Getting approved for a personal loan is not just about having a good credit score — lenders evaluate multiple factors simultaneously. Understanding what lenders look for and how to present your application in the best light can make the difference between approval and rejection, and between a 10% APR and a 25% APR.

Before accepting any loan offer, calculate the total cost of the loan (principal + all interest + fees). A lower monthly payment often means paying thousands more over the life of the loan.

What Lenders Look At

Credit Score

Your FICO score is the first filter most lenders apply. Each lender has a minimum score requirement — typically 580–640 for online lenders, 660+ for banks and credit unions. Your score also determines your rate tier: the higher your score, the lower your APR. Check your score for free at AnnualCreditReport.com or through your bank before applying.

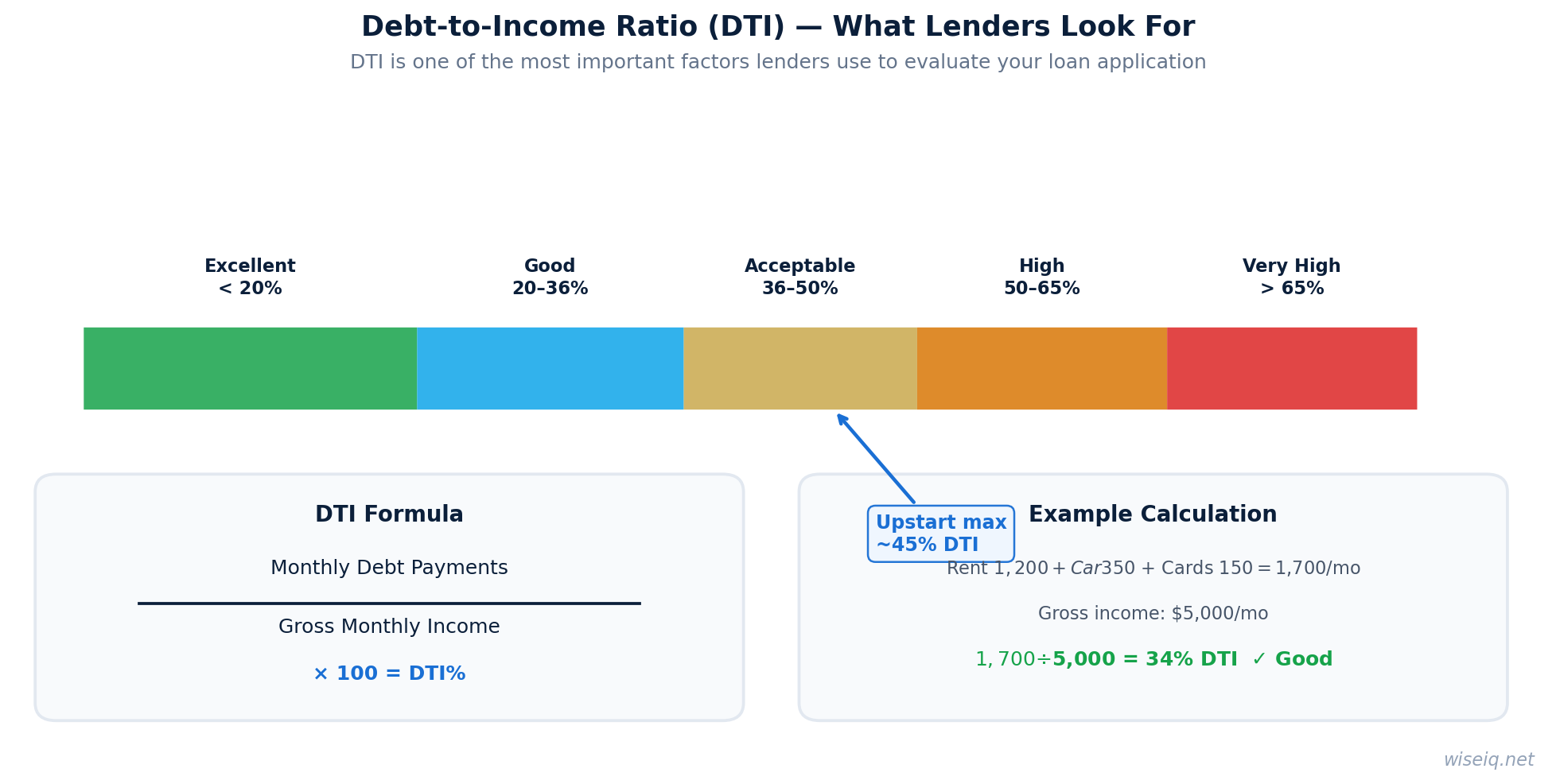

Debt-to-Income Ratio (DTI)

Your DTI is your total monthly debt payments divided by your gross monthly income. Most lenders want a DTI below 43%, with the best rates going to borrowers below 36%. To calculate yours: add up all monthly debt payments (credit cards, car loans, student loans, rent) and divide by your gross monthly income. If your DTI is above 43%, paying down debt before applying will significantly improve your odds.

Income and Employment

Lenders want to see stable, verifiable income. Most require at least 6 months at your current job (or 2 years of self-employment history). You will typically need to provide recent pay stubs, W-2s, or tax returns. Some lenders like Upstart also consider your field of study and career trajectory as indicators of future earning potential.

Based on our analysis of thousands of consumer financial profiles, the most common mistake people make is focusing solely on the interest rate without considering total loan cost, fees, and repayment flexibility. Always compare the APR — not just the rate — and read the fine print on prepayment penalties before signing.

Step-by-Step: How to Get Approved

Step 1: Check Your Credit Report

Before applying, pull your free credit report from all three bureaus at AnnualCreditReport.com. Look for errors — incorrect late payments, accounts that are not yours, or outdated negative items. Disputing and correcting errors can improve your score by 20–50 points within 30–60 days.

Step 2: Pre-Qualify with Multiple Lenders

Pre-qualification uses a soft credit pull and shows you estimated rates without affecting your score. Pre-qualify with 3–5 lenders to compare offers. Our Personal Loans comparison page shows the top lenders side by side.

Step 3: Gather Your Documents

Have these ready before you formally apply: government-issued ID, Social Security number, recent pay stubs (last 2–3), bank statements (last 2–3 months), and your employer's contact information. Having everything ready speeds up the process significantly.

Step 4: Choose the Right Loan Amount and Term

Borrowing more than you need increases your DTI and your total interest cost. Choose the minimum amount that meets your need. For term length: shorter terms have higher monthly payments but lower total interest; longer terms have lower payments but cost more overall. Use our Personal Loan Calculator to find the right balance.

Step 5: Apply and Accept Promptly

Once you choose a lender, complete the formal application. Most online lenders give a decision within minutes. If approved, review the loan agreement carefully — check the APR, origination fee, monthly payment, and prepayment terms. Accept promptly, as rate locks typically expire within 14–30 days.

A personal loan is not the right tool for every situation. Consider alternatives if any of the following apply to you:

- You have home equity: A HELOC typically offers rates 5–10% lower than personal loans. If you own your home, compare HELOC rates before taking a personal loan.

- Your debt is primarily credit card debt: A balance transfer card with a 0% intro APR (typically 12–21 months) will cost less than a personal loan if you can pay off the balance within the intro period.

- You need less than $1,000: Most personal loan lenders have minimum amounts of $1,000–$2,000. For smaller needs, a credit union payday alternative loan (PAL) or a 0% APR credit card may be more appropriate.

- Your credit score is below 500: Most personal loan lenders — including those that accept "bad credit" — have practical minimums around 500–560. Below this, secured loans, credit-builder loans, or co-signer arrangements are more realistic options.

- You are in active bankruptcy: Personal loan lenders will decline applicants in active Chapter 7 or Chapter 13 proceedings. Resolve your bankruptcy first.

Answer 3 quick questions and get a personalized recommendation in seconds.

Common Reasons for Rejection

If you are rejected, the lender is required to send you an adverse action notice explaining why. Common reasons include: credit score below the lender's minimum, DTI too high, insufficient income, too many recent hard inquiries, or a very short credit history. Each reason has a specific fix — use the notice to guide your next steps.

Upstart considers more than your credit score — education, employment, and income all factor in. Best option for borrowers who have been rejected elsewhere. Typical APR 6.2%–35.99%, subject to change.

SoFi offers the best rates for borrowers with strong credit and income. No fees of any kind. Unemployment protection included.

Find Your Best Rate in 2 Minutes

Answer 5 quick questions and see personalized loan offers matched to your credit profile — no credit pull required.

Check My Options →Frequently Asked Questions

What credit score do I need for a personal loan?

Most lenders require a minimum of 580–640. Upstart accepts scores as low as 300. The higher your score, the lower your rate — borrowers with 750+ typically qualify for rates below 10% APR.

How long does personal loan approval take?

Online lenders typically provide a decision within minutes of submitting your application. Funding takes 1–3 business days after you accept the loan agreement.

Does pre-qualifying hurt my credit score?

No. Pre-qualification uses a soft credit pull that does not affect your score. Only a formal application triggers a hard inquiry, which may reduce your score by 2–5 points temporarily.

What documents do I need for a personal loan?

Typically: government-issued ID, Social Security number, recent pay stubs or tax returns, bank statements, and your employer's contact information. Having these ready before you apply speeds up the process.