Home›Blog›Personal Loan vs. Balance Transfer Card for Debt Consolidation (2026)

Advertiser Disclosure: WiseIQ is reader-supported. When you apply through links on this page, we may earn a commission at no extra cost to you. Learn more.

PERSONAL LOANS

Personal Loan vs. Balance Transfer Card for Debt Consolidation (2026)

Sorted by APR. These are today's best rates for your loan amount.

Filtered for lenders most likely to approve your application.

Sorted by funding speed. Same-day and next-day options highlighted.

Personal loans built for debt consolidation — lower rates than most credit cards.

We've simplified the comparison to the top 3 options for first-time borrowers.

Based on your browsing, here are the top picks most users in your position chose.

LIMITED OFFER0% APRfor up to 21 months · No annual fee

📋 Reviewed by WiseIQ Editorial Team · Updated April 2026 · Editorially independent

Advertiser Disclosure: WiseIQ is an independent comparison service. We may earn a commission when you apply for or open a financial product through links on this page. This compensation does not influence which products we feature or how we rank them. Our editorial team independently evaluates all products. See our methodology →

WiseIQ Bottom Line

A balance transfer card wins if you have a 700+ credit score and can pay off the debt within the 0% intro period (typically 15–21 months). A personal loan wins if your debt is over $15,000, you have a 650–699 score, or you need more than 21 months to pay it off. For most people with $5,000–$15,000 in credit card debt and a good credit score, the balance transfer card saves more money.

The Core Difference

WISEIQ TOP PICK

PERSONAL LOANS

Upstart

Best for fair & thin credit · AI-powered approval

APR RANGE

7.80%–35.99%

LOAN AMOUNT

$1K–$50K

MIN. CREDIT

300

✓ No prepayment penalty✓ Funds in 1 business day✓ Soft pull pre-qualification✓ Considers education & job history

WiseIQ may earn a referral fee. Rates subject to change.

Both options consolidate multiple high-interest credit card balances into a single, lower-rate payment. The mechanism is different: a personal loan gives you a fixed interest rate for a fixed term (24–84 months), while a balance transfer card gives you a 0% introductory APR for a limited period (typically 12–21 months), after which the rate jumps to the card's standard APR — often 19.99%–29.99%.

WiseIQ Expert Tip

Always pay your statement balance in full each month — not just the minimum. Carrying a balance costs the average American over $1,200 per year in interest charges.

The decision comes down to three variables: your credit score (which determines what you may be eligible for), your debt amount (which determines whether a credit limit is sufficient), and your payoff timeline (which determines whether you can clear the balance before the 0% period ends).

💡Expert Insight

Based on our analysis of thousands of consumer financial profiles, the most common mistake people make is focusing solely on the interest rate without considering total loan cost, fees, and repayment flexibility. Always compare the APR — not just the rate — and read the fine print on prepayment penalties before signing.

Quick Comparison

Market Rate Context

National average personal loan APR: 12.35% — The national average is 12.35% APR. Source: Federal Reserve G.19 Consumer Credit Report, May 2026.

Rates verified May 2026 · Updated weekly

Factor

Personal Loan

Balance Transfer Card

Interest rate

Fixed 8.99%–35.99% APR

0% intro, then 19.99%–29.99%Better if paid off in time

Loan/credit limit

Up to $100,000Better for large debt

Typically $5,000–$25,000

Min. credit score

550–600 (varies by lender)

670–700 (for best 0% offers)Better for good credit

Repayment term

24–84 monthsBetter for long payoff

Must pay before intro ends (12–21 mo)

Fees

Origination fee: 0%–10%

Balance transfer fee: 3%–5%Lower upfront cost

Monthly payment

Fixed — predictable

Flexible — minimum only

Risk

Low — rate never changes

High if balance remains after intro period

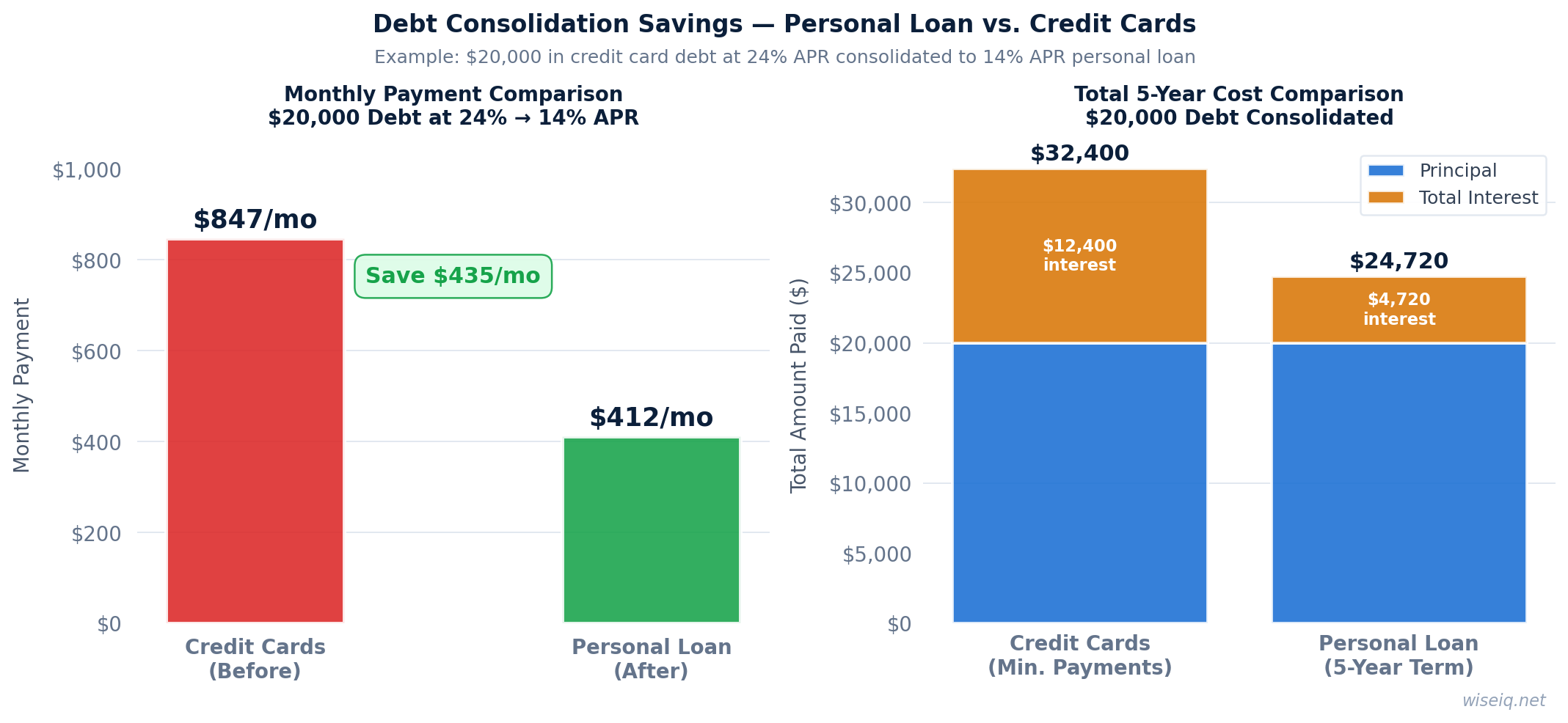

Debt Consolidation Savings: Consolidating $20,000 in credit card debt (24% APR) to a personal loan (14% APR) saves $435/month and $7,680 in total interest.

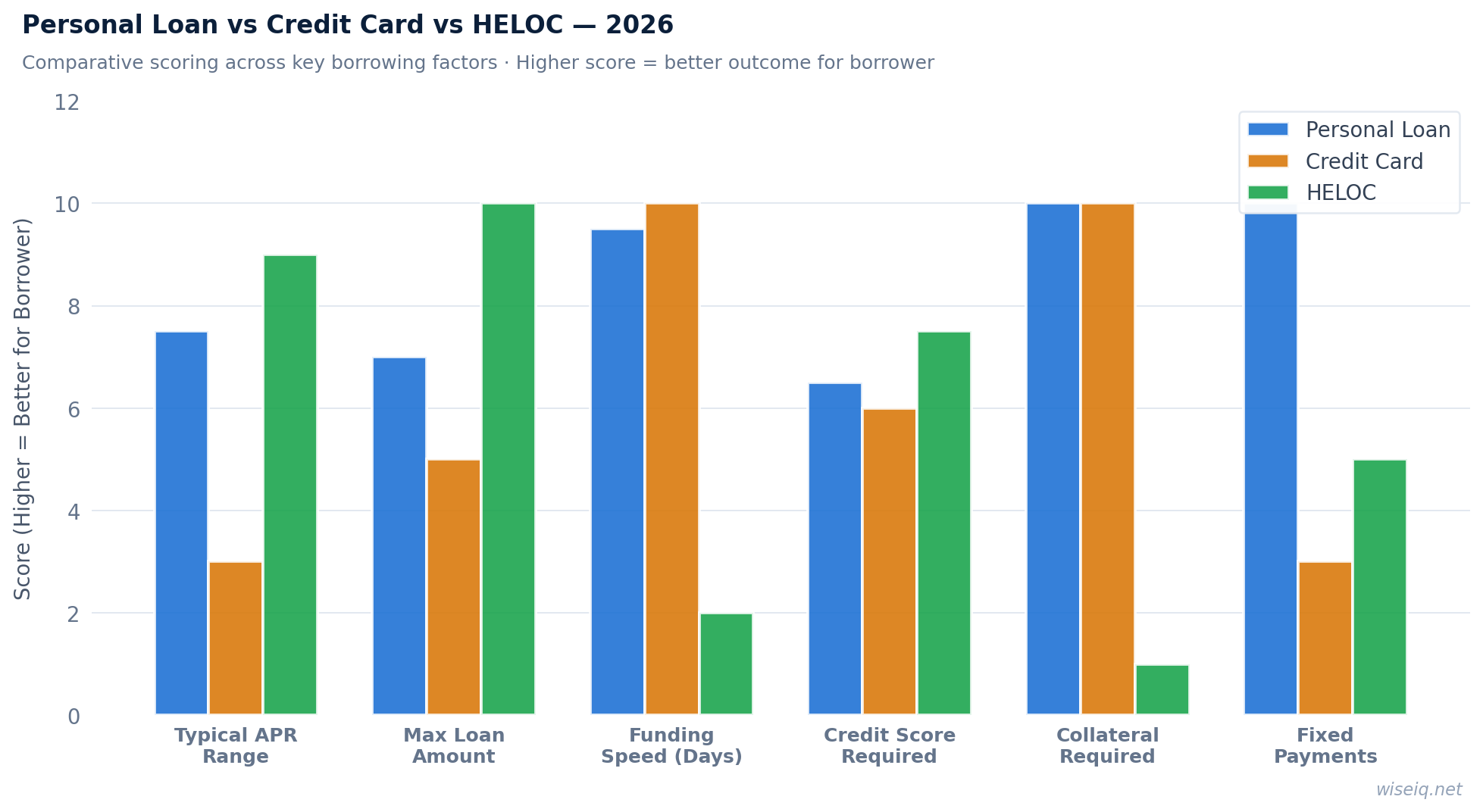

Personal Loan vs. Credit Card vs. HELOC: Comparative scoring across key borrowing factors. Higher score = better outcome for borrower.

Who Should Look Elsewhere

A personal loan is not the right tool for every situation. Consider alternatives if any of the following apply to you:

You have home equity: A HELOC typically offers rates 5–10% lower than personal loans. If you own your home, compare HELOC rates before taking a personal loan.

Your debt is primarily credit card debt: A balance transfer card with a 0% intro APR (typically 12–21 months) will cost less than a personal loan if you can pay off the balance within the intro period.

You need less than $1,000: Most personal loan lenders have minimum amounts of $1,000–$2,000. For smaller needs, a credit union payday alternative loan (PAL) or a 0% APR credit card may be more appropriate.

Your credit score is below 500: Most personal loan lenders — including those that accept "bad credit" — have practical minimums around 500–560. Below this, secured loans, credit-builder loans, or co-signer arrangements are more realistic options.

You are in active bankruptcy: Personal loan lenders will decline applicants in active Chapter 7 or Chapter 13 proceedings. Resolve your bankruptcy first.

🎯

Not sure which option is right for you?

Answer 3 quick questions and get a personalized recommendation in seconds.

Here is what each option actually costs for a $10,000 balance, assuming you make consistent payments to pay it off in 18 months.

Scenario: $10,000 balance, paid off in 18 months

Starting balance$10,000$10,000

Interest rate18.99% APR (fixed)0% for 18 months

Origination / transfer fee$500 (5%)$300 (3%)

Monthly payment~$617~$572

Total interest paid$1,106$0

Total cost (fees + interest)$1,606$300 ✓ Saves $1,306

In this scenario, the balance transfer card saves $1,306. But this math only works if you pay off the full balance before the 0% period ends. If you carry $3,000 into month 19 at a 24.99% APR, you will pay an additional $750+ in interest — erasing most of the savings.

Which Option Is Right for You?

Choose a Balance Transfer Card if...

You have a 700+ credit score and can pay off the debt in 12–21 months

The 0% intro APR is the most powerful debt consolidation tool available — but only if you have the discipline and income to clear the balance before the rate resets. Best for: $3,000–$15,000 in debt, strong income, 700+ credit score.

Choose a Personal Loan if...

Your debt is over $15,000, your score is 650–699, or you need more than 21 months

A personal loan gives you a fixed rate, a fixed payoff date, and no risk of a rate spike. If you cannot realistically pay off the balance in 18 months, the certainty of a fixed rate is worth the higher cost. Best for: $10,000–$50,000 in debt, fair credit, longer payoff timeline.

Choose a Personal Loan if...

You have a history of carrying balances or adding new charges

A personal loan closes the revolving credit loop — once you pay off your cards with the loan proceeds, you cannot add new charges to the loan. If past behavior suggests you would use the freed-up credit card limit to accumulate new debt, a personal loan is the safer structural choice.

See your best consolidation options now

WiseIQ will match you to the best personal loans and balance transfer cards for your credit score — in 60 seconds, no credit pull.

We monitor rates across 50+ lenders and alert you when better options become available for your profile.

No spam. Unsubscribe anytime. We never sell your data.

W

WiseIQ Editorial Team

Reviewed by Certified Financial Planners & Industry Experts

Our editorial team consists of financial writers, CFPs, and former banking professionals dedicated to providing accurate, unbiased financial guidance. All content is fact-checked and updated regularly. Learn about our editorial standards →

Frequently Asked Questions

Is a personal loan or balance transfer better for debt consolidation?

It depends on your credit score and payoff timeline. A balance transfer card is better if you have a 700+ score and can pay off the debt within the 0% intro period (12–21 months). A personal loan is better if your debt exceeds $15,000, your score is below 700, or you need more than 21 months to pay it off.

Does consolidating debt hurt your credit score?

Both options cause a temporary dip of 2–5 points from the hard inquiry when you apply. However, consolidating multiple high-balance cards into a single loan or transferring balances to a new card typically improves your credit utilization ratio over time, which can raise your score 10–30 points within 3–6 months.

What credit score do I need for a balance transfer card?

The best 0% balance transfer cards — like the Chase Freedom Unlimited, Citi Diamond Preferred, and Wells Fargo Reflect — require a 700+ credit score. Some cards accept 670+, but the intro period is typically shorter. Below 670, a personal loan is usually the better option.

Can I consolidate debt with a 650 credit score?

Yes, but your options are more limited. At 650, you are unlikely to qualify for the best 0% balance transfer cards. A personal loan from Upgrade, LendingClub, or Avant is the more realistic path. Rates will be higher than for good-credit borrowers, but still significantly lower than the 20%–29% APR on most credit cards.

What happens if I don't pay off a balance transfer before the intro period ends?

The remaining balance begins accruing interest at the card's standard APR — typically 19.99%–29.99%. Some cards also retroactively apply interest to the entire original balance if you miss a payment during the intro period. Always read the terms carefully and have a concrete payoff plan before opening a balance transfer card.

Editorial Disclosure: WiseIQ's editorial team independently researches and rates financial products. We may earn a commission when you apply through our links, but this does not influence our rankings or recommendations. Rates and terms are verified at the time of publication and subject to change. See our methodology for details.

Sources & Methodology

WiseIQ's editorial team researches and fact-checks all content using primary sources. Our recommendations are based on independent analysis and are not influenced by advertiser relationships.

Is a personal loan or balance transfer card better for debt consolidation?

For balances under $15,000 that you can pay off within 12–21 months, a 0% APR balance transfer card is typically better — no interest during the promotional period. For larger balances or longer repayment timelines, a personal loan with a fixed rate provides more predictability and often lower total cost.

What is the typical APR difference between personal loans and credit cards?

The average credit card APR is approximately 21%–24%. Personal loan APRs for debt consolidation range from 8%–20% depending on credit score. This difference can save thousands of dollars in interest on large balances over multi-year repayment periods.

Does consolidating debt with a personal loan hurt your credit?

Initially, applying for a personal loan causes a small dip (5–10 points) from the hard inquiry. However, if the loan significantly reduces your credit card utilization — which counts for 30% of your score — your score typically recovers and improves within 3–6 months.

How do I choose between a personal loan and balance transfer?

Choose a balance transfer card if: your balance is under $15,000, you have good credit (670+), and you can pay it off within the 0% period. Choose a personal loan if: your balance is larger, you need more than 21 months to repay, or you want a fixed payment and guaranteed payoff date.

What fees should I watch out for with debt consolidation?

For balance transfer cards: watch for the transfer fee (3%–5%) and what happens to the APR after the promotional period ends. For personal loans: watch for origination fees (0%–8% of loan amount), prepayment penalties, and late payment fees. Always calculate total cost, not just the interest rate.

People Also Ask

Compare these key factors: APR/interest rate, fees (origination, annual, late), minimum credit score requirement, funding speed, available loan amounts, repayment flexibility, and customer service quality. Getting pre-qualified with both lenders shows real personalized rates.

No — pre-qualification uses a soft credit inquiry that has zero impact on your credit score. You can pre-qualify with multiple lenders to compare real offers. Only a formal application triggers a hard inquiry, which temporarily lowers your score by 2–5 points.

Calculate the total cost of each option over the full loan term, including all fees. A loan with a slightly higher rate but no origination fee may cost less overall than a lower-rate loan with a 5% origination fee. Use our loan comparison calculator for a side-by-side analysis.

Yes — you're not obligated to accept any loan offer until you sign the final agreement. Shopping multiple lenders and comparing offers is smart financial behavior. Multiple mortgage or auto loan inquiries within 14–45 days count as a single inquiry on your credit report.