articles & Guides

Frequently Asked Questions

Is debt consolidation better than bankruptcy?

How much debt do you need to file bankruptcy?

Does debt consolidation hurt your credit?

How long does debt consolidation take?

Can I consolidate debt with bad credit?

Sources & Methodology

WiseIQ's editorial team researches and fact-checks all content using primary sources. Our recommendations are based on independent analysis and are not influenced by advertiser relationships.

- Consumer Financial Protection Bureau (CFPB)

- Federal Reserve — Consumer Credit Report (G.19)

- myFICO Credit Education

- Issuer and lender websites — rates, terms, and eligibility verified directly from source

Last reviewed: April 3, 2026 | How we rank products