When considering a personal loan, comparing options from different lenders is crucial. This guide provides a detailed Upstart vs Achieve comparison for 2026, helping you understand the nuances of each platform. Both Upstart and Achieve offer personal loans that can be used for various purposes, including debt consolidation, home improvements, or unexpected expenses. However, their approaches to lending, eligibility requirements, and overall borrower experience differ significantly. We\'ll delve into their interest rates, origination fees, approval odds, and funding speed to help you determine which is better for your financial situation.

Expert Tip: Always prequalify with multiple lenders to compare personalized offers without impacting your credit score. This allows for a true interest rate comparison and helps you find the most favorable terms.

Upstart Personal Loans: An AI-Driven Approach

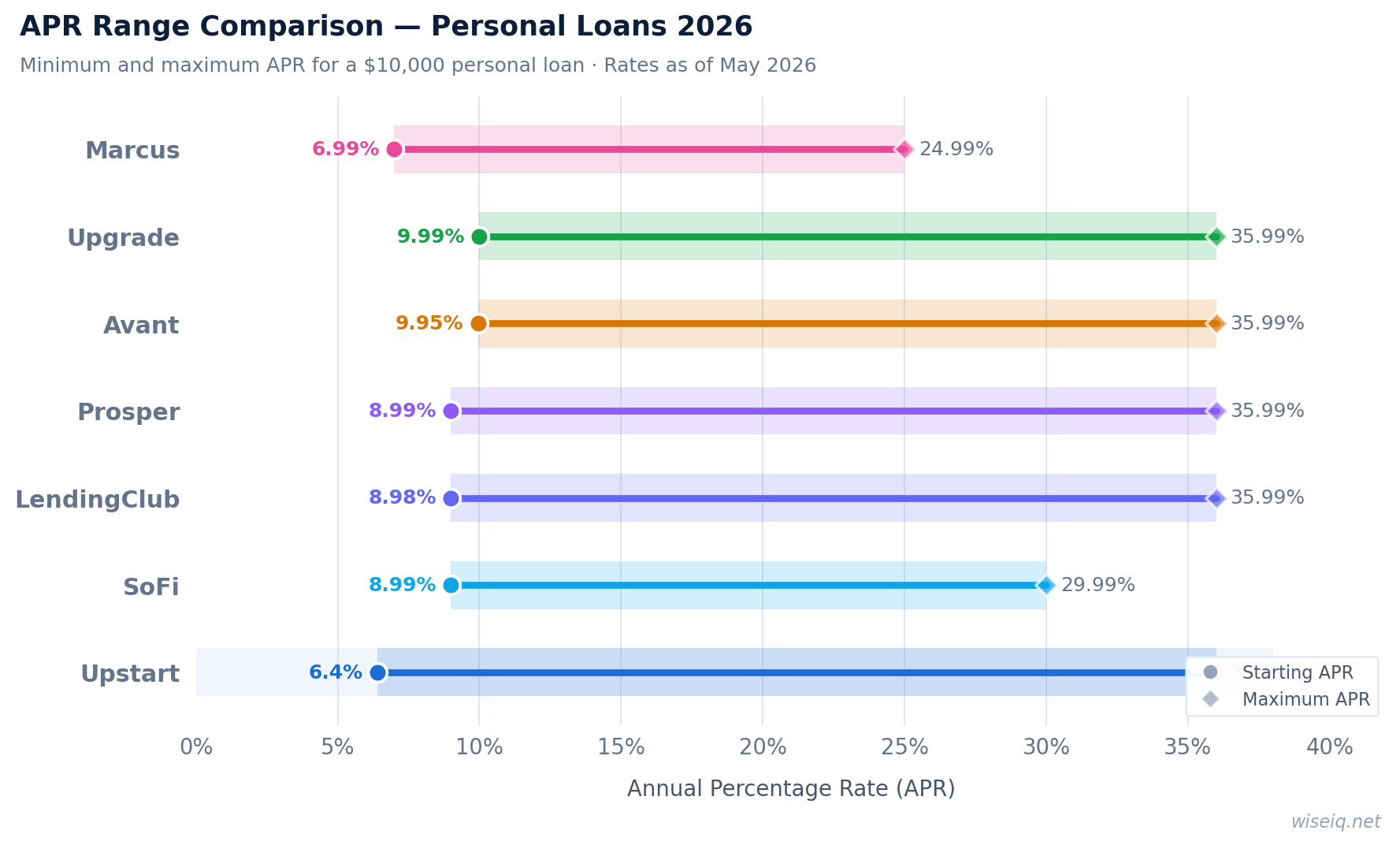

Upstart stands out in the personal loan market due to its innovative use of AI underwriting. Unlike traditional lenders that rely heavily on FICO scores, Upstart considers a broader range of factors, including your education, employment history, and area of study. This approach can be particularly beneficial for younger borrowers or those with a limited credit history who might otherwise struggle to qualify for competitive rates. Upstart offers loans from $1,000 to $50,000 with an annual percentage rate (APR) ranging from 6.40% to 35.99%. Their origination fee can be anywhere from 0% to 12%, depending on your credit profile. A key advantage is the absence of a prepayment penalty, giving borrowers flexibility to pay off their loan early and save on interest.

How Upstart Works: Step-by-Step

1. Check Your Rate

Complete a short online form for a soft credit pull that won\'t affect your credit score. Get personalized offers in minutes.

2. Choose Your Loan

Review various loan options, terms, and monthly payment amounts. Select the offer that best fits your budget.

3. Verify Information

If you accept an offer, you\'ll undergo a hard credit inquiry and may need to provide documentation to verify your income and identity.

4. Receive Funds

Once approved, funds are often disbursed as early as the next business day, providing quick access to cash.

Achieve Personal Loans: Debt Consolidation Specialist

Achieve, formerly known as FreedomPlus, positions itself as a debt consolidation specialist, though its personal loans can be used for other purposes as well. Achieve personal loan offerings are particularly strong for those looking to manage existing debt more effectively. They often provide a direct creditor payoff option, simplifying the debt consolidation process by sending funds directly to your creditors. Achieve offers loans from $5,000 to $50,000, with APRs ranging from 8.99% to 35.99%. Their origination fee is typically included in the APR. Achieve also stands out for its potential to offer a co-borrower option, which can improve approval odds and secure better rates for applicants with less-than-perfect credit. While not as focused on non-traditional credit factors as Upstart, Achieve still considers a holistic view of your financial health.

Upstart vs Achieve: A Head-to-Head Comparison

To help you decide which is better, let\'s break down the key differences between Upstart and Achieve across several critical categories. This head-to-head comparison will highlight their strengths and weaknesses, focusing on aspects like interest rate comparison, approval odds, origination fee comparison, and funding speed.

Rates verified May 2026

| Feature | Upstart | Achieve |

|---|---|---|

| APR Range | 6.40%–35.99% | 8.99%–35.99% |

| Loan Amounts | $1,000–$50,000 | $5,000–$50,000 |

| Origination Fee | 0%–12% | Included in APR |

| Minimum Credit Score | No stated minimum (AI underwriting) | Typically 620+ recommended |

| Funding Speed | As early as next business day | Typically 1-3 business days |

| Prequalification | Yes (soft credit pull) | Yes (soft credit pull) |

| Co-borrower Option | No | Yes |

| Specialization | AI-driven, broader eligibility | Debt consolidation specialist |

| BBB Rating | A- (as of May 2026) | A+ (as of May 2026) |

| Trustpilot Score | Excellent (4.8/5) | Excellent (4.6/5) |

Interest Rates and Fees: A Deeper Dive

When evaluating personal loans, the annual percentage rate (APR) is arguably the most critical factor, as it represents the total cost of borrowing, including interest and fees. Upstart advertises a starting APR of 6.40%, which is notably lower than Achieve\'s 8.99%. This difference can translate to significant savings over the life of a loan, especially for well-qualified borrowers. However, it\'s important to remember that these are starting rates, and the actual APR you receive will depend on your creditworthiness, loan term, and other factors. Both lenders have a maximum APR of 35.99%, which is common for personal loans and often applies to borrowers with lower credit scores or higher perceived risk. The origination fee is another key component of the total cost. Upstart\'s origination fee can range from 0% to 12%, deducted from the loan proceeds. Achieve\'s origination fees are typically factored into the APR, meaning you won\'t see a separate deduction but it\'s still part of your overall cost. Always use the APR for an accurate interest rate comparison between the two lenders.

Approval Odds and Eligibility: Who Qualifies?

The eligibility criteria and approval odds are where Upstart and Achieve diverge significantly. Upstart\'s innovative AI underwriting model is a game-changer for many. By analyzing factors beyond just your FICO score, such as your education, employment history, and even your field of study, Upstart can offer loans to individuals who might be overlooked by traditional lenders. This makes Upstart particularly appealing for recent graduates, those with limited credit history, or individuals who have improved their financial standing but whose credit score hasn\'t yet caught up. While there\'s no strict minimum credit score requirement, successful applicants often have a fair credit score or better. Achieve, on the other hand, tends to cater to a slightly more traditional borrower profile, typically recommending a minimum credit score of 620 or higher. However, Achieve offers a valuable co-borrower option, allowing you to apply with another person to improve your approval odds and potentially secure a lower interest rate. This can be a significant advantage for those with a lower credit score or a higher debt-to-income ratio. Both lenders offer prequalification with a soft credit pull, which is a risk-free way to gauge your approval odds and see potential loan offers without impacting your credit score.

Funding Speed and Loan Use Cases

When you need funds quickly, funding speed becomes a critical consideration. Upstart is renowned for its efficiency, often disbursing funds as early as the next business day after final approval. This rapid funding can be a lifesaver for unexpected expenses or time-sensitive financial needs. Achieve also offers competitive funding speed, typically getting funds to borrowers within one to three business days. For those specifically seeking a debt consolidation specialist, Achieve truly shines. They offer a direct creditor payoff option, where they send funds directly to your creditors, simplifying the debt consolidation process and ensuring your old accounts are paid off efficiently. While both lenders offer personal loans for a variety of purposes, including medical bills, home repairs, or major purchases, Achieve\'s specialized focus on debt consolidation makes it a strong contender for borrowers whose primary goal is to streamline and manage their existing debts. Upstart\'s flexibility in considering non-traditional credit factors also makes it suitable for a wider range of personal loan needs.

Which is Better: Upstart or Achieve for Your Financial Goals?

The ultimate decision of which is better, Upstart or Achieve, hinges on your unique financial situation and borrowing needs. If you are a borrower with a strong educational background and stable employment but a limited or fair credit history, Upstart\'s AI underwriting model could provide you with access to competitive rates that traditional lenders might not offer. Their quick funding speed is also a major plus if you need cash fast. Upstart\'s transparency regarding its 0%–12% origination fee, along with no prepayment penalty, adds to its appeal for many borrowers seeking flexibility.

Conversely, if your primary objective is debt consolidation, Achieve personal loan services are highly specialized and effective. Their direct creditor payoff feature can simplify the process of managing multiple debts, and the co-borrower option can significantly improve your chances of approval and secure better terms, especially if you have a lower credit score or a high debt-to-income ratio. Achieve\'s strong customer service reputation, reflected in its BBB rating and Trustpilot score, also provides an added layer of confidence.

Before making a decision, it is highly recommended to utilize the prequalification processes offered by both lenders. This allows you to compare personalized annual percentage rate offers, loan terms, and monthly payment estimates without undergoing a hard credit inquiry that could impact your FICO score. Consider all semantic terms discussed, such as origination fee, loan term, and approval odds, to make a truly informed choice. Whether you prioritize a unique underwriting model or specialized debt relief solutions, both Upstart and Achieve offer valuable personal loan options in 2026.

Related Personal Loan Guides

About the WiseIQ Editorial Team

Our team of financial experts is dedicated to providing unbiased, accurate, and actionable advice to help you make smarter financial decisions. We meticulously research and compare financial products to bring you the most relevant information.

Frequently Asked Questions About Upstart vs Achieve

What is the main difference between Upstart and Achieve personal loans?

The primary difference lies in their underwriting models. Upstart uses AI underwriting, considering education and employment history in addition to traditional credit factors, which can benefit borrowers with limited credit history. Achieve personal loan focuses more on traditional credit metrics and specializes in debt consolidation, often offering direct creditor payoff options.

Which lender offers better interest rates: Upstart or Achieve?

Upstart\'s APRs range from 6.40% to 35.99%, while Achieve\'s range from 8.99% to 35.99%. Upstart generally offers a lower starting APR, but the actual rate you receive from either lender depends on your creditworthiness and other factors. It\'s crucial to prequalify with both to compare personalized interest rate comparison offers.

Can I get a personal loan from Upstart or Achieve with bad credit?

Upstart is known for its AI underwriting, which can make it more accessible for borrowers with fair credit or limited credit history, as it considers non-traditional credit factors. Achieve also serves a range of credit profiles, but typically looks for a more established credit history. Approval odds vary, and a soft credit pull can help you check without impacting your score.

Do Upstart or Achieve charge origination fees?

Yes, both Upstart and Achieve charge origination fees. Upstart\'s origination fee typically ranges from 0% to 12% of the loan amount. Achieve also charges an origination fee, which is factored into the APR. An origination fee comparison is essential when evaluating the total cost of the loan.

How quickly can I get funding from Upstart vs Achieve?

Upstart is known for its next-day funding, with many borrowers receiving funds as early as one business day after approval. Achieve also offers competitive funding speed, often within a few business days, especially for debt consolidation loans where they can perform a direct creditor payoff.

Which lender has a better BBB rating and Trustpilot score?

Both Upstart and Achieve generally maintain good reputations. Their BBB rating and Trustpilot score can fluctuate, so it\'s advisable to check the most current ratings directly on the respective platforms. These scores reflect customer satisfaction and transparency, offering insight into which is better for customer service.

What are the loan terms available for Upstart and Achieve?

Upstart typically offers loan terms of 3 or 5 years. Achieve offers a wider range of loan terms, often from 24 to 60 months (2 to 5 years), providing more flexibility in monthly payment options. The loan term you choose will impact your monthly payment and the total interest paid over the life of the loan.

Do either Upstart or Achieve have a prepayment penalty?

No, neither Upstart nor Achieve charge a prepayment penalty. This means you can pay off your loan early without incurring any additional fees, which can save you a significant amount in interest over the loan term. This flexibility is a key benefit for borrowers looking to manage their debt efficiently.

How does a soft credit pull differ from a hard credit inquiry?

A soft credit pull, used during prequalification, allows lenders to view your credit report without impacting your credit score. It\'s a way to check your potential rates and approval odds risk-free. A hard credit inquiry, on the other hand, occurs when you formally apply for a loan and can temporarily lower your credit score by a few points. Both Upstart and Achieve use soft credit pulls for initial checks.

Disclaimer: The information provided on WiseIQ is for educational purposes only and should not be considered financial advice. Always consult with a qualified financial professional before making any financial decisions. Loan terms and availability are subject to change and depend on individual creditworthiness.