When you need to borrow money, three options dominate: personal loans, credit cards, and HELOCs. Each has distinct advantages, risks, and ideal use cases. The right choice depends on how much you need, how quickly you need it, and whether you own a home.

Fixed-rate, lump-sum loan repaid over 2–7 years. No collateral required. Best for defined expenses with a clear payoff plan.

Revolving credit line with variable rate. Best for everyday spending, rewards, and short-term financing (especially 0% APR offers).

Variable-rate line of credit secured by your home equity. Best for large, ongoing expenses like home renovation where you need flexibility.

Side-by-Side Comparison

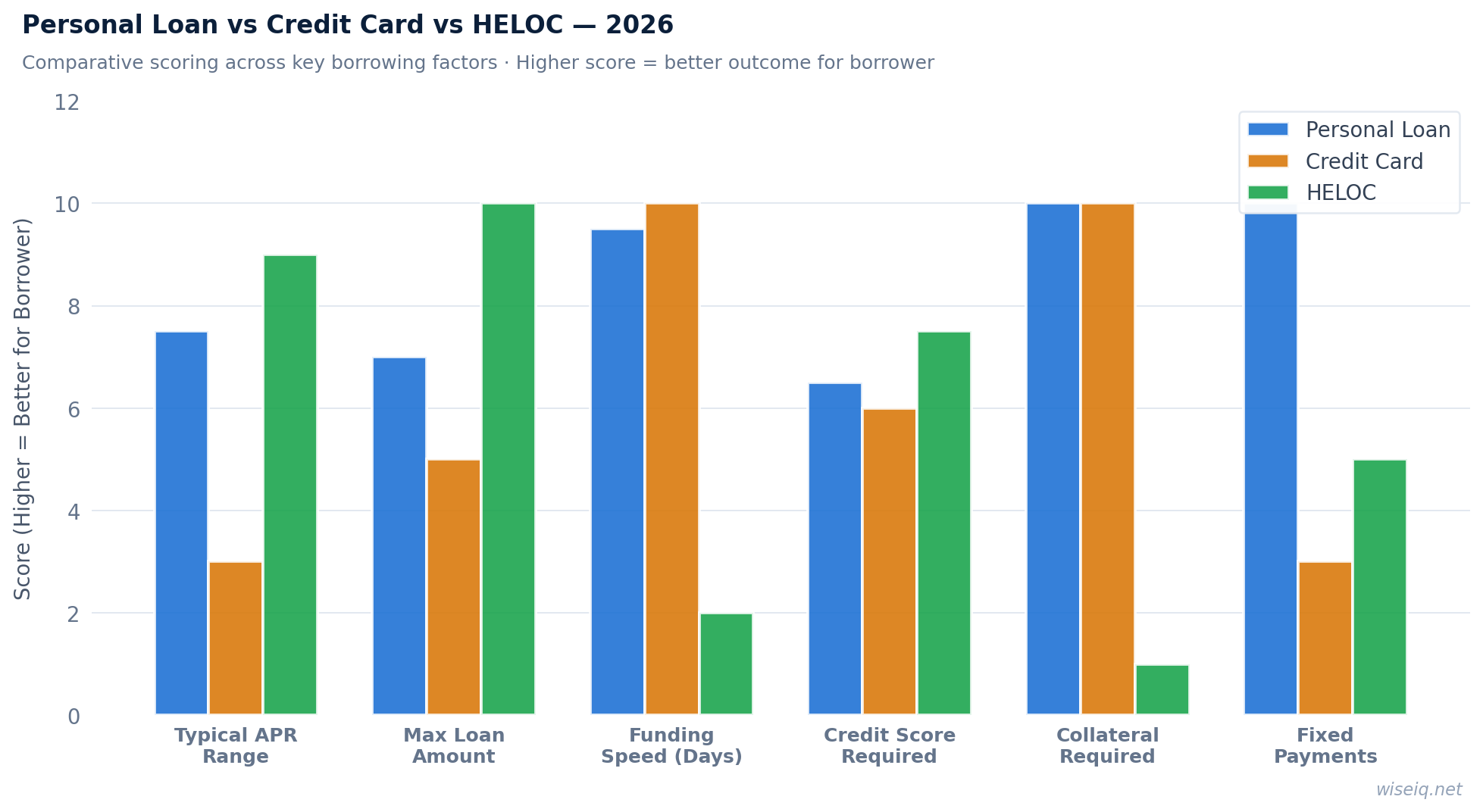

| Feature | Personal Loan | Credit Card | HELOC |

|---|---|---|---|

| Interest rate | Fixed 6%–36% | Variable 20%+ | Variable 7%–12% |

| Collateral required | None | None | Your home |

| Foreclosure risk | No | No | Yes |

| Funding speed | 1–3 days | Instant (existing card) | 2–6 weeks |

| Best amount | $1,000–$100,000 | $500–$30,000 | $10,000–$500,000 |

| Rate type | Fixed | Variable | Variable |

| Credit score needed | 580+ | 580+ | 620+ |

| Tax deductible | No | No | Sometimes (home improvement) |

The Verdict: Which Should You Choose?

- You need a fixed monthly payment

- You don't own a home

- You want funds in 1–3 days

- You're consolidating debt

- You can pay off in 12–21 months

- You qualify for a 0% APR offer

- You want rewards on spending

- Amount is under $10,000

- You own a home with equity

- You need $50,000+

- You can wait 2–6 weeks

- You're comfortable with variable rate

A personal loan is not the right tool for every situation. Consider alternatives if any of the following apply to you:

- You have home equity: A HELOC typically offers rates 5–10% lower than personal loans. If you own your home, compare HELOC rates before taking a personal loan.

- Your debt is primarily credit card debt: A balance transfer card with a 0% intro APR (typically 12–21 months) will cost less than a personal loan if you can pay off the balance within the intro period.

- You need less than $1,000: Most personal loan lenders have minimum amounts of $1,000–$2,000. For smaller needs, a credit union payday alternative loan (PAL) or a 0% APR credit card may be more appropriate.

- Your credit score is below 500: Most personal loan lenders — including those that accept "bad credit" — have practical minimums around 500–560. Below this, secured loans, credit-builder loans, or co-signer arrangements are more realistic options.

- You are in active bankruptcy: Personal loan lenders will decline applicants in active Chapter 7 or Chapter 13 proceedings. Resolve your bankruptcy first.

Answer 3 quick questions and get a personalized recommendation in seconds.

Frequently Asked Questions

Advertiser Disclosure: WiseIQ may earn a referral fee from some lenders and financial products on this page. This does not influence our editorial ratings or recommendations. Our reviews are independently researched and editorially independent.

Sources & Methodology: WiseIQ's editorial team researches and fact-checks all content using primary sources including the Consumer Financial Protection Bureau (CFPB), Federal Reserve G.19 Consumer Credit Report, myFICO Credit Education, and lender websites for current rates and terms. Last reviewed: April 2026. How we rank products.