Top Personal Loans for 600 Credit Score

At this score range, you'll qualify for some products but with higher rates and stricter terms. Subprime lenders are your primary option.

Before accepting any loan offer, calculate the total cost of the loan (principal + all interest + fees). A lower monthly payment often means paying thousands more over the life of the loan.

Expect rates 5–12% above prime borrowers.

Dispute any errors on your credit report — even one removed negative item can push you into the fair range.

Timeline: 6–18 months of positive activity can improve your score significantly.

AI model considers more than credit score — great for 600-range borrowers.

Same-day or next-day funding. Secured loan option available for lower rates.

Peer-to-peer lending model. Accepts 600+ scores. Joint applications allowed.

Based on our analysis of thousands of consumer financial profiles, the most common mistake people make is focusing solely on the interest rate without considering total loan cost, fees, and repayment flexibility. Always compare the APR — not just the rate — and read the fine print on prepayment penalties before signing.

What to Know About Personal Loans with a 600 Score

Your credit score is one of the most important factors lenders use to determine your interest rate and loan amount. A 600 score (Fair Credit) means you have limited credit history or some negative marks. Understanding where you stand helps you target the right lenders and negotiate better terms.

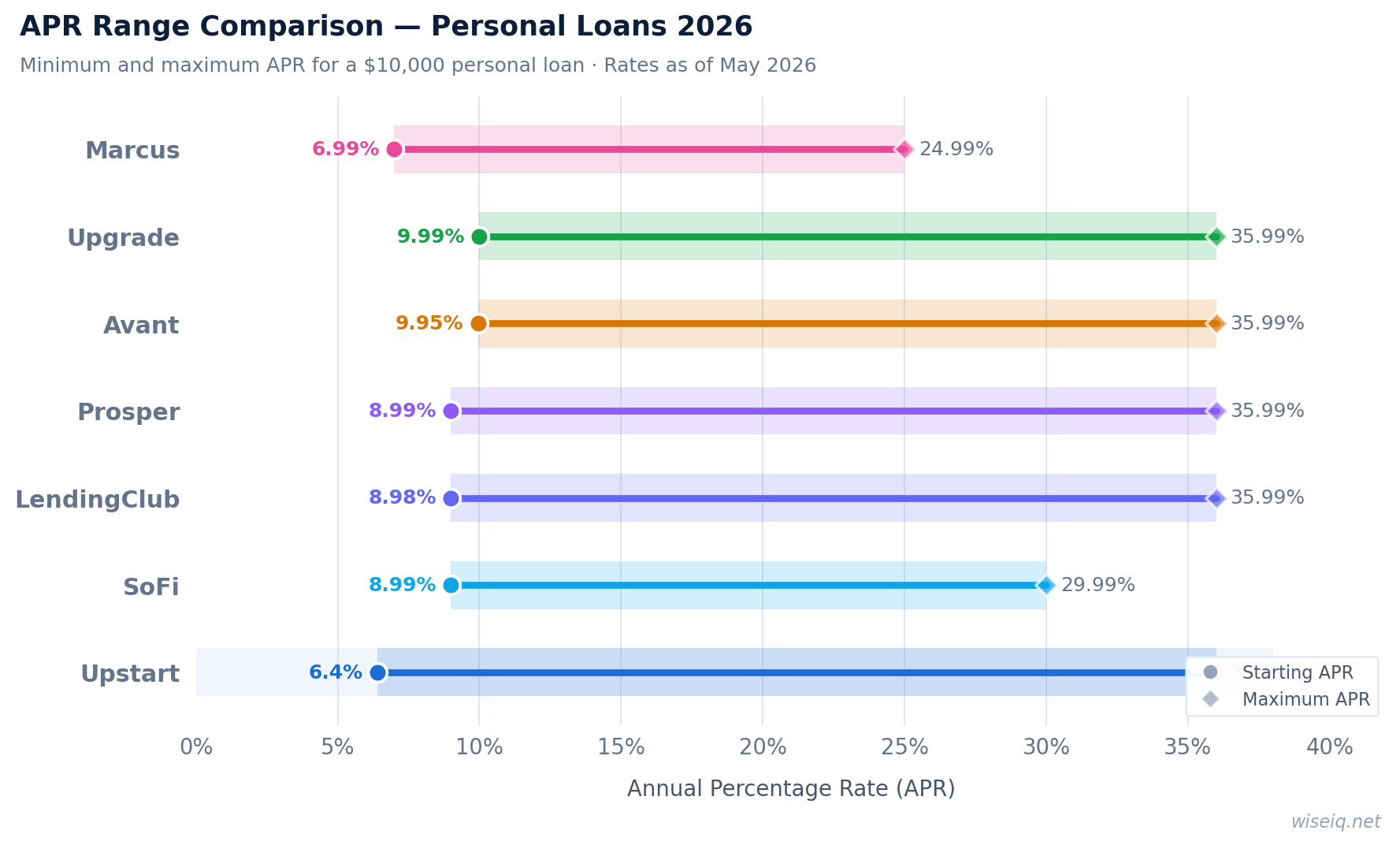

When comparing personal loans, focus on the Annual Percentage Rate (APR) rather than just the interest rate. The APR includes all fees and gives you the true cost of borrowing. Also compare loan amounts, repayment terms, and whether the lender charges origination fees, prepayment penalties, or late fees.

A personal loan is not the right tool for every situation. Consider alternatives if any of the following apply to you:

- You have home equity: A HELOC typically offers rates 5–10% lower than personal loans. If you own your home, compare HELOC rates before taking a personal loan.

- Your debt is primarily credit card debt: A balance transfer card with a 0% intro APR (typically 12–21 months) will cost less than a personal loan if you can pay off the balance within the intro period.

- You need less than $1,000: Most personal loan lenders have minimum amounts of $1,000–$2,000. For smaller needs, a credit union payday alternative loan (PAL) or a 0% APR credit card may be more appropriate.

- Your credit score is below 500: Most personal loan lenders — including those that accept "bad credit" — have practical minimums around 500–560. Below this, secured loans, credit-builder loans, or co-signer arrangements are more realistic options.

- You are in active bankruptcy: Personal loan lenders will decline applicants in active Chapter 7 or Chapter 13 proceedings. Resolve your bankruptcy first.

Answer 3 quick questions and get a personalized recommendation in seconds.

How to Get the Best Rate with a 600 Score

Even with a 600 credit score, there are several strategies to improve your offered rate. First, always pre-qualify with multiple lenders before accepting any offer — this uses a soft credit pull that doesn't affect your score, and comparing offers takes less than 10 minutes. Second, consider the loan term carefully: shorter terms typically come with lower interest rates, though monthly payments will be higher. Third, if you have a trusted family member or friend with excellent credit, adding them as a co-signer can significantly lower your rate.

Reducing your debt-to-income ratio before applying is another powerful lever. Lenders look at how much of your monthly income goes toward debt payments — a ratio below 35% is generally considered favorable. Paying down existing credit card balances before applying can improve both your credit score and your debt-to-income ratio simultaneously.

Find Your Best Personal Loan

Compare rates from top lenders in 2 minutes. No credit impact.

Compare Personal Loan Rates →