Both personal loans and credit cards let you borrow money, but they work very differently. The right choice depends on what you are financing, how much you need, and how quickly you can repay. This guide breaks down the key differences and tells you exactly when to choose each option.

Always pay your statement balance in full each month — not just the minimum. Carrying a balance costs the average American over $1,200 per year in interest charges.

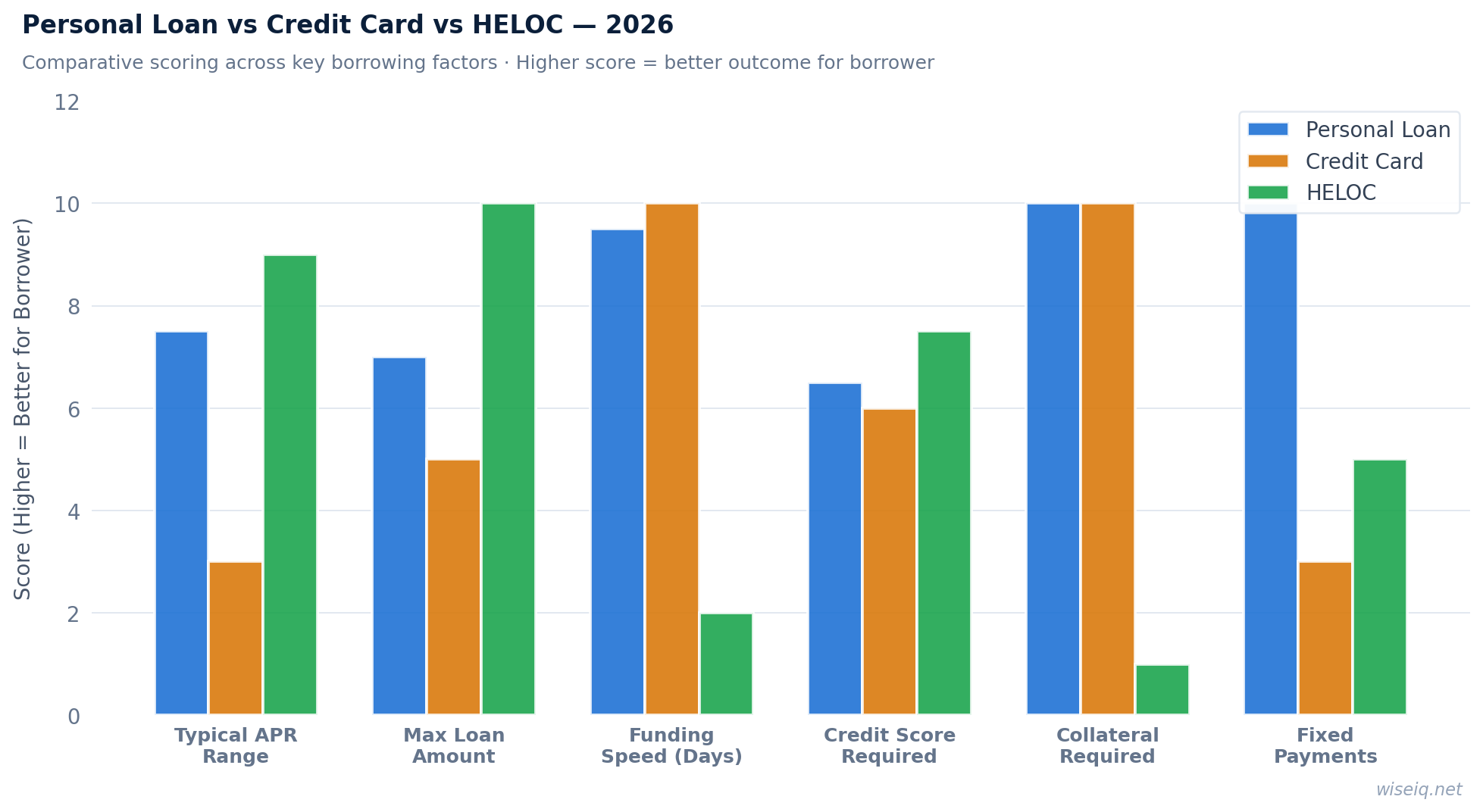

How They Differ

A personal loan is a lump-sum installment loan — you borrow a fixed amount at a fixed APR and repay it in equal monthly payments over a set term (typically 2–7 years). A credit card is a revolving line of credit — you can borrow up to your limit, repay it, and borrow again. You only pay interest on your outstanding balance.

Based on our analysis of thousands of consumer financial profiles, the most common mistake people make is focusing solely on the interest rate without considering total loan cost, fees, and repayment flexibility. Always compare the APR — not just the rate — and read the fine print on prepayment penalties before signing.

Interest Rates: Personal Loans Usually Win

The average credit card APR in 2026 is approximately 21–24%. The average personal loan APR for borrowers with good credit is 10–14%. For large balances or long repayment timelines, a personal loan will almost always cost less in total interest. The exception: 0% APR credit card promotions, which beat personal loans for the promotional period (typically 12–21 months).

A personal loan is not the right tool for every situation. Consider alternatives if any of the following apply to you:

- You have home equity: A HELOC typically offers rates 5–10% lower than personal loans. If you own your home, compare HELOC rates before taking a personal loan.

- Your debt is primarily credit card debt: A balance transfer card with a 0% intro APR (typically 12–21 months) will cost less than a personal loan if you can pay off the balance within the intro period.

- You need less than $1,000: Most personal loan lenders have minimum amounts of $1,000–$2,000. For smaller needs, a credit union payday alternative loan (PAL) or a 0% APR credit card may be more appropriate.

- Your credit score is below 500: Most personal loan lenders — including those that accept "bad credit" — have practical minimums around 500–560. Below this, secured loans, credit-builder loans, or co-signer arrangements are more realistic options.

- You are in active bankruptcy: Personal loan lenders will decline applicants in active Chapter 7 or Chapter 13 proceedings. Resolve your bankruptcy first.

Answer 3 quick questions and get a personalized recommendation in seconds.

When to Choose a Personal Loan

Choose a personal loan when: you need more than $5,000, you need more than 18 months to repay, you want a fixed monthly payment for budgeting purposes, or you are consolidating existing high-interest debt. Personal loans are also better for large one-time expenses like home improvements, medical bills, or major purchases.

When to Choose a Credit Card

Choose a credit card when: you qualify for a 0% APR promotional offer and can pay off the balance before it expires, you need a small amount (under $3,000) that you can repay quickly, you want purchase protection or rewards on the transaction, or you need flexible access to funds over time rather than a lump sum.

Best option when you need to consolidate credit card debt or finance a large expense. AI-powered approval considers more than your credit score. Typical APR 6.2%–35.99%, subject to change.

Side-by-Side Comparison

| Factor | Personal Loan | Credit Card |

|---|---|---|

| Avg APR | 10%–36% | 21%–29% |

| Best APR available | 6.2% | 0% (promotional) |

| Repayment | Fixed monthly payments | Flexible minimum payments |

| Loan amount | $1K–$100K | Up to credit limit |

| Best for | Large expenses, consolidation | Small purchases, rewards |

| Winner for large balances | Personal Loan | |

Find Your Best Rate in 2 Minutes

Answer 5 quick questions and see personalized loan offers matched to your credit profile — no credit pull required.

Check My Options →Frequently Asked Questions

Is a personal loan better than a credit card for debt consolidation?

Yes, in almost all cases. Personal loan APRs average 10–14% for good credit borrowers, compared to 21–24% for credit cards. On $10,000 in debt, the difference is $700–$1,400 per year in interest savings.

Does taking out a personal loan hurt your credit score?

A personal loan application causes a temporary 2–5 point dip from the hard inquiry. However, paying off credit card balances with the loan reduces your utilization ratio, which can improve your score by 20–50 points.

Can I use a personal loan to pay off credit cards?

Yes. This is called debt consolidation. You take out a personal loan at a lower APR than your credit cards and use the proceeds to pay them off. You then make a single monthly payment on the personal loan.

What is the minimum credit score for a personal loan?

Upstart accepts scores as low as 300. Most lenders require 580–640. For the best rates (under 10% APR), you typically need a score of 720 or higher.