Advertiser Disclosure: WiseIQ earns a commission when you apply through links on this page. This does not influence our rankings. See how we rank →

WiseIQ Editorial Team

Reviewed by certified financial experts · Updated March 2026

Why we recommend it: Zero fees (no origination, no prepayment, no late fees). Competitive rates for debt consolidation. Unique on-time payment reward: make 12 consecutive on-time payments and you can skip one month. Best for borrowers with 660+ credit.

Before accepting any loan offer, calculate the total cost of the loan (principal + all interest + fees). A lower monthly payment often means paying thousands more over the life of the loan.

Affiliate disclosure: WiseIQ may earn a commission if you apply.

Why we recommend it: Specifically designed for credit card debt consolidation. Provides free FICO score monitoring and financial coaching. Research shows Happy Money customers see an average 40-point credit score increase after paying off their credit cards.

Affiliate disclosure: WiseIQ may earn a commission if you apply.

Why we recommend it: Best rates for 700+ credit scores. No fees, same-day funding, and a Rate Beat program — if you get a lower rate elsewhere, LightStream will beat it by 0.10%. Best for large debt consolidation ($25K+).

Affiliate disclosure: WiseIQ may earn a commission if you apply.

Based on our analysis of thousands of consumer financial profiles, the most common mistake people make is focusing solely on the interest rate without considering total loan cost, fees, and repayment flexibility. Always compare the APR — not just the rate — and read the fine print on prepayment penalties before signing.

A personal loan is not the right tool for every situation. Consider alternatives if any of the following apply to you:

Is a personal loan good for debt consolidation?

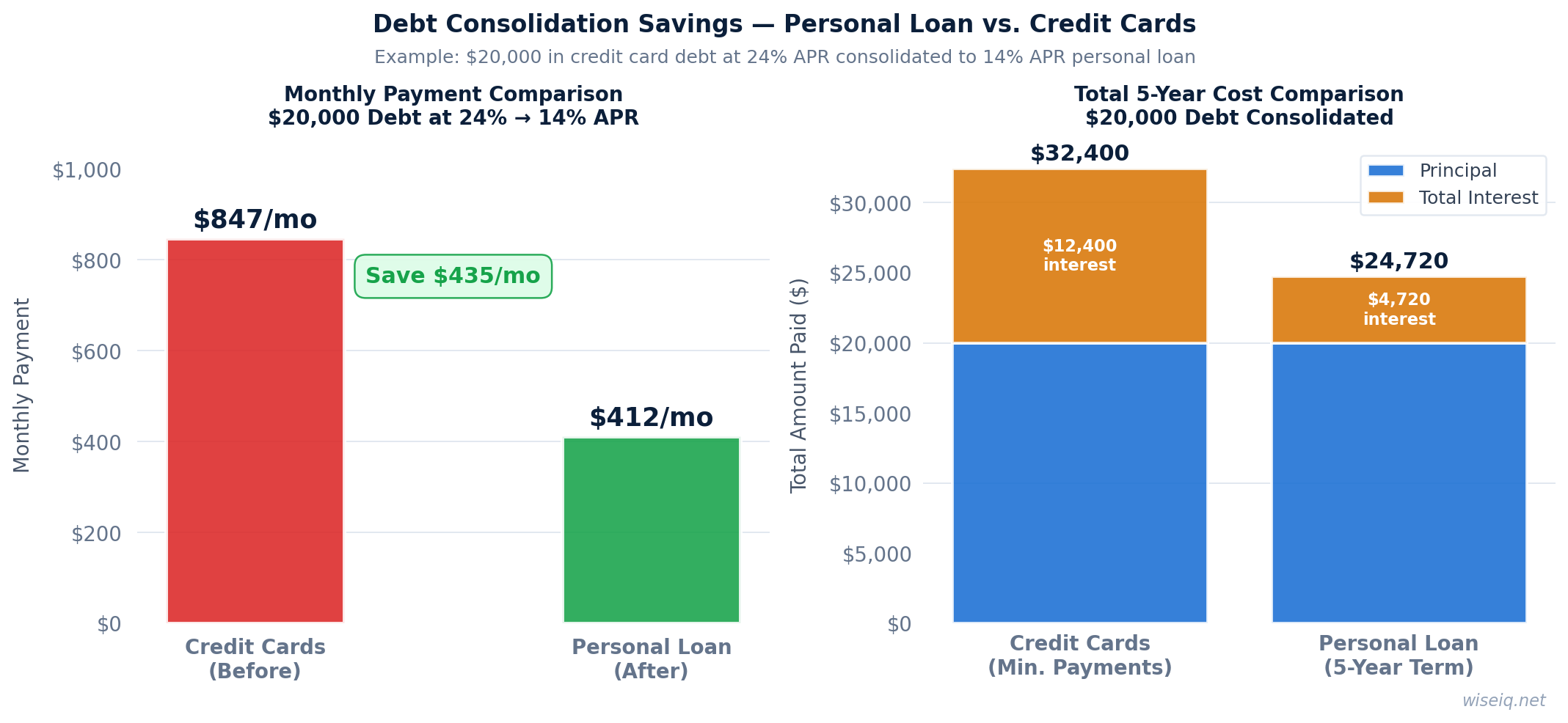

Yes, if you can get a lower interest rate than your current debts. If you have credit card debt at 20%–25% APR and qualify for a personal loan at 10%–15%, consolidation can save thousands in interest and simplify your payments to one monthly bill.

What credit score do I need for a debt consolidation loan?

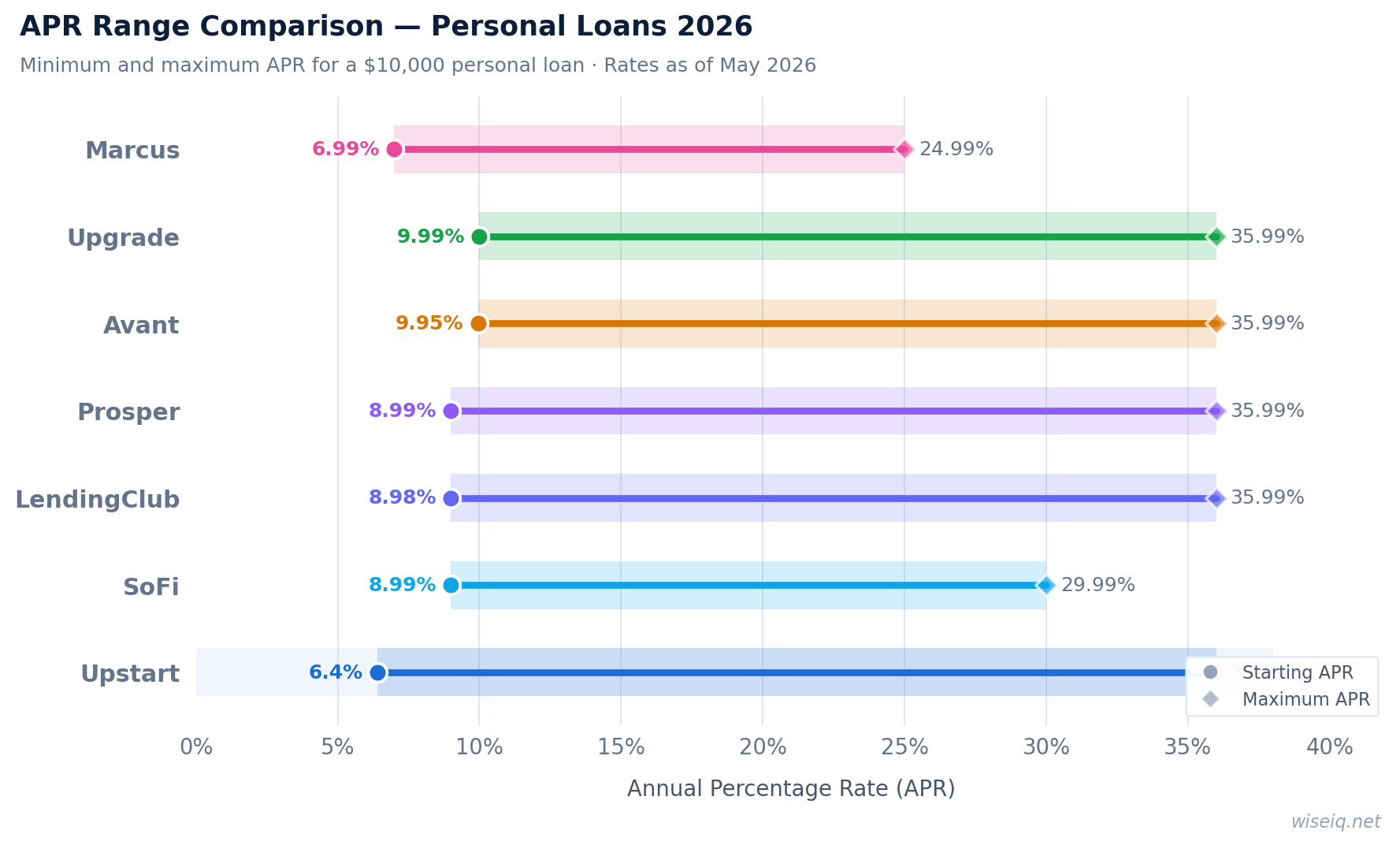

Most debt consolidation lenders require a 640–660 minimum credit score. Marcus and LightStream require 660+. Happy Money accepts 640+. Upstart accepts lower scores but rates will be higher. The better your credit, the lower your consolidation rate.

How much can I save by consolidating credit card debt?

The savings depend on your current rates and the consolidation rate you qualify for. Example: $20,000 in credit card debt at 22% APR costs $4,400/year in interest. Consolidating at 12% APR saves $2,000/year. Over a 3-year payoff, that's $6,000 in savings.

Does debt consolidation hurt your credit score?

Applying for a consolidation loan causes a hard inquiry (typically -5 to -10 points temporarily). However, paying off multiple credit cards reduces your credit utilization, which can increase your score significantly. Most borrowers see a net positive impact within 3–6 months.

Recommended books to go deeper on this topic

Dave Ramsey's famous baby steps system for getting out of debt and building wealth — practical and actionable.

View on Amazon →A comprehensive budgeting and debt management guide from one of the most trusted voices in personal finance.

View on Amazon →As an Amazon Associate, WiseIQ earns from qualifying purchases. This does not affect our editorial recommendations.

WiseIQ's editorial team researches and fact-checks all content using primary sources. Our recommendations are based on independent analysis and are not influenced by advertiser relationships.

Last reviewed: April 2026 | How we rank products

Dave Ramsey's famous baby steps system for getting out of debt and building wealth — practical and actionable.

View on Amazon →A comprehensive budgeting and debt management guide from one of the most trusted voices in personal finance.

View on Amazon →As an Amazon Associate, WiseIQ earns from qualifying purchases. This does not affect our editorial recommendations.