WiseIQ Editorial Team

Reviewed by certified financial experts · Updated March 2026

Your credit score affects the interest rate on every loan you take, whether you get approved for an apartment, and sometimes even whether you get a job offer. Raising it by even 50 points can save you thousands of dollars over the life of a mortgage or auto loan. Here is exactly how to do it — fast.

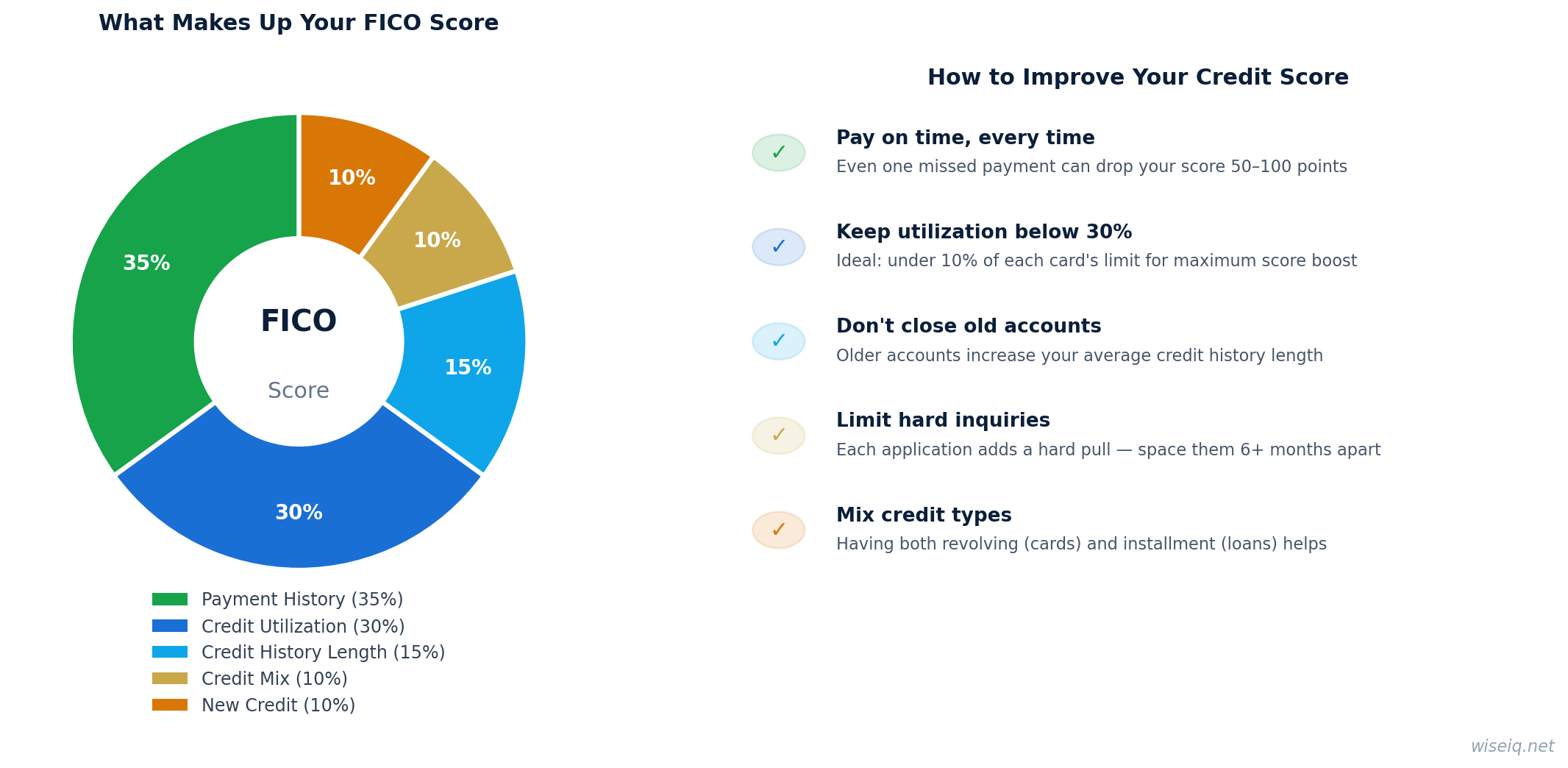

FICO scores — used by 90% of lenders — are calculated from five factors. Understanding the weight of each factor tells you where to focus your energy.

Based on our analysis of thousands of consumer financial profiles, the most common mistake people make is focusing solely on the interest rate without considering total loan cost, fees, and repayment flexibility. Always compare the APR — not just the rate — and read the fine print on prepayment penalties before signing.

Credit utilization — how much of your available credit you are using — accounts for 30% of your score. Paying down balances can raise your score within a single billing cycle. The target is under 30% utilization across all cards, and ideally under 10% for maximum score impact.

One in five Americans has an error on their credit report that is negatively affecting their score. Get your free reports at AnnualCreditReport.com and look for accounts that are not yours, incorrect late payments, or balances that have been paid off but still show as open. Disputing and removing errors can raise your score significantly within 30–45 days.

Ask a family member or trusted friend with excellent credit to add you as an authorized user on their oldest, lowest-utilization credit card. Their positive payment history on that card gets added to your credit report. You do not even need to use the card — just being listed as an authorized user is enough.

If you have been a responsible cardholder for 6+ months, call your credit card issuer and request a credit limit increase. If approved, your utilization ratio drops immediately — even if your balance stays the same. Most issuers will do a soft pull for this request, meaning no impact to your score.

Payment history is 35% of your score — the single largest factor. One missed payment can drop your score by 60–110 points and stays on your report for 7 years. Set up autopay for at least the minimum payment on every account so you never miss a due date.

Answer 3 quick questions and get a personalized recommendation in seconds.

Paying down balances and disputing errors can show results within 30–60 days. Building a strong payment history takes 12–24 months of consistent on-time payments. The good news: once you hit 700+, you will qualify for the best credit card rewards and the lowest loan rates available.

WiseIQ's editorial team researches and fact-checks all content using primary sources. Our recommendations are based on independent analysis and are not influenced by advertiser relationships.

Last reviewed: April 2026 | How we rank products

| Action | Timeline | Potential Score Impact |

|---|---|---|

| Pay down credit card to under 10% utilization | 1 billing cycle (30–45 days) | +20 to +80 points |

| Remove error from credit report | 30–60 days | +20 to +100 points |

| Experian Boost | Immediate | +5 to +15 points (Experian only) |

| Become authorized user | 1–2 billing cycles | +20 to +50 points |

| 6 months of on-time payments | 6 months | +30 to +60 points |

| Open secured card + 12 months of payments | 12 months | +40 to +80 points |

| Late payment ages 2+ years | 24 months | Impact significantly reduced |

The credit repair industry is full of misleading claims. Here's what to ignore:

"We can remove accurate negative items from your report." No one can legally remove accurate, verified negative information before its natural expiration date (7 years for most items, 10 years for Chapter 7 bankruptcy). If a company claims otherwise, it's a scam.

"Pay for deletion" on collections. Some collection agencies will agree to remove a collection from your report if you pay in full — this is called "pay for deletion." It's not illegal, but it's not guaranteed, and the major bureaus have policies against it. Under FICO 9, paid collections don't affect your score anyway. Focus on disputing inaccurate collections rather than paying for deletion.

Rapid rescore services. These are legitimate but only available through mortgage lenders — you can't access them directly. They're used to quickly update your score before a home purchase closes. They don't add new positive information; they just speed up the processing of changes you've already made.

Red flags for credit repair scams: Any company that asks for payment before providing services, guarantees a specific score increase, tells you to dispute accurate information, or suggests creating a "new" credit identity (using an Employer Identification Number instead of your SSN) is operating illegally. Report these companies to the FTC at ReportFraud.ftc.gov.

The financial stakes of your credit score are higher than most people realize. Here's what the same $30,000 auto loan costs at different credit scores:

| Credit Score | Typical Auto APR | Monthly Payment | Total Interest (60 mo) |

|---|---|---|---|

| 750+ (Excellent) | 5.5% | $574 | $4,440 |

| 700–749 (Good) | 8.5% | $616 | $6,960 |

| 650–699 (Fair) | 13.5% | $686 | $11,160 |

| Below 600 (Poor) | 21% | $809 | $18,540 |

The difference between excellent credit and poor credit on a $30,000 auto loan is $14,100 in extra interest — more than the down payment on the car. On a $300,000 mortgage, the same gap can exceed $100,000 over the life of the loan. Improving your credit score is one of the highest-return financial actions you can take.

Use our free Credit Score Simulator to model the impact of paying down debt, opening new accounts, or disputing errors — before you take action.

Try the Simulator — Free →The fastest improvements come from paying down credit card balances — this can show results within 30 days since utilization updates monthly. Disputing errors can improve your score within 30–45 days. Recovering from a missed payment or collection takes 12–24 months. There is no legitimate way to improve your score overnight.

The two highest-impact actions are: (1) reducing credit card utilization below 10% — this affects 30% of your score and can add 20–50 points quickly, and (2) maintaining a perfect on-time payment history — this affects 35% of your score and compounds over time. Everything else is secondary.

Paying off a loan generally has a modest positive effect on your score over time. However, in the short term, it may slightly decrease your score because it reduces your credit mix (the variety of account types). The long-term benefit of being debt-free and having a positive payment history outweighs any temporary dip.

No legitimate company can remove accurate negative information from your credit report before it naturally expires. Credit repair companies that promise to 'erase' bad credit are often scams. You can dispute genuine errors yourself for free through AnnualCreditReport.com — the same process credit repair companies use.

You are entitled to one free credit report per year from each of the three major bureaus (Equifax, Experian, TransUnion) through AnnualCreditReport.com — the only federally authorized source. During COVID, the bureaus began offering free weekly reports, which has continued. Monitoring services like Credit Karma also provide free ongoing access.