Having a 600 credit score places you in the "fair" credit category, which means traditional lenders might view you as a higher risk. However, this doesn't mean personal loans are out of reach. Many lenders specialize in working with borrowers who have less-than-perfect credit, offering viable solutions for consolidating debt, covering unexpected expenses, or funding significant purchases. The key is knowing where to look and understanding what to expect in terms of interest rates and loan terms. This comprehensive guide will help you navigate the landscape of personal loans with a 600 credit score, providing actionable steps to improve your chances of approval and secure the best possible terms in 2026.

Before accepting any loan offer, calculate the total cost of the loan (principal + all interest + fees). A lower monthly payment often means paying thousands more over the life of the loan.

Understanding Your Options: Lenders for a 600 Credit Score

At this score range, you'll qualify for some products but with higher rates and stricter terms. Subprime lenders are your primary option.

Expect rates 5–12% above prime borrowers.

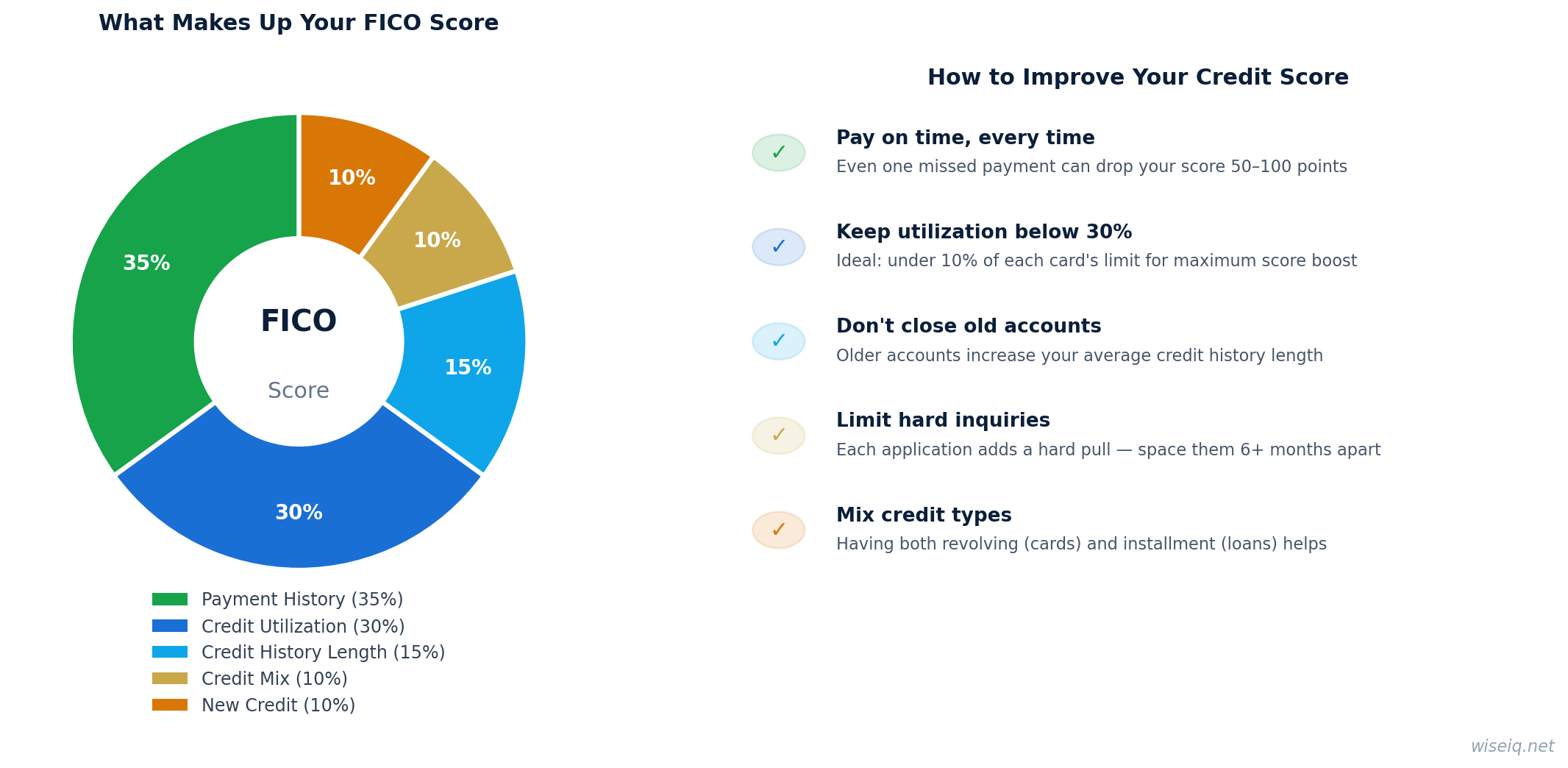

Dispute any errors on your credit report — even one removed negative item can push you into the fair range.

Timeline: 6–18 months of positive activity can improve your score significantly.

While a 600 credit score might limit your access to prime rates, several reputable lenders are willing to consider applicants in this range. These lenders often look beyond just your credit score, evaluating factors like your income, employment history, and debt-to-income ratio. It's crucial to compare offers from various lenders to find one that best suits your financial situation.

Avant is a popular choice for borrowers with fair credit, offering a straightforward application process and quick funding. They consider a range of factors beyond just your credit score.

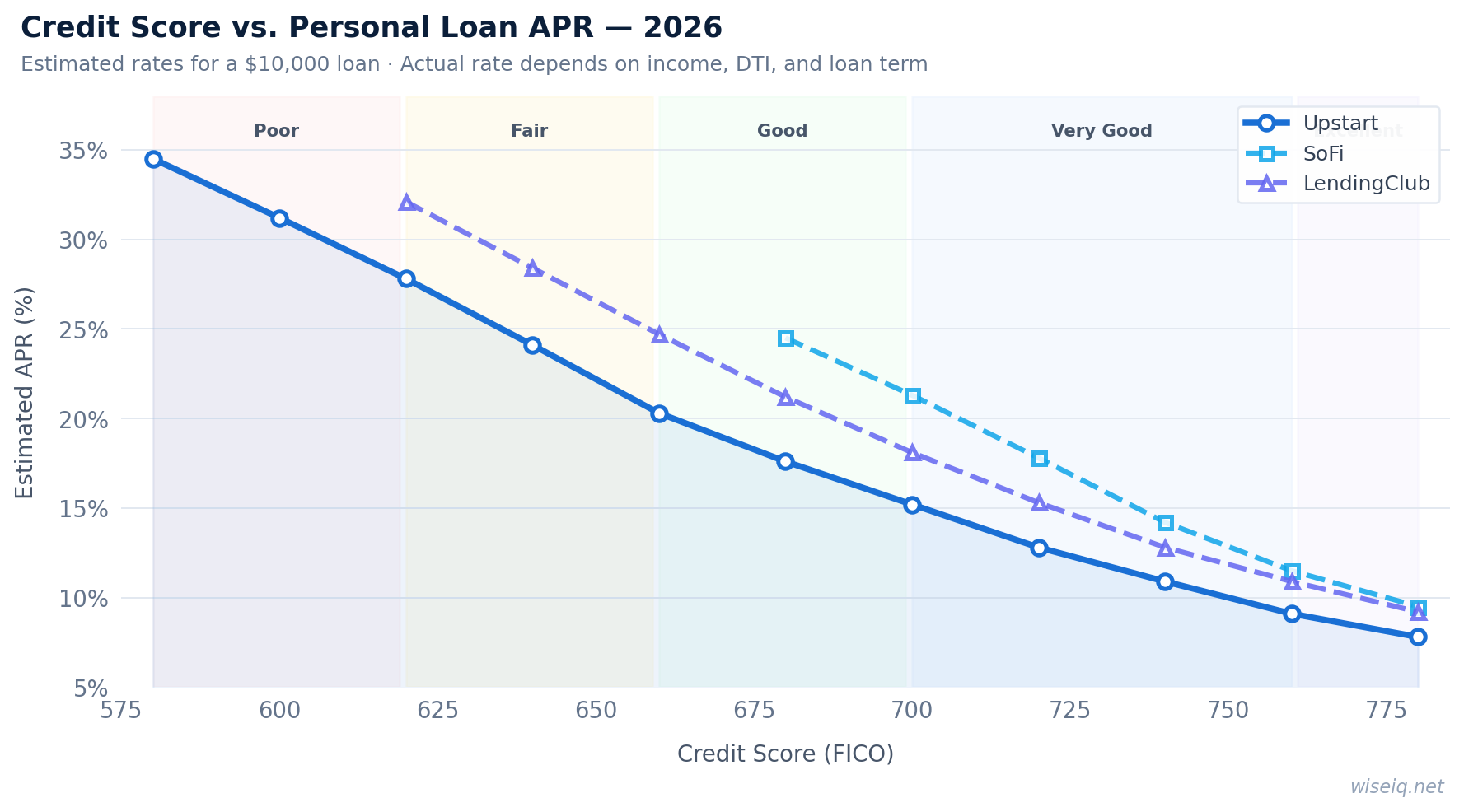

LendingClub offers personal loans through a peer-to-peer model, which can sometimes provide more flexible terms for borrowers with a 600 credit score. They are a solid option for debt consolidation.

Best Egg offers personal loans with competitive rates for borrowers with fair to good credit. They are known for their quick application process and funding, making them a good option for urgent needs.

OneMain Financial offers both unsecured and secured personal loans, which can be a significant advantage for borrowers with a 600 credit score. Their local branches provide a personalized touch.

Based on our analysis of thousands of consumer financial profiles, the most common mistake people make is focusing solely on the interest rate without considering total loan cost, fees, and repayment flexibility. Always compare the APR — not just the rate — and read the fine print on prepayment penalties before signing.

What to Expect: APRs and Loan Terms with a 600 Credit Score

When you have a 600 credit score, it's important to set realistic expectations regarding the Annual Percentage Rate (APR) and loan terms. Lenders typically view borrowers with fair credit as having a higher risk of default, which translates to higher interest rates. You can generally expect APRs to range from 18% to 36%. The exact rate will depend on several factors, including the lender, the loan amount, the loan term, and your overall financial health. Longer loan terms might offer lower monthly payments but will result in paying more interest over the life of the loan. Always review the loan offer carefully, paying close attention to the APR, fees, and total cost of the loan.

A personal loan is not the right tool for every situation. Consider alternatives if any of the following apply to you:

- You have home equity: A HELOC typically offers rates 5–10% lower than personal loans. If you own your home, compare HELOC rates before taking a personal loan.

- Your debt is primarily credit card debt: A balance transfer card with a 0% intro APR (typically 12–21 months) will cost less than a personal loan if you can pay off the balance within the intro period.

- You need less than $1,000: Most personal loan lenders have minimum amounts of $1,000–$2,000. For smaller needs, a credit union payday alternative loan (PAL) or a 0% APR credit card may be more appropriate.

- Your credit score is below 500: Most personal loan lenders — including those that accept "bad credit" — have practical minimums around 500–560. Below this, secured loans, credit-builder loans, or co-signer arrangements are more realistic options.

- You are in active bankruptcy: Personal loan lenders will decline applicants in active Chapter 7 or Chapter 13 proceedings. Resolve your bankruptcy first.

Answer 3 quick questions and get a personalized recommendation in seconds.

How to Improve Your Approval Odds

Even with a 600 credit score, there are strategies you can employ to increase your chances of getting approved for a personal loan and potentially secure better terms:

- Apply with a Co-signer: A co-signer with good credit can significantly boost your application. Their creditworthiness provides an added layer of security for the lender, potentially leading to approval and a lower interest rate.

- Consider a Secured Loan: Secured personal loans require collateral, such as a car or savings account. This reduces the lender's risk, making them more willing to approve your application, even with a fair credit score.

- Demonstrate Stable Income: Lenders want to see that you have a consistent and sufficient income to repay the loan. Provide clear documentation of your employment and income.

- Reduce Your Debt-to-Income Ratio: A high debt-to-income (DTI) ratio can be a red flag for lenders. Try to pay down existing debts before applying for a new loan to show you can manage your finances responsibly.

- Check for Pre-qualification: Many online lenders offer pre-qualification with a soft credit check, which won't impact your credit score. This allows you to see potential loan offers and compare rates without commitment.

- Explain Any Credit Issues: If you have specific reasons for your credit score (e.g., medical emergencies), some lenders may be willing to consider your explanation, especially if you can show you've taken steps to improve your financial situation.

Step-by-Step Guide to Getting a Personal Loan with a 600 Credit Score

Follow these steps to navigate the personal loan application process with a 600 credit score:

- Check Your Credit Report: Obtain a free copy of your credit report from AnnualCreditReport.com. Review it for any errors and dispute them immediately. Understanding your credit history is the first step.

- Determine Your Loan Needs: Clearly define why you need the loan and how much you need to borrow. This will help you choose the right lender and avoid borrowing more than necessary.

- Research Lenders: Focus on lenders that specialize in fair credit loans. Look at online lenders, credit unions, and community banks. Compare their minimum credit score requirements, APR ranges, and fees.

- Gather Necessary Documents: Prepare documents such as proof of income (pay stubs, tax returns), identification (driver's license), and bank statements. Having these ready will streamline the application process.

- Pre-qualify (If Available): Use pre-qualification tools to get an idea of the rates and terms you might receive without affecting your credit score.

- Submit Your Application: Once you've chosen a lender, complete the full application. Be honest and accurate with all information provided.

- Review Loan Offers: Carefully read all loan documents, paying attention to the APR, repayment schedule, and any associated fees. Don't hesitate to ask questions if anything is unclear.

- Accept the Loan and Receive Funds: If you're satisfied with the terms, accept the loan offer. Funds are typically disbursed within a few business days.