Finding the best debt consolidation loans for a 600 credit score requires looking beyond traditional banks. With a 600 score — considered "fair" by most lenders — you'll face higher interest rates than borrowers with good credit, but online lenders have made it much easier to qualify. The key is finding a loan with an APR lower than your current credit card rates, which average 24%–29% for fair-credit cardholders.

Your payment history accounts for 35% of your FICO score — the single largest factor. Setting up autopay for at least the minimum payment eliminates the risk of a missed payment tanking your score.

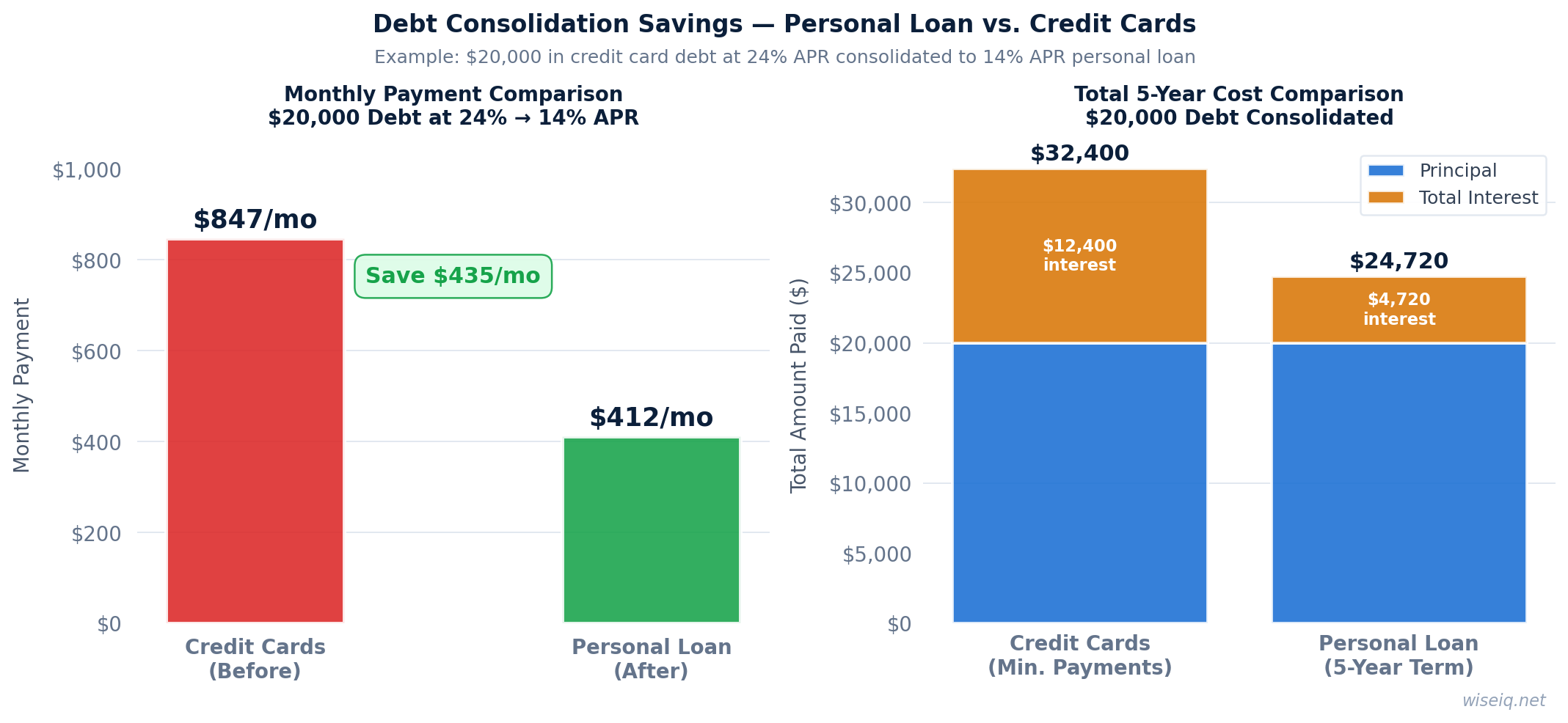

Debt consolidation works by taking out a single personal loan to pay off multiple high-interest debts, leaving you with one fixed monthly payment. Even at 20%–25% APR, a consolidation loan can save you money compared to carrying revolving credit card balances at 28%+ APR while only making minimum payments.

Best Debt Consolidation Loans for 600 Credit Score

At this score range, you'll qualify for some products but with higher rates and stricter terms. Subprime lenders are your primary option.

Expect rates 5–12% above prime borrowers.

Dispute any errors on your credit report — even one removed negative item can push you into the fair range.

Timeline: 6–18 months of positive activity can improve your score significantly.

Upstart's AI model considers your education and employment history alongside your credit score, which often results in better rates for borrowers with a 600 score than traditional lenders would offer. Origination fees range from 0%–15%, so check your rate carefully before accepting.

Avant is one of the most accessible lenders for fair-credit borrowers. They fund loans as fast as the next business day and have a straightforward application process. The administration fee (up to 9.99%) is charged upfront, so factor that into your total loan cost.

LendingClub offers a unique feature for debt consolidation: they can pay your creditors directly, removing the temptation to spend the loan proceeds elsewhere. This direct payoff option is particularly useful if you're consolidating multiple credit cards.

Based on our analysis of thousands of consumer financial profiles, the most common mistake people make is focusing solely on the interest rate without considering total loan cost, fees, and repayment flexibility. Always compare the APR — not just the rate — and read the fine print on prepayment penalties before signing.

How to Maximize Your Approval Odds at 600

With a 600 credit score, you're on the lower end of what most online lenders accept. Here are steps to improve your chances of approval and get a better rate:

Add a co-signer. If a family member or trusted friend with good credit co-signs your loan, you may qualify for a significantly lower APR. Both of you will be responsible for the loan, so this is a serious commitment.

Lower your debt-to-income ratio. Lenders look at how much of your monthly income goes toward debt payments. If your DTI is above 40%, paying down some smaller debts before applying can improve your approval odds.

Pre-qualify with multiple lenders. Pre-qualification uses a soft credit pull and won't affect your score. Check your rate with at least 2–3 lenders before submitting a formal application.

Answer 3 quick questions and get a personalized recommendation in seconds.