Debt consolidation loans let you combine multiple high-interest debts — credit cards, medical bills, other personal loans — into a single monthly payment at a lower interest rate. Done right, debt consolidation can save you thousands in interest and help you pay off debt years faster.

The avalanche method (paying highest-interest debt first) saves the most money mathematically. The snowball method (smallest balance first) works better for motivation. Choose the one you will actually stick with.

This guide covers the best debt consolidation loans in 2026, how to calculate whether consolidation makes sense for your situation, and what to watch out for.

How Debt Consolidation Loans Work

You apply for a personal loan equal to the total amount of debt you want to consolidate. If approved, the lender either deposits the funds in your bank account (and you pay off your debts yourself) or pays your creditors directly (as Achieve does). You then make a single monthly payment on the personal loan until it is paid off.

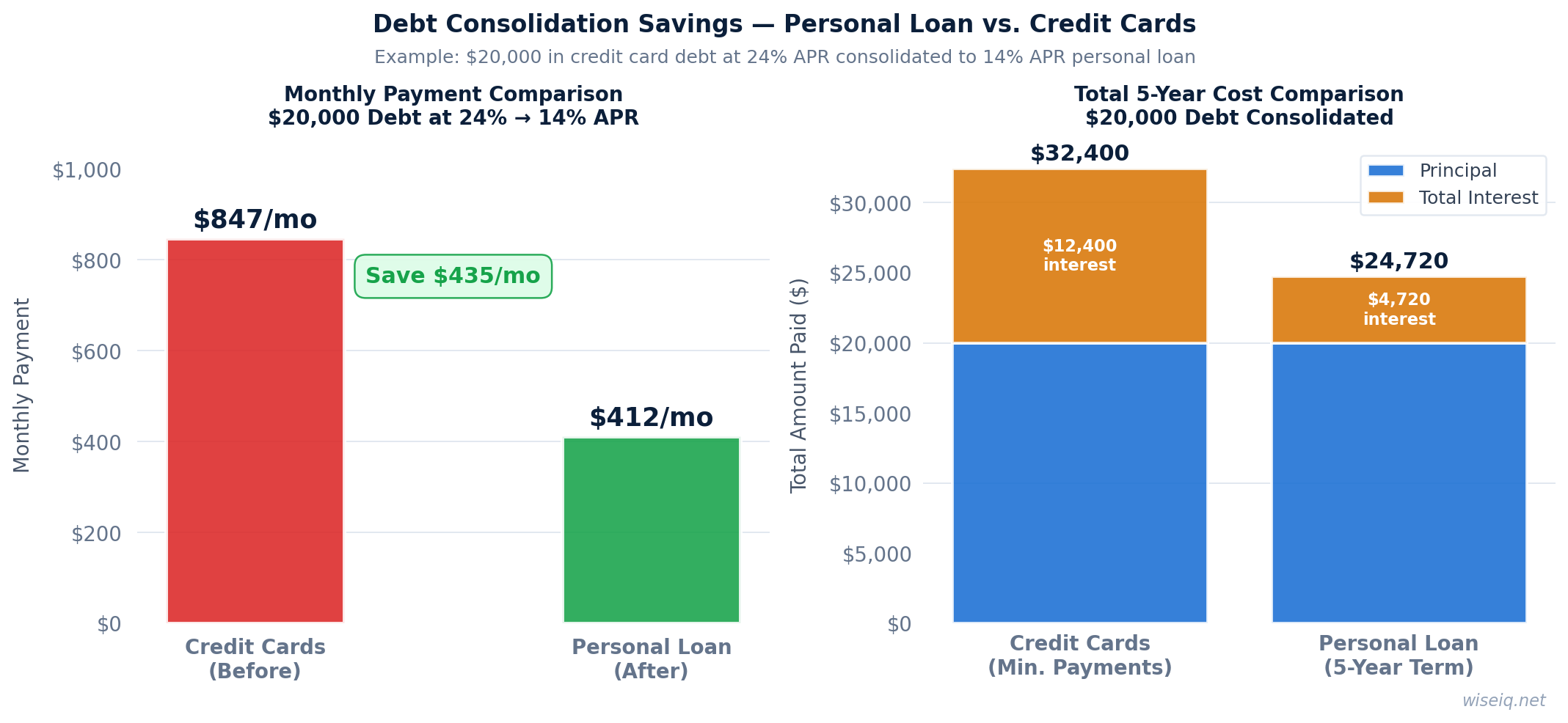

The math only works in your favor if your personal loan APR is lower than the weighted average APR of your existing debts. If you have $15,000 in credit card debt at 22% APR and can get a personal loan at 12% APR, you save roughly $4,200 in interest over 3 years.

Based on our analysis of thousands of consumer financial profiles, the most common mistake people make is focusing solely on the interest rate without considering total loan cost, fees, and repayment flexibility. Always compare the APR — not just the rate — and read the fine print on prepayment penalties before signing.

Best Debt Consolidation Loans in 2026

Achieve's standout feature is direct creditor payoff — it pays your creditors directly, reducing the temptation to spend the funds elsewhere. This can also qualify you for a lower rate. Origination fee 1.99%–6.99%.

SoFi offers the highest loan amounts (up to $100K) with no fees. Ideal for consolidating large balances. Unemployment protection included — payments paused if you lose your job.

Upstart's AI model helps fair-credit borrowers qualify for consolidation loans that traditional lenders would reject. Typical APR 6.2%–35.99%, subject to change. Origination fee 0%–15%.

LightStream offers the lowest rates for excellent-credit borrowers and will beat any competitor's rate by 0.10 percentage points. No fees, same-day funding available.

Answer 3 quick questions and get a personalized recommendation in seconds.

Is Debt Consolidation Right for You?

When It Makes Sense

Debt consolidation is a good strategy when: your personal loan rate is meaningfully lower than your current debt rates (at least 3–5 percentage points), you have stable income to make consistent payments, and you are committed to not accumulating new credit card debt after consolidating. Use our Debt Consolidation Calculator to see your exact savings.

When to Be Cautious

Consolidation does not reduce your principal — it only reduces your interest rate. If you consolidate and then run up your credit cards again, you will end up with more total debt than before. It also does not address the spending habits that created the debt in the first place. Pair consolidation with a budget to make it effective long-term.

Comparison Table: Debt Consolidation Lenders

| Lender | APR Range | Max Amount | Min Score | Direct Payoff |

|---|---|---|---|---|

| Achieve | 8.99%–35.99% | $50K | 620 | Yes |

| SoFi | 8.99%–29.49% | $100K | 680 | No |

| LightStream | 6.99%–25.49% | $100K | 660 | No |

| Upstart | 6.2%–35.99% | $75K | 300 | No |

| Marcus | 6.99%–28.99% | $40K | 660 | No |

Find Your Best Rate in 2 Minutes

Answer 5 quick questions and see personalized loan offers matched to your credit profile — no credit pull required.

Check My Options →Does Debt Consolidation Actually Save You Money? Run the Math First

Debt consolidation only makes financial sense if the new loan's APR is lower than the weighted average APR of the debts you're consolidating. Many people consolidate without doing this calculation and end up paying more — especially when origination fees are factored in.

Here's a concrete example. Say you have $15,000 in credit card debt across three cards at an average APR of 22%. You're paying $3,300 per year in interest. If you consolidate into a personal loan at 12% APR, you pay $1,800 per year — saving $1,500 annually. Over a 3-year payoff, that's $4,500 in savings. Clear win.

Now the same scenario with a 6% origination fee on the consolidation loan: the fee costs $900 upfront, reducing your net savings to $3,600. Still worth it. But if your consolidation loan rate is 19% instead of 12%, you'd save only $450 per year — and the origination fee might wipe out 1–2 years of savings. Use our free Debt Consolidation Calculator to run your specific numbers before applying.

Real Scenarios: When Consolidation Makes Sense (and When It Doesn't)

$18,000 across 4 credit cards averaging 24% APR. Credit score: 680. Qualifies for a LightStream consolidation loan at 11% APR over 48 months. Monthly payment: $466. Total interest paid: ~$4,368. Without consolidation, paying the same $466/month across the cards would cost approximately $8,200 in interest. Net savings: ~$3,800. Clear win.

$8,000 in credit card debt at 19% APR. Credit score: 590. Best available consolidation loan: 28% APR with a 10% origination fee ($800). The origination fee plus higher rate means consolidation costs more than the original debt. In this case, a 0% balance transfer card or an aggressive payoff plan is better than consolidating.

The Biggest Mistake People Make with Debt Consolidation

The most common — and costly — mistake is consolidating credit card debt and then running the cards back up. You end up with both the consolidation loan payment and new credit card debt, leaving you worse off than before. Studies suggest this happens to a significant percentage of people who consolidate without a behavioral plan.

The solution is behavioral, not financial: after consolidating, either close the cards (accepting the temporary credit score impact) or freeze them — literally put them in a container of water in your freezer. The friction of thawing them out is enough to prevent impulse spending. If you can't commit to not using the cards, consolidation will likely make your situation worse, not better.

Debt Consolidation vs. Balance Transfer: Which Is Better?

For credit card debt specifically, a 0% intro APR balance transfer card is often a better option than a consolidation loan — if you qualify. The best balance transfer cards offer 0% APR for 15–21 months with a 3%–5% transfer fee. On $10,000 in debt, a 3% transfer fee costs $300 upfront, but you pay zero interest for 18 months. That's almost always cheaper than a consolidation loan at 12%–15% APR.

The catch: you need good credit (670+) to qualify for the best balance transfer cards, and you must pay off the balance before the intro period ends — otherwise the rate jumps to 25%+. If you have the discipline to pay it off and the credit score to qualify, a balance transfer is usually the cheaper option. See our balance transfer card guide for top picks.

Calculate Your Consolidation Savings

Enter your current debts and see exactly how much you'd save with a consolidation loan — before you apply.

Use the Free Calculator →Frequently Asked Questions

Does debt consolidation hurt your credit score?

Applying for a consolidation loan causes a temporary 2–5 point dip from the hard inquiry. However, paying off credit cards reduces your utilization ratio, which can improve your score by 20–50 points within a few months.

What is the best debt consolidation loan for fair credit?

Upstart is the top pick for fair credit (580–669) due to its AI-powered approval model. Achieve is also a strong option with its direct creditor payoff feature.

How much can I save with debt consolidation?

It depends on your current rates and the consolidation loan rate. On $15,000 in credit card debt at 22% APR, consolidating at 12% APR over 3 years saves approximately $4,200 in interest. Use our Debt Consolidation Calculator for your exact numbers.

Can I consolidate student loans with a personal loan?

Technically yes, but it is generally not recommended. Federal student loans have income-driven repayment options and forgiveness programs that you lose if you refinance into a private personal loan. Only consider this if your private student loan rates are higher than available personal loan rates.