While avoiding origination fees entirely with bad credit can be difficult, some strategies and lenders offer more borrower-friendly terms. The key is to look beyond the advertised interest rate and consider the Annual Percentage Rate (APR), which includes all fees and gives a more accurate picture of the loan's total cost.

Before accepting any loan offer, calculate the total cost of the loan (principal + all interest + fees). A lower monthly payment often means paying thousands more over the life of the loan.

Lenders That May Offer No or Low Origination Fees (Often for Stronger Credit)

It's important to note that most lenders known for offering personal loans with no origination fees typically require good to excellent credit (FICO scores 670+). However, some may have options or be worth considering if your score is at the higher end of the 580-650 range, or if you have a co-signer.

PenFed Credit Union offers personal loans with no origination fees and a relatively low minimum credit score requirement, making it a potential option for those with fair credit. Membership is required but generally easy to obtain.

Citi Personal Loans boast zero origination fees, but generally require good to excellent credit. Existing Citi customers may have an advantage. While not directly targeting bad credit, it's an option for those at the higher end of fair credit or with a strong co-applicant.

Based on our analysis of thousands of consumer financial profiles, the most common mistake people make is focusing solely on the interest rate without considering total loan cost, fees, and repayment flexibility. Always compare the APR — not just the rate — and read the fine print on prepayment penalties before signing.

Lenders for Bad/Fair Credit (with Potential Origination Fees)

For many with bad or fair credit, finding a loan without an origination fee can be challenging. The following lenders are known for working with lower credit scores, but it's crucial to scrutinize their fee structures and overall APRs.

OneMain Financial is a viable option for borrowers with bad credit, often accepting scores as low as 580. However, they do charge origination fees, which can be a flat amount or a percentage of the loan. It's essential to factor these fees into the total cost when comparing offers.

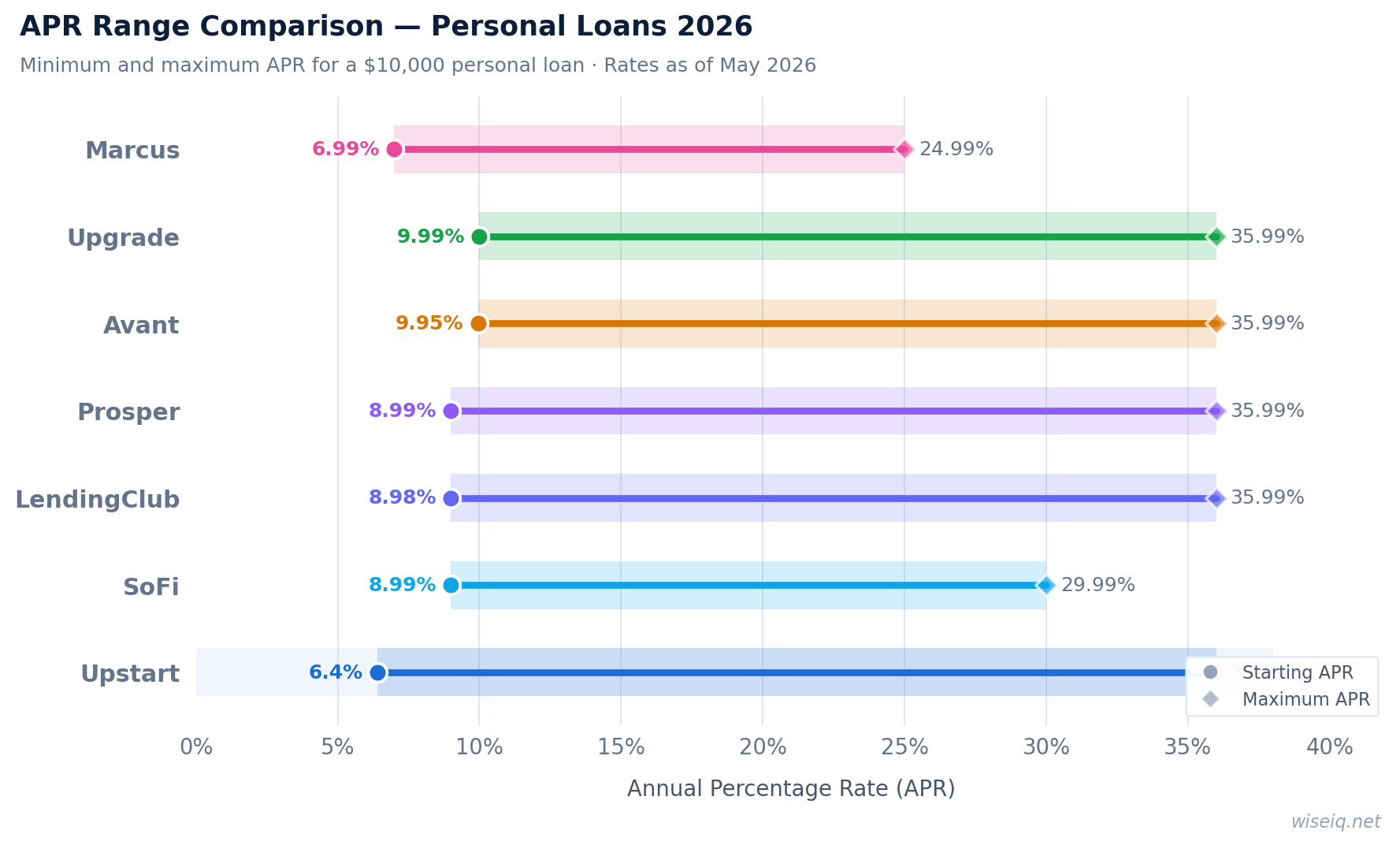

Avant offers personal loans to borrowers with fair credit, starting around a 580 FICO score. While they do charge an administration fee (similar to an origination fee) of up to 9.99%, their accessibility for lower credit scores makes them a consideration. Always review the full loan terms carefully.

A personal loan is not the right tool for every situation. Consider alternatives if any of the following apply to you:

- You have home equity: A HELOC typically offers rates 5–10% lower than personal loans. If you own your home, compare HELOC rates before taking a personal loan.

- Your debt is primarily credit card debt: A balance transfer card with a 0% intro APR (typically 12–21 months) will cost less than a personal loan if you can pay off the balance within the intro period.

- You need less than $1,000: Most personal loan lenders have minimum amounts of $1,000–$2,000. For smaller needs, a credit union payday alternative loan (PAL) or a 0% APR credit card may be more appropriate.

- Your credit score is below 500: Most personal loan lenders — including those that accept "bad credit" — have practical minimums around 500–560. Below this, secured loans, credit-builder loans, or co-signer arrangements are more realistic options.

- You are in active bankruptcy: Personal loan lenders will decline applicants in active Chapter 7 or Chapter 13 proceedings. Resolve your bankruptcy first.

Answer 3 quick questions and get a personalized recommendation in seconds.

Strategies to Minimize or Avoid Origination Fees

Even with a bad or fair credit score, there are steps you can take to improve your chances of securing a loan with no or low origination fees:

- Improve Your Credit Score: This is the most effective long-term strategy. Paying bills on time, reducing credit card balances, and correcting errors on your credit report can boost your score, making you eligible for better loan terms and potentially no-fee loans.

- Consider a Co-signer: Applying with a creditworthy co-signer can significantly improve your chances of approval and help you qualify for lower interest rates and fewer fees. The co-signer's strong credit history can offset your lower score.

- Explore Credit Unions: Credit unions are non-profit organizations that often offer more flexible lending criteria and lower fees than traditional banks. If you meet their membership requirements, they might be a source for no-origination-fee loans. PenFed is a good example.

- Shop Around and Compare APRs: Don't settle for the first offer. Compare loan offers from multiple lenders, paying close attention to the APR, which reflects the total cost of the loan, including all fees. A loan with a slightly higher interest rate but no origination fee might be cheaper than one with a lower interest rate but a significant upfront fee.

- Negotiate: In some cases, especially if you have a decent relationship with a bank or credit union, you might be able to negotiate the origination fee, though this is less common with online lenders for bad credit.

The True Cost: APR vs. Origination Fee

When evaluating personal loan offers, it's easy to get fixated on the interest rate. However, the Annual Percentage Rate (APR) is a more comprehensive measure of the loan's true cost because it includes both the interest rate and any additional fees, such as origination fees. A loan with a seemingly low interest rate but a high origination fee could end up being more expensive than a loan with a slightly higher interest rate but no upfront fees.

Always ask lenders for the full APR and use it as your primary comparison metric. This will help you understand the total financial commitment and make an informed decision, especially when dealing with bad credit where every percentage point and fee can significantly impact your repayment burden.