Advertiser Disclosure: WiseIQ is reader-supported. When you apply through links on this page, we may earn a commission at no extra cost to you. Learn more.

DEBT CONSOLIDATION

Best Debt Consolidation Loans for 2026

Sorted by APR. These are today's best rates for your loan amount.

Filtered for lenders most likely to approve your application.

Sorted by funding speed. Same-day and next-day options highlighted.

Personal loans built for debt consolidation — lower rates than most credit cards.

We've simplified the comparison to the top 3 options for first-time borrowers.

Based on your browsing, here are the top picks most users in your position chose.

LIVE RATE7.49% APRfor qualified borrowers · No hard credit pull

📋 Reviewed by WiseIQ Editorial Team · Updated April 2026 · Editorially independent

Debt consolidation means taking out a single personal loan to pay off multiple high-interest debts — typically credit cards. If you can get a loan at a lower APR than your current debts, you'll save money on interest and simplify your monthly payments.

WiseIQ Expert Tip

The avalanche method (paying highest-interest debt first) saves the most money mathematically. The snowball method (smallest balance first) works better for motivation. Choose the one you will actually stick with.

$6,501

Avg. CC Debt

20.68%

Avg. APR

3–5 yrs

Payoff Timeline

SoFi Personal LoanNo fees, rates from 8.99% APR, unemployment protection

WiseIQ's editorial team evaluated each option based on annual fees, rewards rates, approval requirements, customer service ratings, and overall value for the target user. All rates and terms are verified as of April 2026.

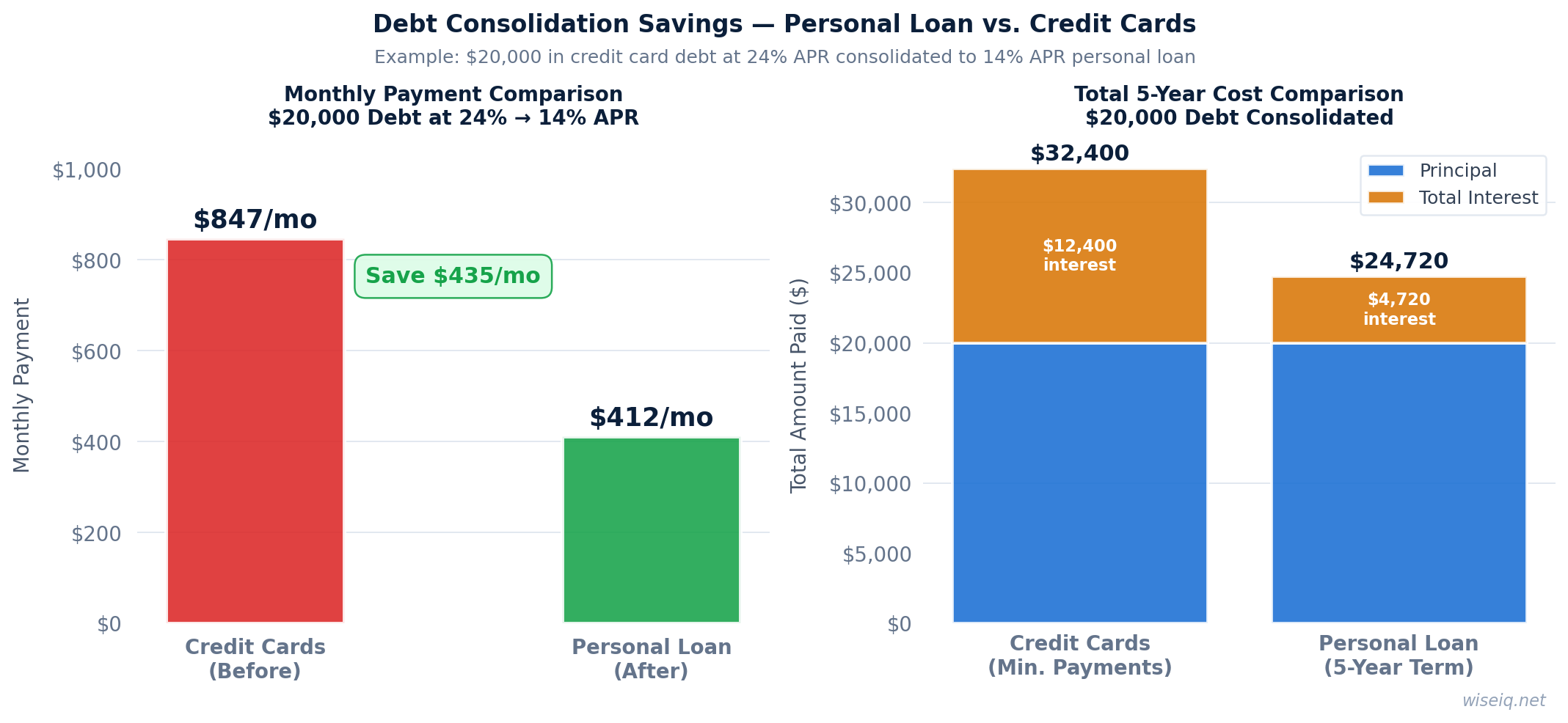

Debt Consolidation Savings: Consolidating $20,000 in credit card debt (24% APR) to a personal loan (14% APR) saves $435/month and $7,680 in total interest.

⚠️ Important: Debt consolidation works best when combined with a budget that prevents new debt accumulation. Address the root cause, not just the symptoms.

Upgrade580+ credit score, direct payment to creditors

We monitor rates across 50+ lenders and alert you when better options become available for your profile.

No spam. Unsubscribe anytime. We never sell your data.

W

WiseIQ Editorial Team

Reviewed by Certified Financial Planners & Industry Experts

Our editorial team consists of financial writers, CFPs, and former banking professionals dedicated to providing accurate, unbiased financial guidance. All content is fact-checked and updated regularly. Learn about our editorial standards →

Frequently Asked Questions

Does debt consolidation hurt your credit?

Applying for a debt consolidation loan triggers a hard inquiry (5–10 point temporary drop). However, paying off credit cards reduces your utilization ratio, which can significantly boost your score within 30–60 days.

What credit score do I need for a debt consolidation loan?

Most lenders require 580–660 for debt consolidation loans. LightStream and SoFi require 650–660+; Upgrade accepts 580+.

Is debt consolidation a good idea?

Debt consolidation makes sense if you can get a lower APR than your current debts. If your credit cards charge 20–25% APR and you can get a personal loan at 12–15%, you'll save significantly on interest.

What's the difference between debt consolidation and debt settlement?

Debt consolidation means taking a new loan to pay off existing debts — you still pay the full amount owed. Debt settlement means negotiating with creditors to pay less than you owe, which severely damages your credit score.

Most personal loan lenders require a minimum score of 580–640. The best rates (under 10% APR) typically require a score of 720+. Some lenders like Upstart consider education and employment history alongside credit scores, making them accessible to borrowers with limited credit history.

Online lenders like Upstart can approve and fund loans in as little as 1–3 business days. Traditional banks may take 1–2 weeks. Pre-qualification takes just minutes and uses a soft credit pull that won't affect your score.

The average personal loan APR is 11–12% for borrowers with good credit. Rates range from 6% for excellent credit to 36% for poor credit. Always compare at least 3 lenders before accepting an offer — rates vary significantly between lenders for the same credit profile.

Yes — lenders like Upstart, Avant, and OneMain Financial specialize in loans for borrowers with scores below 640. Expect higher rates (20–36% APR) and consider a co-signer to improve your terms. Improving your score by even 30–50 points before applying can significantly reduce your rate.