If you've been searching for ways to manage multiple debts, you've probably seen both "personal loan" and "debt consolidation" come up repeatedly. Many people assume they're the same thing — and in some contexts they are — but there's an important distinction. Understanding the difference will help you choose the right product for your financial situation.

Before accepting any loan offer, calculate the total cost of the loan (principal + all interest + fees). A lower monthly payment often means paying thousands more over the life of the loan.

What Is a Personal Loan?

A personal loan is an unsecured installment loan — you borrow a fixed amount, receive it as a lump sum, and repay it in fixed monthly payments over a set term (typically 2–7 years). Personal loans can be used for almost anything: home improvement, medical bills, vacations, or paying off other debts. The interest rate is fixed, so your payment never changes.

Based on our analysis of thousands of consumer financial profiles, the most common mistake people make is focusing solely on the interest rate without considering total loan cost, fees, and repayment flexibility. Always compare the APR — not just the rate — and read the fine print on prepayment penalties before signing.

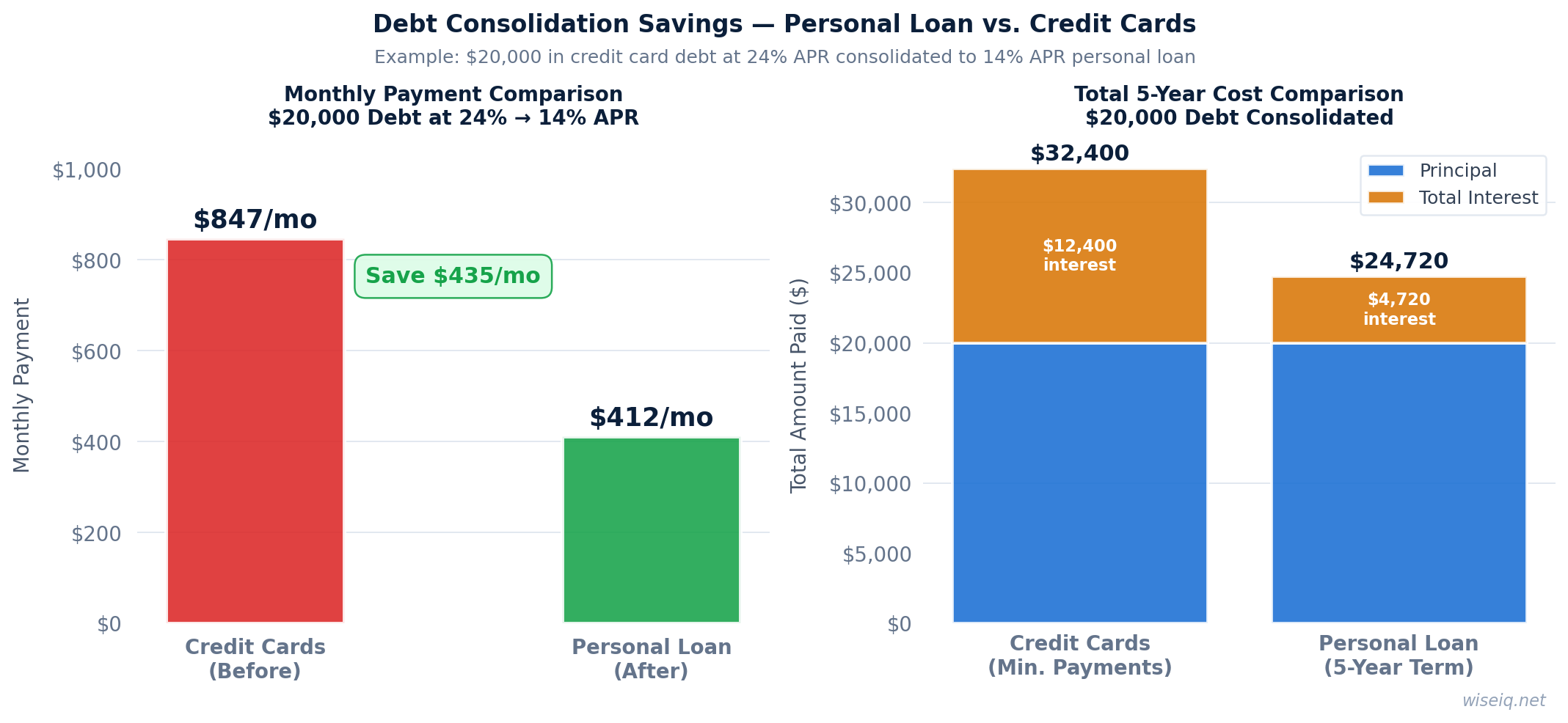

What Is Debt Consolidation?

Debt consolidation is the act of combining multiple debts into a single payment, ideally at a lower interest rate. The goal is to simplify your finances and reduce the total interest you pay. Debt consolidation can be accomplished through several different financial products:

- Personal loan — borrow a lump sum to pay off multiple debts

- Balance transfer credit card — move credit card balances to a 0% intro APR card

- Home equity loan or HELOC — use home equity to pay off unsecured debts

- Debt management plan (DMP) — nonprofit agency negotiates lower rates with creditors

A personal loan is not the right tool for every situation. Consider alternatives if any of the following apply to you:

- You have home equity: A HELOC typically offers rates 5–10% lower than personal loans. If you own your home, compare HELOC rates before taking a personal loan.

- Your debt is primarily credit card debt: A balance transfer card with a 0% intro APR (typically 12–21 months) will cost less than a personal loan if you can pay off the balance within the intro period.

- You need less than $1,000: Most personal loan lenders have minimum amounts of $1,000–$2,000. For smaller needs, a credit union payday alternative loan (PAL) or a 0% APR credit card may be more appropriate.

- Your credit score is below 500: Most personal loan lenders — including those that accept "bad credit" — have practical minimums around 500–560. Below this, secured loans, credit-builder loans, or co-signer arrangements are more realistic options.

- You are in active bankruptcy: Personal loan lenders will decline applicants in active Chapter 7 or Chapter 13 proceedings. Resolve your bankruptcy first.

Answer 3 quick questions and get a personalized recommendation in seconds.

Personal Loan vs Debt Consolidation: Key Differences

| Factor | Personal Loan | Debt Consolidation (General) |

|---|---|---|

| What it is | A specific loan product | A financial strategy |

| How it works | Lump sum, fixed payments | Varies by method used |

| Credit requirement | Varies by lender (300–660+) | Varies by method (DMPs have no minimum) |

| Typical APR | 6.2%–35.99% | 0%–25%+ depending on method |

| Best for | Borrowers who qualify for a loan | Anyone with multiple high-interest debts |

| Collateral required | Usually no (unsecured) | Depends on method |

When a Personal Loan Is the Right Choice

Using a personal loan for debt consolidation makes the most sense when you have a credit score of 580 or higher and can qualify for an APR lower than your current credit card rates. If you're carrying $10,000 in credit card debt at 26% APR, a personal loan at 18% APR would save you significant money over the repayment period, even after accounting for any origination fees.

Upstart is one of the most accessible personal loan lenders for debt consolidation, accepting borrowers with scores as low as 300. Their AI underwriting considers your full financial picture, not just your credit score.

When a Different Consolidation Method Is Better

Balance transfer card: If you have good credit (660+) and can pay off the balance within the 0% intro period (typically 12–21 months), a balance transfer card is often the cheapest consolidation option — you pay zero interest during the promo period.

Debt management plan: If your credit score is below 580 and you can't qualify for a personal loan at a reasonable rate, a nonprofit DMP can reduce your credit card interest rates to 6%–10% without requiring a credit check.

Home equity loan: If you own a home with equity, a home equity loan typically offers the lowest rates (often 7%–10%) but puts your home at risk if you default. Only consider this option if you're confident in your ability to repay.