Getting a personal loan can provide the financial flexibility you need, whether for debt consolidation, home improvements, or unexpected expenses. When considering lenders, understanding the **Upstart loan requirements** is crucial, especially since their approach differs significantly from conventional banks. Upstart utilizes a sophisticated **AI underwriting** model that looks beyond just your credit score, taking into account your educational background, area of study, and job history. This innovative method aims to provide access to credit for a wider range of borrowers, including those with limited credit files or those who might be overlooked by traditional lenders. This comprehensive guide will walk you through everything you need to know about qualifying for an Upstart personal loan in 2026, from **minimum income requirements** to residency and **employment requirements**. We will delve into how Upstart's unique model assesses your creditworthiness, the specific criteria you need to meet, and what you can expect during the application process. By the end of this guide, you'll have a clear understanding of whether an Upstart personal loan is the right financial solution for you.

Expert Tip: Boost Your Upstart Approval Odds

While Upstart doesn\'t require a minimum FICO score, a strong **employment history** and a higher educational attainment can significantly improve your chances of approval and secure a lower **annual percentage rate (APR)**. Ensure all your application details are accurate and reflect your full financial picture, including any non-traditional credit factors that might strengthen your profile. Consider highlighting any specialized skills or certifications that demonstrate your earning potential, as Upstart's **AI underwriting** model is designed to recognize these attributes.

Understanding Upstart Eligibility: Beyond the Credit Score

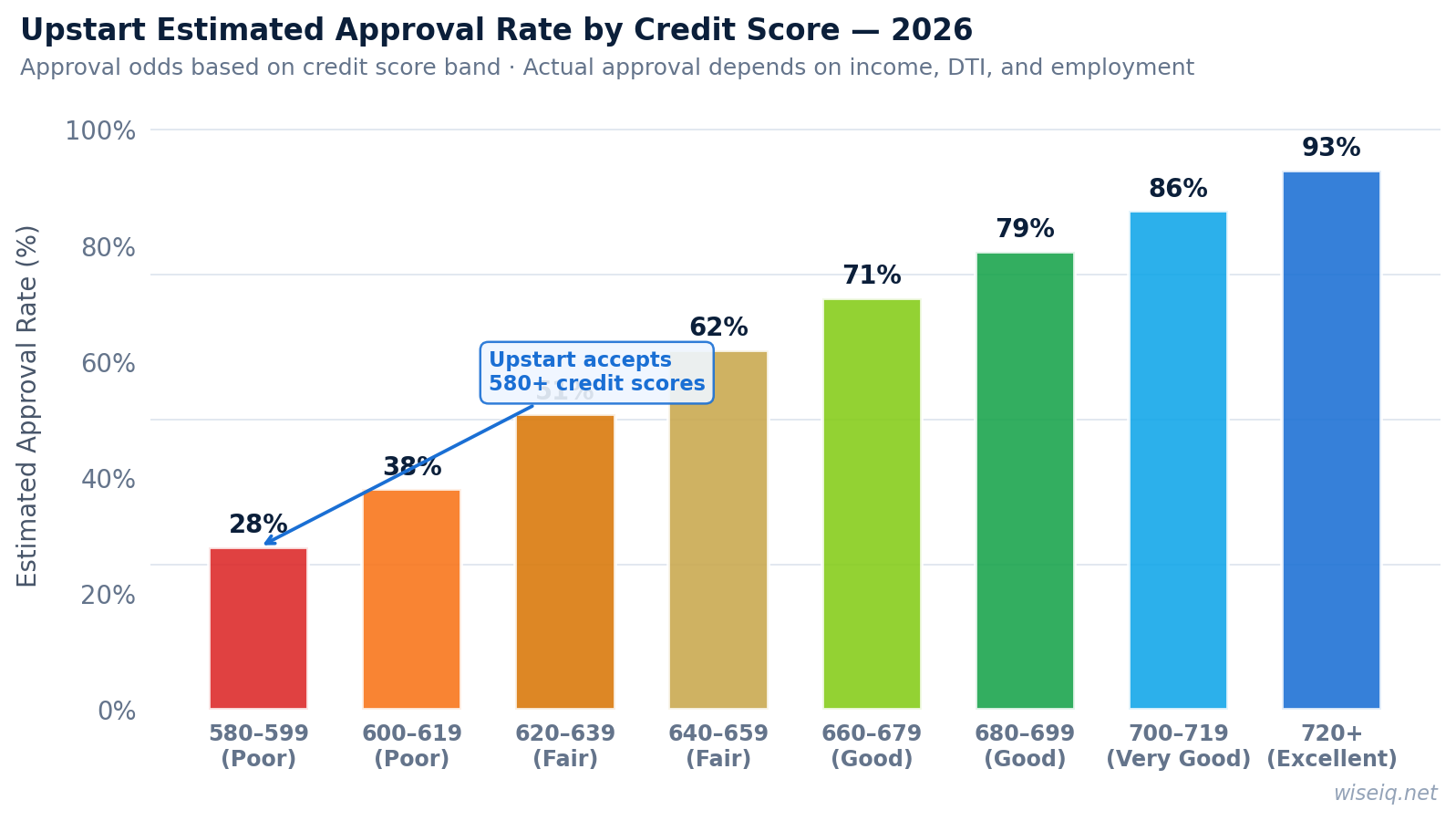

One of the most compelling aspects of Upstart is its commitment to inclusive lending. While many lenders focus solely on your **FICO score**, Upstart\'s **AI underwriting** model analyzes over 1,600 data points. This includes traditional factors like your **debt-to-income ratio** and credit history, but also extends to **non-traditional credit factors** such as your education, major, and job experience. This holistic view can be particularly beneficial for young professionals or individuals with a **fair credit** score who might struggle to get approved elsewhere. This innovative approach allows Upstart to identify creditworthy individuals who may be overlooked by conventional lending models, offering them a chance to access affordable credit. It's a game-changer for those looking to establish credit or rebuild their financial standing.

Key Upstart Loan Requirements for 2026

To be eligible for an Upstart personal loan, applicants must meet several fundamental criteria. These requirements ensure that borrowers are in a stable financial position to repay their loans. Here’s a detailed breakdown of what Upstart looks for:

1. Age Requirement

- You must be at least 18 years old (19 in Alabama and Nebraska). This is a standard legal requirement for entering into loan agreements.

2. Residency and Bank Account Requirement

- You must be a U.S. citizen or permanent resident. This ensures compliance with federal lending regulations.

- You must have a valid U.S. bank account. This is essential for receiving loan funds and making **monthly payment**s.

- You must have a verifiable email address. This is used for communication and official loan documentation.

3. Minimum Income Requirement

- Applicants generally need a **minimum income of $12,000 per year**. This threshold helps Upstart assess your ability to make consistent **monthly payment**s.

- This income can be from full-time employment, part-time employment, or other regular income sources. Upstart is flexible in considering various forms of verifiable income.

- Upstart considers your income potential, which is a key component of their **AI underwriting** model. This means they look at your future earning capacity, not just your current income.

4. Credit Score Requirement

- Upstart does not have a strict **minimum credit score requirement**. This is a significant differentiator from traditional lenders.

- They accept applicants with no credit history or **fair credit**. This opens up opportunities for many who would otherwise be denied.

- However, a higher credit score can still lead to more favorable terms and a lower **APR**. While not mandatory, a good credit history can certainly benefit you.

- They perform a **soft credit pull** during **prequalification**, which doesn\'t affect your credit score, and a **hard credit inquiry** if you accept a loan offer. This allows you to check your rates risk-free.

5. Employment Requirement

- You must have a full-time job, a full-time job offer starting within six months, or a regular part-time job. Consistent employment demonstrates financial stability.

- Alternatively, you can demonstrate other sources of regular income. This provides flexibility for freelancers or those with diverse income streams.

- Your **employment history** is a significant factor in Upstart\'s assessment, as it provides insight into your stability and earning potential.

6. Debt-to-Income Ratio

- While not a strict cutoff, Upstart evaluates your **debt-to-income ratio** to ensure you can comfortably manage new **monthly payment** obligations. A lower DTI indicates a healthier financial standing.

- A high **debt-to-income ratio** might indicate that taking on additional debt could be a strain, and Upstart aims to lend responsibly.

The Upstart Application Checklist: What You\'ll Need for a Smooth Process

Preparing your documents and information beforehand can streamline the application process and increase your chances of quick approval. Here\'s a detailed **application checklist** to help you get started:

- Personal Information: Your full legal name, date of birth, current residential address, phone number, and email address. Accuracy is key here.

- Proof of Identity: A valid government-issued identification, such as a driver\'s license, state ID, or passport. This is crucial for verifying your identity and preventing fraud.

- Income Verification: Recent pay stubs, bank statements, tax returns (if self-employed), or other official documents that verify your income. Upstart needs to confirm your **minimum income requirement**.

- Employment Details: Your current employer\'s name, your job title, start date, and annual salary. If you have a job offer, be prepared to provide documentation. Your **employment history** is a strong indicator of stability.

- Education History: Details about your highest degree obtained, the institution you attended, and your graduation year. This information is vital for Upstart\'s **education-based lending** model.

- Bank Account Information: Your bank\'s routing number and your account number for direct deposit of loan funds and automatic **monthly payment**s. This fulfills the **bank account requirement**.

Upstart\'s **prequalification** process allows you to check your potential rates without impacting your credit score, as it only involves a **soft credit pull**. This is a great way to gauge your approval odds before committing to a full application that involves a **hard credit inquiry**. This initial step is highly recommended to understand your options without any commitment.

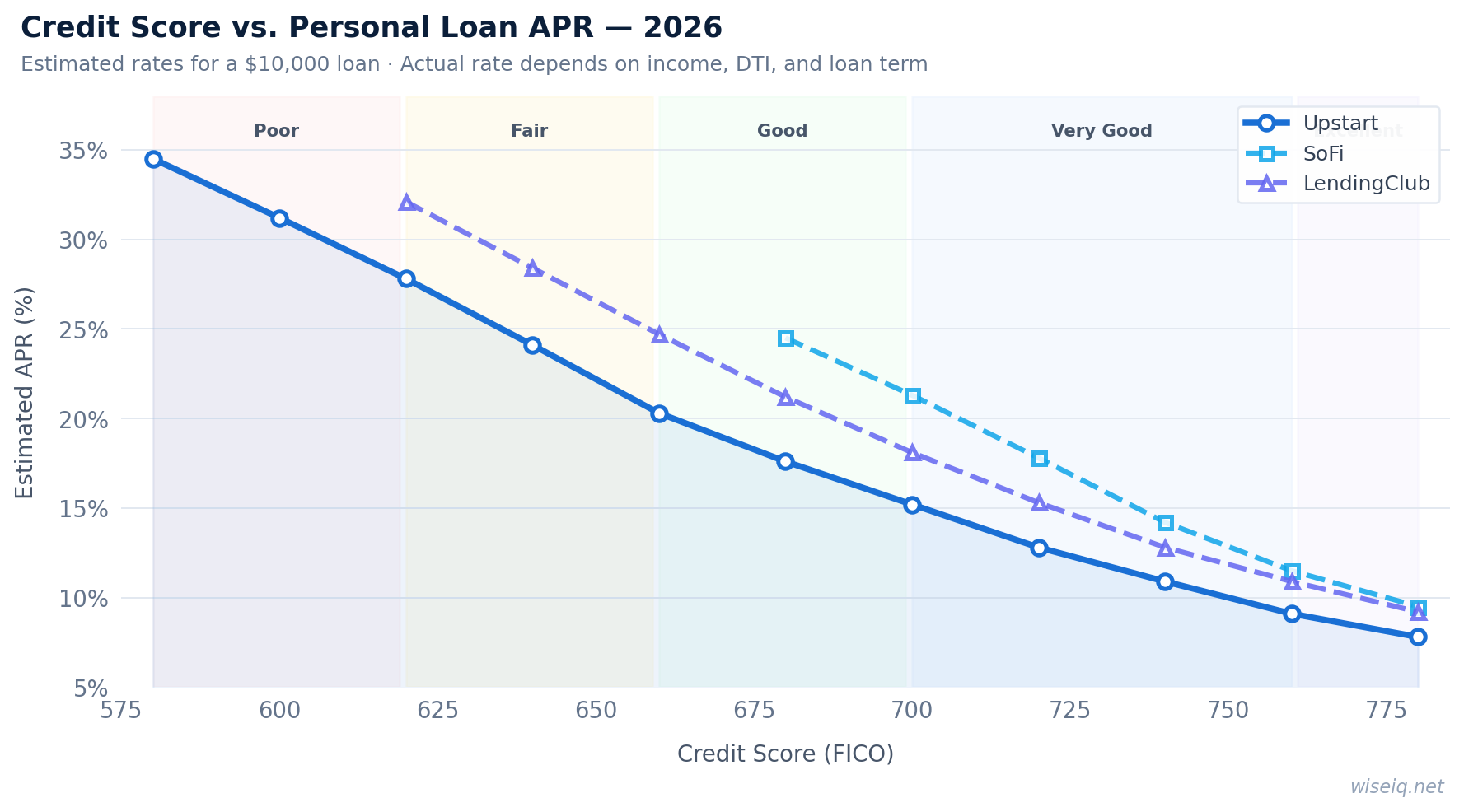

Upstart Loan Details: Rates, Fees, and Terms Explained

Understanding the financial specifics of an Upstart loan is just as important as meeting the **Upstart eligibility** criteria. Here’s a comprehensive look at what you can expect regarding costs and repayment, including the **annual percentage rate** and **origination fee**:

| Feature | Details |

|---|---|

| Loan Range | $1,000 – $75,000 |

| APR Range | 6.40% – 35.99% |

| Origination Fee | 0% – 12% (deducted from loan proceeds) |

| Loan Term | 3 or 5 years (36 or 60 months) |

| Prepayment Penalty | None |

| Minimum Income | $12,000/year |

| Minimum Credit Score | None (AI underwriting considers other factors) |

| Funding Speed | As fast as **next-day funding** (after acceptance) |

Upstart\'s **origination fee** can range from 0% to 12%, which is deducted from your loan proceeds. This fee varies based on your creditworthiness and other factors assessed by their **AI underwriting** model. It's important to factor this into the total cost of your loan. Importantly, there is **no prepayment penalty**, meaning you can pay off your loan early without incurring additional charges, potentially saving significantly on total interest. The **loan term** is typically 3 or 5 years (36 or 60 months), allowing for manageable **monthly payment** options that fit your budget. The **annual percentage rate (APR)** you receive will be determined by a variety of factors, including your credit profile, income, and the loan term you choose. Upstart aims to offer competitive rates, especially for those with strong **non-traditional credit factors**.

Ready to see what rates you qualify for? Don't let a limited credit history hold you back. Upstart's innovative approach could be your path to financial flexibility.

Check Your Upstart Rate in MinutesAlternatives to Upstart and How They Compare

While Upstart offers a unique lending model, it\'s always wise to explore alternatives to ensure you find the best fit for your financial situation. Traditional lenders often have stricter **credit score requirements**, typically looking for borrowers with good to excellent credit (FICO scores above 670). For individuals with **subprime borrower** profiles or those actively engaged in **credit building**Upstart\\'s**non-traditional underwriting** can be a significant advantage. This is where Upstart truly shines, providing opportunities where others might not.

Other lenders might offer different **APR** ranges, **origination fee** structures, or **loan term** options. For instance, some lenders specialize in personal loans for **bad credit personal loans**, while others cater to those with excellent credit seeking the lowest possible **annual percentage rate**. Always compare multiple offers, considering the total cost of the loan, including all fees and interest, before making a decision. Factors like **funding speed** and customer service can also play a role in your choice. It's crucial to understand the nuances of each lender's offerings to make an informed decision that aligns with your financial goals.

Frequently Asked Questions About Upstart Loan Requirements

What are the minimum credit score requirements for an Upstart personal loan?

Upstart is unique because it does not have a minimum FICO score requirement. Instead, it uses **AI underwriting** to evaluate applicants based on **non-traditional credit factors** like education, **employment history**, and income, making it accessible to those with limited credit history or **fair credit**. This innovative approach broadens access to credit for many individuals.

What is the minimum income required for an Upstart loan?

To qualify for an Upstart personal loan, applicants generally need a **minimum income requirement** of $12,000 per year. This income can come from various sources, including full-time employment, part-time work, or other verifiable income streams. Upstart considers your overall financial picture.

Does Upstart consider my education and employment history?

Yes, Upstart\'s **AI underwriting** model heavily considers your education and **employment history**. These **non-traditional credit factors** help Upstart assess your creditworthiness beyond just your FICO score, potentially leading to better approval odds and rates. This is a key differentiator from traditional lenders.

Are there any residency or bank account requirements for Upstart?

Yes, to be eligible for an Upstart personal loan, you must be a **US resident** and have a valid **bank account requirement**. You also need to be at least 18 years old (or 19 in Alabama and Nebraska) and have a valid email address. These are standard requirements for most lenders.

What is the typical APR range for Upstart personal loans?

Upstart personal loans typically have an **APR** range from 6.40% to 35.99%. The actual **annual percentage rate** you receive will depend on your creditworthiness, income, and other factors assessed by Upstart\'s **AI underwriting** model. It's important to compare this with other lenders.

How does Upstart\'s AI underwriting work?

Upstart's **AI underwriting** uses machine learning to analyze thousands of data points beyond just your **FICO score**. This includes your education, job history, and income potential, providing a more comprehensive view of your financial stability and future earning capacity. This allows them to approve more applicants and offer potentially lower rates to those with strong profiles but limited traditional credit. It's a modern approach to lending.Does checking my rate affect my credit score?

No, checking your rate with Upstart involves a **soft credit pull**, which will not impact your **credit score**. A **hard credit inquiry** only occurs if you proceed with the loan application and accept an offer, which may temporarily affect your score. This allows you to explore your options risk-free.

What is an origination fee and how much does Upstart charge?

An **origination fee** is a one-time fee charged by lenders for processing a loan. Upstart's **origination fee** can range from 0% to 12% of the loan amount, and it is typically deducted from your loan proceeds before you receive the funds. The exact fee depends on your credit profile and other factors.

Can I pay off my Upstart loan early?

Yes, Upstart does not charge a **prepayment penalty**. This means you can pay off your loan ahead of schedule without incurring any additional fees, which can save you money on interest over the **loan term**.

Disclaimer: The information provided on this page is for informational purposes only and does not constitute financial advice. Loan approval, interest rates, and terms depend on your individual creditworthiness and the lender\'s policies. Always review the full terms and conditions before accepting any loan offer. WiseIQ strives to provide accurate and up-to-date information, but we recommend consulting with a qualified financial professional for personalized advice.