Your credit score is a three-digit number that lenders use to evaluate how likely you are to repay debt. The most widely used scoring model is the FICO Score, which ranges from 300 to 850. A higher score means better rates, higher approval odds, and more financial options. Here's what each range means in practice.

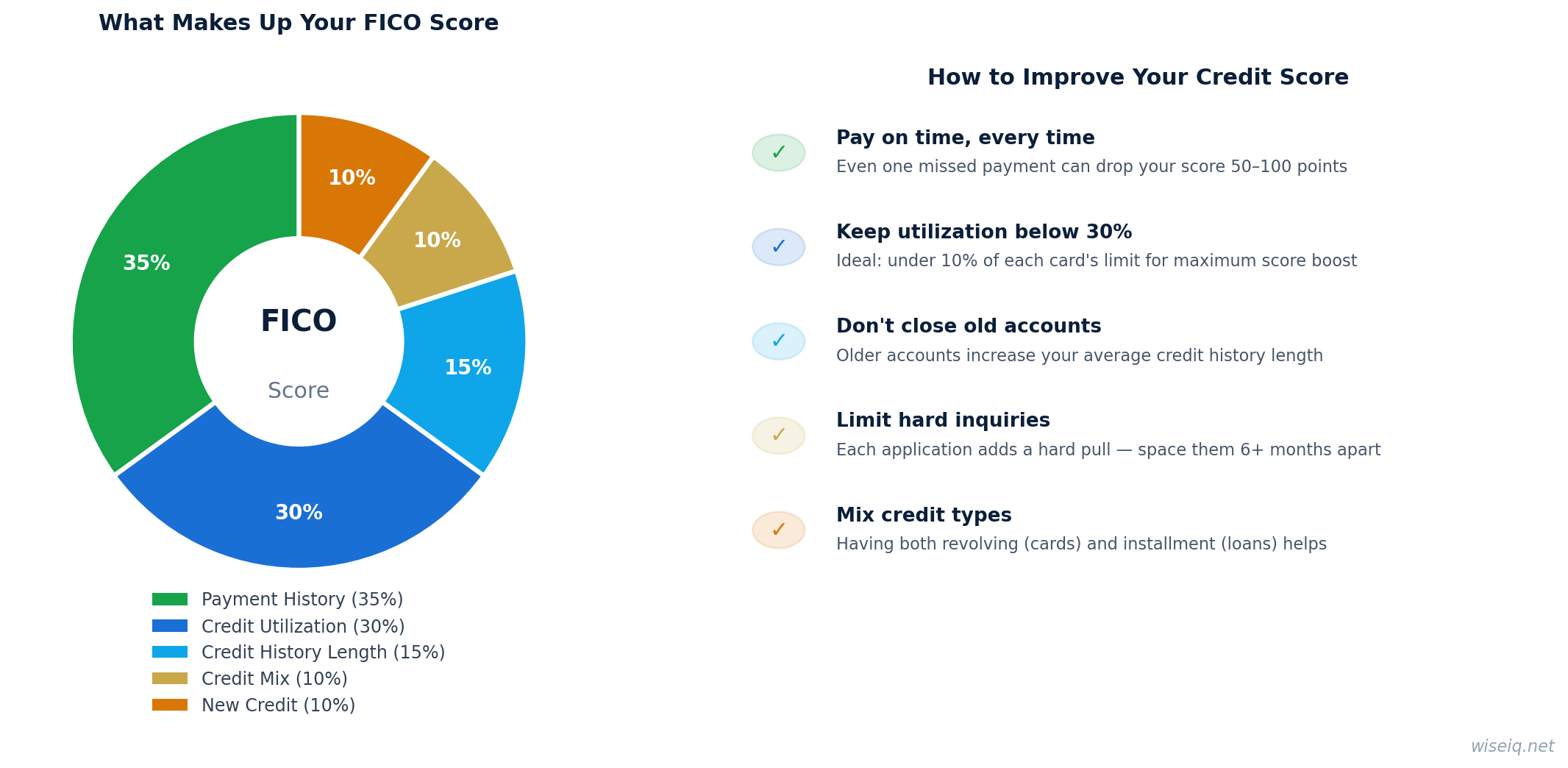

Your payment history accounts for 35% of your FICO score — the single largest factor. Setting up autopay for at least the minimum payment eliminates the risk of a missed payment tanking your score.

| FICO Score Range | Rating | What You Can Qualify For |

|---|---|---|

| 800–850 | Exceptional | Best rates on all products; premium credit cards; lowest mortgage rates |

| 740–799 | Very Good | Near-best rates; most premium cards; excellent loan terms |

| 670–739 | Good | Most rewards cards; competitive loan rates; standard mortgage rates |

| 580–669 | Fair | Some rewards cards; higher interest rates; FHA mortgage (580+) |

| 500–579 | Poor | Secured cards; credit builder loans; FHA mortgage with 10% down |

| 300–499 | Very Poor | Secured cards only; credit builder products; no traditional loans |

FICO Score vs VantageScore — What's the Difference?

Most lenders use FICO Scores, but some use VantageScore. Both range from 300–850 and use similar factors, but the exact calculations differ. When a lender says they check your "credit score," they almost always mean your FICO Score. Credit monitoring apps like Credit Karma typically show your VantageScore, which may be slightly different from your FICO Score.

| Score Range | FICO Rating | VantageScore Rating |

|---|---|---|

| 781–850 | Exceptional | Excellent |

| 740–780 | Very Good | Good |

| 670–739 | Good | Good |

| 580–669 | Fair | Fair |

| 500–579 | Poor | Poor |

| 300–499 | Very Poor | Very Poor |

What Factors Make Up Your Credit Score?

| Factor | FICO Weight | What It Means |

|---|---|---|

| Payment History | 35% | Whether you pay on time — the single most important factor |

| Amounts Owed (Utilization) | 30% | How much of your available credit you're using — keep below 10% |

| Length of Credit History | 15% | How long your accounts have been open — older is better |

| Credit Mix | 10% | Having both revolving (cards) and installment (loans) accounts |

| New Credit | 10% | Recent applications and hard inquiries — minimize these |

Related Articles & Guides

Answer 3 quick questions and get a personalized recommendation in seconds.

What Credit Score Do You Need for Major Financial Products?

| Financial Product | Minimum Score | Best Rate Score |

|---|---|---|

| Secured Credit Card | No minimum | N/A |

| Basic Unsecured Card | 580+ | N/A |

| Rewards Credit Card | 670+ | 720+ |

| Premium Travel Card | 720+ | 740+ |

| Personal Loan (competitive rate) | 640+ | 720+ |

| Auto Loan (good rate) | 660+ | 720+ |

| FHA Mortgage | 500+ (10% down) / 580+ (3.5% down) | 740+ |

| Conventional Mortgage | 620+ | 740+ |

| Apartment Rental | 620+ | 680+ |

Check Your Credit Score — Free, No Credit Pull

Frequently Asked Questions

What is considered a good credit score?

What credit score do you need to buy a house?

What credit score do you need for a credit card?

How often does your credit score update?

Does checking your credit score lower it?

Sources & Methodology

WiseIQ's editorial team researches and fact-checks all content using primary sources. Our recommendations are based on independent analysis and are not influenced by advertiser relationships.

- Consumer Financial Protection Bureau (CFPB)

- Federal Reserve — Consumer Credit Report (G.19)

- myFICO Credit Education

- Issuer and lender websites — rates, terms, and eligibility verified directly from source

Last reviewed: April 3, 2026 | How we rank products