Does Debt Consolidation Make Sense at 620?

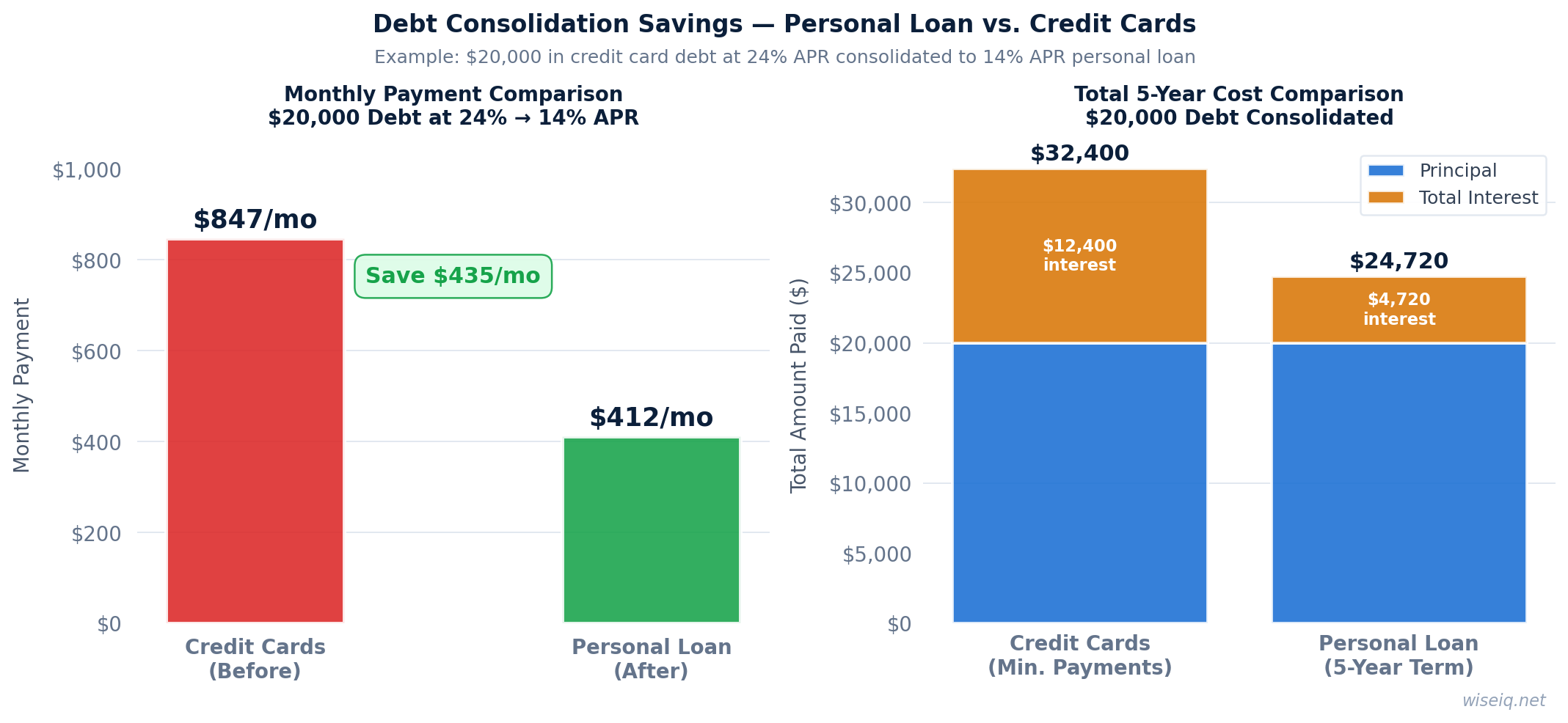

Debt consolidation replaces multiple high-rate debts — typically credit cards charging 20%–29% APR — with a single personal loan at a lower rate. With a 620 credit score, you can realistically qualify for rates between 15% and 28%. If your current credit card rates are above that range, consolidation saves you money even at a higher personal loan rate.

Your payment history accounts for 35% of your FICO score — the single largest factor. Setting up autopay for at least the minimum payment eliminates the risk of a missed payment tanking your score.

The key calculation: if your weighted average credit card APR is 24% and you can get a consolidation loan at 20%, you save 4 percentage points on every dollar of debt. On a $10,000 balance over 3 years, that's roughly $600 in interest savings.

Before you apply: Use our free debt consolidation calculator to see exactly how much you could save based on your current balances and rates.

Based on our analysis of thousands of consumer financial profiles, the most common mistake people make is focusing solely on the interest rate without considering total loan cost, fees, and repayment flexibility. Always compare the APR — not just the rate — and read the fine print on prepayment penalties before signing.

Best Debt Consolidation Lenders for 620 Credit Score

Upstart's AI underwriting model looks beyond your credit score to factors like education and employment history. Borrowers with a 620 score and stable income often qualify for rates well below 30%. Upstart is also one of the fastest lenders — most borrowers receive funds the next business day.

Pros

- Considers income and employment, not just score

- Soft pull pre-qualification

- Fast funding (1 business day)

- Loans up to $50,000

Cons

- Origination fee up to 12%

- Only 3 or 5 year terms

- No joint applications

WiseIQ may earn a commission. This does not affect our editorial ratings.

LendingClub is one of the few major online lenders that allows joint applications. If you have a spouse or family member with better credit, applying together can significantly lower your rate. LendingClub also offers a direct pay feature — they send loan proceeds directly to your creditors, simplifying the consolidation process.

Pros

- Joint applications allowed

- Direct creditor pay option

- Flexible loan terms

- Established peer-to-peer platform

Cons

- Origination fee 3%–8%

- Funding takes 2–4 days

- Higher rates at 620 score

Avant is built specifically for near-prime borrowers and has funded over $8 billion in loans. At a 620 credit score, you're in their sweet spot. Their online application takes about 10 minutes and decisions are typically fast. Avant also offers a mobile app for managing your loan and making payments.

Pros

- Designed for 580–700 credit scores

- Fast online application

- Mobile app included

- No prepayment penalty

Cons

- Administration fee up to 9.99%

- Not available in all states

- Lower maximum loan amount

Prosper is a peer-to-peer lending platform where individual investors fund your loan. Their minimum credit score of 560 makes them accessible for 620-score borrowers, and their maximum loan amount of $50,000 is generous. Prosper also allows joint applications, which can help you qualify for a better rate.

Pros

- Low minimum credit score (560)

- Loans up to $50,000

- Joint applications allowed

- No prepayment penalty

Cons

- Origination fee 1%–9.99%

- Funding can take 3–5 days

- Late fees apply

Answer 3 quick questions and get a personalized recommendation in seconds.

Quick Comparison: Best Debt Consolidation Loans for 620

| Lender | Min. Score | APR Range | Max Loan | Best Feature |

|---|---|---|---|---|

| Upstart | 300 | 7.8%–35.99% | $50,000 | AI underwriting, fast funding |

| LendingClub | 600 | 8.98%–35.99% | $40,000 | Joint applications, direct pay |

| Avant | 580 | 9.95%–35.99% | $35,000 | Built for near-prime borrowers |

| Prosper | 560 | 8.99%–35.99% | $50,000 | Peer-to-peer, joint apps |

How to Qualify for a Debt Consolidation Loan at 620

A 620 credit score is workable, but lenders will scrutinize other factors closely. Here's what matters most:

Debt-to-Income Ratio (DTI)

Your DTI is your total monthly debt payments divided by gross monthly income. Most lenders want DTI below 40–45%. If you're consolidating to lower your monthly payment, your post-consolidation DTI should improve — make sure to show this in your application context.

Income Stability

Lenders want to see consistent income. W-2 employees have an easier time than self-employed borrowers. If you're self-employed, prepare 2 years of tax returns and recent bank statements.

Credit History Length

A longer credit history helps at 620. If you have older accounts, keep them open even if you don't use them — closing old accounts shortens your average account age and can lower your score.

Watch out: Some lenders advertise "debt consolidation" but are actually debt settlement companies. These are very different — settlement damages your credit and takes years. Only use licensed personal loan lenders for true debt consolidation.

Alternatives to a Debt Consolidation Loan

If you can't qualify for a personal loan at an acceptable rate, consider these alternatives:

- Balance transfer credit card: Some cards offer 0% intro APR for 12–21 months. With a 620 score, options are limited, but cards like the Citi Secured or Discover it Secured may be accessible.

- Home equity loan (HELOC): If you own a home, a HELOC can offer much lower rates. See our HELOC guide for details.

- Debt management plan (DMP): A nonprofit credit counseling agency negotiates lower rates with your creditors. No loan required. See our debt relief guide.

- Negotiate directly with creditors: Many credit card issuers will reduce your interest rate if you call and ask, especially if you've been a long-time customer.

Frequently Asked Questions

How much can I consolidate with a 620 credit score?

Most lenders will approve $5,000–$25,000 for borrowers with a 620 credit score, depending on income and existing debt. Upstart and Prosper offer up to $50,000 for qualified borrowers.

Will debt consolidation improve my credit score?

Yes, over time. Consolidation reduces your credit card utilization (a major score factor) and adds an installment loan to your credit mix. Most borrowers see score improvements within 3–6 months of making on-time payments. See our guide: How to Improve Your Credit Score Fast.

What's the difference between debt consolidation and debt settlement?

Debt consolidation combines your debts into a single loan — you pay everything back in full. Debt settlement negotiates to pay less than you owe, which severely damages your credit. See our full comparison guide.

Sources & Methodology

WiseIQ's editorial team researches and fact-checks all content using primary sources. Our recommendations are based on independent analysis and are not influenced by advertiser relationships.

- Consumer Financial Protection Bureau (CFPB) — regulatory data and consumer guidance

- Federal Reserve — Consumer Credit Report (G.19) — interest rate benchmarks

- AnnualCreditReport.com — official free credit report access

- myFICO Credit Education — credit score methodology

- Lender and issuer websites — rates, terms, and eligibility verified directly from source

Last reviewed: April 2026 | How we rank products