Securing a $15,000 personal loan can provide the financial flexibility you need for various life events. Whether you're looking to consolidate high-interest credit card debt, finance a significant home improvement project, or cover unexpected medical bills, a fifteen thousand dollar loan offers a structured repayment plan. This guide will walk you through finding the best $15,000 loan rates in 2026, understanding monthly payment on $15000 loan scenarios, and exploring options even if you have fair credit or are seeking a 15000 loan bad credit solution. We'll also delve into how lenders like Upstart utilize AI underwriting to offer more inclusive lending opportunities, considering factors beyond just your FICO score.

Expert Tip: Always prequalify with multiple lenders to compare personalized offers without impacting your FICO score. This soft credit pull allows you to see potential annual percentage rates (APRs) and loan terms upfront, helping you avoid unnecessary hard credit inquiry marks on your report.

How to Get the Best $15,000 Personal Loan in 2026

Finding the ideal $15,000 personal loan involves more than just looking for the lowest APR. It requires understanding the full scope of loan terms, potential origination fees, and how different lenders assess your creditworthiness. Here's a step-by-step guide to help you secure a great 15000 dollar loan:

1. Check Your Credit and Financial Health

Your FICO score is a major factor in determining your eligibility and interest rate. Lenders typically prefer higher scores, but some, like Upstart, consider non-traditional credit factors. Knowing your score helps you target appropriate lenders, especially if you're looking for a 15000 loan fair credit or 15000 loan bad credit. Also, assess your debt-to-income ratio to understand your capacity for a new monthly payment.

2. Prequalify with Multiple Lenders

Utilize prequalification services to get personalized rate estimates without a hard credit inquiry. This crucial step allows you to compare various $15,000 loan rates from different providers like Upstart, SoFi, and LendingClub, helping you find the most competitive annual percentage rate (APR) and favorable loan term. It's a soft credit pull that won't harm your credit.

3. Compare Loan Offers Thoroughly

Look beyond just the APR. Consider the total cost of the loan, including any origination fee, and the overall monthly payment. A longer loan term might mean lower monthly payments but higher overall interest. Evaluate the prepayment penalty policies as well; ideally, choose a lender with no prepayment penalty to maintain flexibility.

4. Submit Your Application and Get Funded

Once you've chosen a lender, complete the full application. This will involve a hard credit inquiry. Be prepared to provide documentation for income, employment history, and other financial details. Many lenders, especially online platforms, offer next-day funding upon approval, ensuring you get your fifteen thousand dollar loan quickly.

Why Upstart is a Top Choice for a $15,000 Loan

Upstart stands out in the personal loan market, especially for borrowers who might not have a perfect credit history. Their innovative approach to lending makes them a strong contender for a $15,000 personal loan. Here's why:

- AI Underwriting: Upstart uses artificial intelligence to assess more than just your FICO score. They consider your education-based lending potential, employment history, and other non-traditional credit factors, which can lead to approval for borrowers with fair credit or limited credit history. This unique approach broadens access to credit for many.

- Competitive APRs: While their APR range is 6.40%–35.99%, many qualified borrowers can secure favorable $15,000 loan rates. The actual annual percentage rate you receive will depend on your individual profile, including your income, education, and credit history.

- Flexible Loan Terms: Upstart offers various loan terms, allowing you to choose a monthly payment that fits your budget. They also have no prepayment penalty, giving you the flexibility to pay off your loan early and save on interest without incurring extra fees.

- Fast Funding: Approved applicants often receive next-day funding, making Upstart an excellent option if you need quick access to your $15,000 for urgent expenses or opportunities.

- Transparent Fees: Upstart charges an origination fee ranging from 0%–12% origination fee, which is deducted from your loan proceeds. They are transparent about all costs associated with your 15000 dollar loan, ensuring you know exactly what to expect.

Not sure if a $15,000 loan is right for you?

Take our quick quiz to find out which loan amount and type best suits your financial situation. Understand your options for debt consolidation 15000 or a home improvement 15000 project.

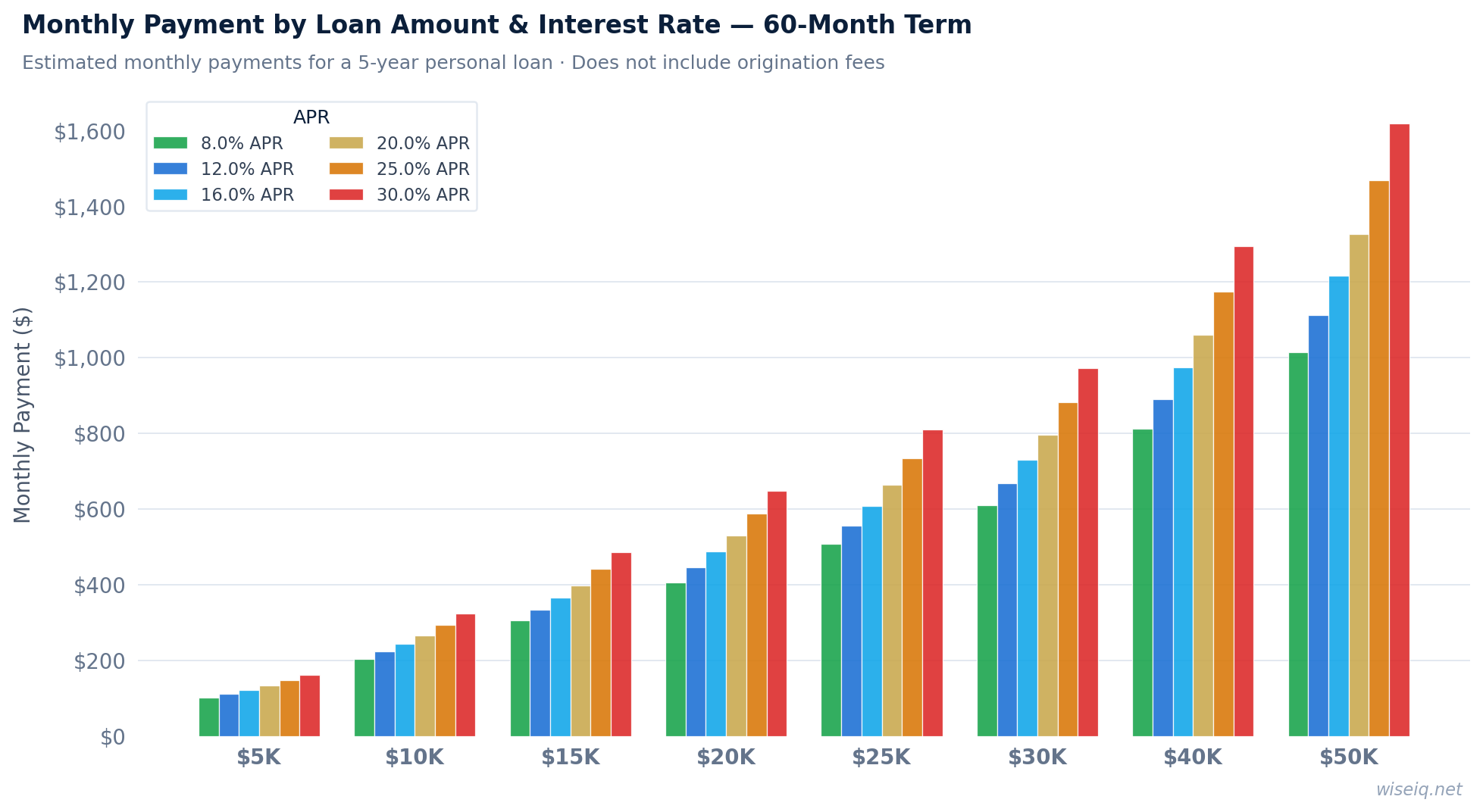

Start Quiz Now$15,000 Personal Loan Rates and Monthly Payments

Understanding the potential monthly payment on $15000 loan is crucial for budgeting. The table below illustrates estimated monthly payments based on different APRs and loan terms. Remember that these are estimates, and your actual rates will depend on your credit profile and the lender's assessment. Factors like your debt-to-income ratio and employment history also play a role in determining your final annual percentage rate.

| Lender | Starting APR | Loan Term | Est. Monthly Payment ($15k) |

|---|---|---|---|

| Upstart | 6.40% | 3-5 Years | $290 - $458 |

| SoFi | 8.99% | 2-7 Years | $250 - $480 |

| LendingClub | 9.57% | 3-5 Years | $315 - $485 |

| Example (12% APR) | 12.00% | 3 Years | $498 |

| Example (12% APR) | 12.00% | 5 Years | $334 |

Eligibility and Requirements for a $15,000 Loan

To qualify for a $15,000 personal loan, lenders will evaluate several factors. While specific requirements vary, here are the common criteria you'll encounter when seeking a fifteen thousand dollar loan:

- Credit Score: A good FICO score (typically 670+) will give you the best $15,000 loan rates. However, options exist for 15000 loan fair credit (580-669) and even 15000 loan bad credit, especially with lenders like Upstart that use AI underwriting and consider non-traditional credit factors.

- Income and Employment: Lenders want to ensure you have a stable income to make your monthly payment. Your employment history is often reviewed, and a consistent income stream is a key indicator of your ability to repay the loan.

- Debt-to-Income Ratio (DTI): This ratio compares your monthly debt payments to your gross monthly income. A lower DTI indicates you have more disposable income to handle new loan payments, making you a less risky borrower.

- Prequalification: Many lenders offer prequalification, which involves a soft credit pull and gives you an idea of your approval odds and potential annual percentage rate (APR) without affecting your credit score. This is a great way to shop around for the best loan terms.

- Origination Fee: Be aware of any origination fee, which is a one-time charge deducted from your loan proceeds. Upstart's origination fee ranges from 0%–12%. Always factor this into the total cost of your 15000 dollar loan.

- Loan Purpose: While a $15,000 personal loan can be used for almost anything, some common uses include debt consolidation 15000 and home improvement 15000. Clearly defining your purpose can sometimes influence lender offers.

Understanding these requirements will help you prepare your application and increase your chances of approval for a 15000 dollar loan with favorable loan terms and a manageable monthly payment.

Alternatives and How to Improve Your Chances for a $15,000 Loan

If you're struggling to qualify for a $15,000 personal loan or want to secure better terms, consider these alternatives and strategies to improve your financial standing and approval odds:

- Improve Your Credit Score: Paying bills on time, reducing existing debt, and correcting errors on your credit report can boost your FICO score over time. A higher score will significantly improve your access to better $15,000 loan rates and more favorable loan terms.

- Consider a Co-signer: A co-signer with good credit can significantly improve your approval odds and help you secure a lower annual percentage rate (APR), especially if you have fair credit or are seeking a 15000 loan bad credit. The co-signer's strong credit profile can offset perceived risks.

- Secured Loans: These loans require collateral (like a car or savings account) but are often easier to obtain with lower credit scores and may offer more favorable loan terms and lower APRs. However, be aware of the risk of losing your collateral if you default.

- Debt Management Plans: If debt consolidation 15000 is your primary goal, a non-profit credit counseling agency can help you create a debt management plan. This can help you manage your existing debts more effectively and potentially improve your credit over time.

- Explore Credit Unions: Credit unions often have more flexible lending criteria and may offer lower rates than traditional banks, particularly for members. They may be more willing to work with individuals who have a 15000 loan fair credit history.

- Focus on Employment History: A stable and consistent employment history demonstrates reliability to lenders. If you have a strong work record, highlight this in your application, especially with lenders like Upstart that consider it a key factor in their AI underwriting.

Even if you face challenges, there are pathways to obtaining the financial assistance you need. Always be mindful of the loan term and any prepayment penalty when evaluating options for your fifteen thousand dollar loan. A thorough understanding of these elements will help you make the best financial decision.

WiseIQ Editorial Team

The WiseIQ Editorial Team is dedicated to providing accurate, unbiased, and comprehensive financial information to help you make informed decisions about personal loans, debt management, and more. Our experts analyze market trends and lender offerings to bring you the most up-to-date advice on $15,000 personal loan options, annual percentage rates, and strategies for improving your financial health.

Frequently Asked Questions About $15,000 Personal Loans

What is a typical monthly payment on a $15,000 loan?

The monthly payment on a $15000 loan varies significantly based on the loan term and the annual percentage rate (APR). For example, a 3-year loan at 10% APR might have a monthly payment around $484, while a 5-year loan at the same APR could be around $318. Always consider the total interest paid over the loan term, as a longer term often means more interest overall, even with lower monthly payments.

Can I get a $15,000 loan with bad credit?

Yes, it is possible to get a $15,000 loan with bad credit, but it may come with higher interest rates and stricter eligibility requirements. Lenders like Upstart use AI underwriting to consider more than just your FICO score, looking at education and employment history. Exploring options for a 15000 loan bad credit may involve secured loans or co-signers to improve your chances of approval and secure a more favorable annual percentage rate.

What are the best $15,000 loan rates I can expect?

The best $15,000 loan rates typically range from 6% to 36% APR, depending on your creditworthiness, the lender, and the loan term. Borrowers with excellent credit can qualify for the lowest rates, while those with fair credit or bad credit will likely see higher rates. Prequalification can help you see personalized offers without a hard credit inquiry, allowing you to compare various annual percentage rates effectively.

How quickly can I get a $15,000 personal loan?

Many online lenders, including Upstart, offer next-day funding for approved $15,000 personal loans. The speed of funding can depend on your bank and how quickly you complete the application process. Always check with your chosen lender for their specific funding timelines and ensure you have all necessary documentation ready to expedite the process. A soft credit pull during prequalification can also speed up the initial assessment.

What is the difference between a soft credit pull and a hard credit inquiry?

A soft credit pull occurs during prequalification and does not affect your FICO score. It allows lenders to give you an idea of potential rates and loan terms. A hard credit inquiry happens when you formally apply for a loan and can temporarily lower your credit score by a few points. It's important to understand this distinction when comparing $15,000 loan rates and deciding which lenders to apply with, as too many hard inquiries can negatively impact your creditworthiness.

Can I use a $15,000 personal loan for debt consolidation?

Absolutely. A $15,000 personal loan for debt consolidation is a common use case. It allows you to combine multiple high-interest debts into a single, more manageable monthly payment, often at a lower overall annual percentage rate (APR). This can simplify your finances, potentially save you money on interest, and make it easier to track your repayment progress. Many lenders, including Upstart, offer competitive options for debt consolidation 15000.

What is an origination fee and how does it affect a $15,000 loan?

An origination fee is a one-time charge levied by a lender for processing your loan application. It's typically a percentage of the total loan amount and is deducted from your loan proceeds before you receive the funds. For a $15,000 personal loan, an origination fee of, say, 5% would mean you receive $14,250. Upstart's origination fee ranges from 0%–12%. Always factor this fee into your calculations to understand the true cost of your fifteen thousand dollar loan.

Does a $15,000 personal loan have a prepayment penalty?

Many modern personal loans, especially from online lenders like Upstart, do not have a prepayment penalty. This means you can pay off your $15,000 personal loan early without incurring extra charges, potentially saving you a significant amount on interest over the loan term. However, it's crucial to confirm this policy with your chosen lender before signing any agreements, as some traditional banks or older loan products might still include them.

Disclaimer: The information provided on this page is for informational purposes only and does not constitute financial advice. Loan approval, interest rates, and terms are subject to lender review and your individual creditworthiness. Always read the terms and conditions carefully before accepting any loan offer. WiseIQ does not guarantee specific rates or approval. The annual percentage rate (APR), origination fee, and loan term can vary significantly based on your FICO score, debt-to-income ratio, and other factors considered by lenders, including non-traditional credit factors and employment history. Be aware of any potential prepayment penalty, though many lenders offer loans with no such fees. A soft credit pull is generally used for prequalification, while a hard credit inquiry is part of the final application process.