When considering a personal loan, understanding all associated costs is crucial. The Upstart origination fee is one such cost that can significantly impact the total amount you repay. This comprehensive guide from WiseIQ will break down what an origination fee is, how Upstart applies it, and practical strategies to help you minimize this upfront fee, ensuring you get the most out of your loan proceeds. We\'ll also explore how this fee affects your overall Annual Percentage Rate (APR) and what you need to know about Upstart\'s unique AI underwriting model.

Expert Tip: Always factor the origination fee into your total loan cost. It\'s not just about the interest rate; the upfront fee can make a big difference in your disbursement amount and overall repayment. Use the APR, which includes all fees, for the most accurate comparison.

Understanding the Upstart Origination Fee: A Deeper Dive

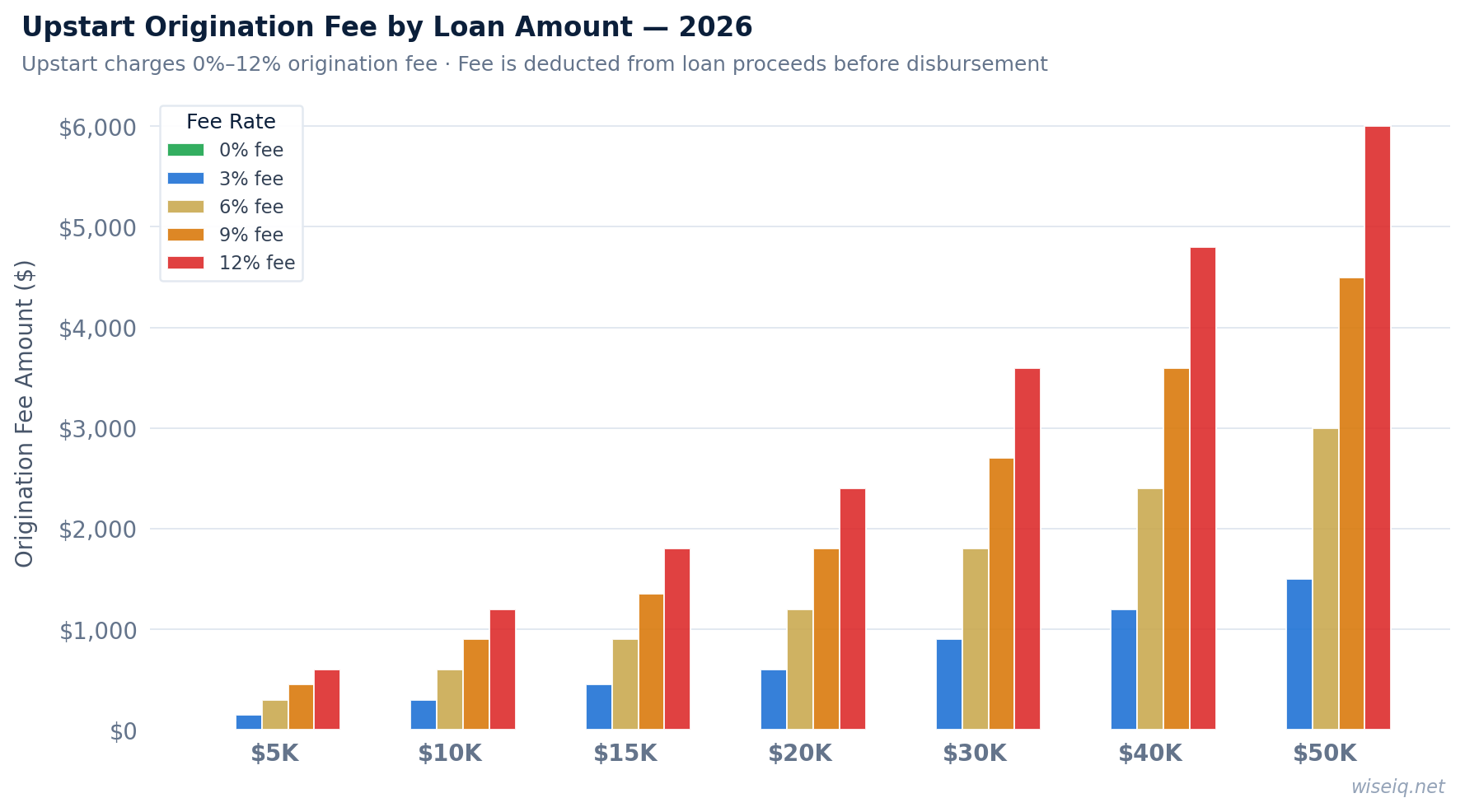

An origination fee is a standard charge in the lending industry, essentially a processing fee for setting up your loan. For Upstart personal loans, this fee can range from 0% to 12% of the total loan amount. Unlike some lenders, Upstart deducts this fee directly from your loan proceeds before the funds are disbursed to you. This means if you\'re approved for a $10,000 loan with a 5% origination fee, you would receive $9,500, with $500 going towards the fee. This upfront fee covers the administrative costs associated with loan processing, including credit checks, application review, and account setup. It\'s important to recognize that this fee is a one-time charge, but its impact reverberates throughout the life of your loan by reducing the actual amount of money you receive.

Upstart\'s approach to lending is unique due to its reliance on AI underwriting. Instead of solely focusing on traditional metrics like FICO score, Upstart considers non-traditional credit factors such as education-based lending and employment history. This innovative model allows them to approve a broader range of borrowers, including those with a fair credit or limited credit history. However, the origination fee percentage you receive is a direct reflection of the risk assessment performed by their AI, with higher-risk borrowers typically facing higher fees. This sophisticated system analyzes thousands of data points to determine your creditworthiness, which directly influences the loan fee and ultimately, your overall loan cost. Understanding this AI-driven process can help you prepare a stronger application.

The fee is not arbitrary; it\'s a reflection of the lender\'s assessment of the risk involved in lending to you. A higher risk profile, as determined by Upstart\'s algorithms, often translates to a higher origination fee. This is why improving your financial standing and presenting a comprehensive picture of your creditworthiness can be beneficial. Factors like a stable employment history, a strong educational background, and a manageable debt-to-income ratio can all contribute to a more favorable assessment and potentially a lower origination fee.

How Upstart\'s Origination Fee Impacts Your Loan and Total Cost

The impact of an Upstart origination fee extends beyond just the initial deduction from your loan. It plays a crucial role in determining your effective Annual Percentage Rate (APR). The APR is a more comprehensive measure of the cost of borrowing, as it includes both the interest rate and any additional fees, such as the origination fee. When comparing loan offers, it\'s vital to look at the APR rather than just the interest rate to understand the true total loan cost. A common misconception is to only focus on the interest rate, but neglecting the origination fee can lead to an underestimation of the loan\'s true expense.

For example, a loan with a lower interest rate but a high origination fee might end up being more expensive than a loan with a slightly higher interest rate but no origination fee. This is why understanding the fee calculation is so important. The net loan proceeds you receive will be less than the approved loan amount, which can affect your ability to meet your financial needs, especially if you have a specific disbursement amount in mind for debt consolidation or a major purchase. Upstart is known for its no prepayment penalty policy, which is a significant benefit, allowing you to save on interest if you pay off your loan early. However, the upfront fee remains a key consideration, as it\'s paid regardless of how quickly you repay the loan. This means that even if you plan to pay off your loan ahead of schedule, the origination fee will still be a part of your initial cost.

Consider a scenario where you need exactly $10,000 for a project. If your approved Upstart loan has a 5% origination fee, you would need to apply for a loan of approximately $10,526 to receive the full $10,000 after the fee is deducted ($10,526 * 0.05 = $526.30 fee; $10,526 - $526.30 = $9,999.70). This adjustment is critical for accurate financial planning and ensuring you have the necessary funds. Always calculate your required loan amount with the origination fee in mind to avoid shortfalls.

Strategies to Minimize Your Upstart Origination Fee

While an origination fee is often unavoidable, there are several strategies you can employ to potentially reduce the amount you pay or improve your chances of securing a lower fee:

- Improve Your Credit Profile: Although Upstart uses AI underwriting, a good FICO score and a healthy credit history can still positively influence your loan terms, potentially leading to a lower origination fee. Focus on paying bills on time, reducing your debt-to-income ratio, and correcting any errors on your credit report. A strong credit profile signals lower risk to lenders, including Upstart\'s AI model.

- Demonstrate Stable Employment and Education: Upstart values education-based lending and stable employment history. Highlighting these aspects in your application can signal lower risk to their AI model. Providing a consistent work history and details about your educational achievements can significantly improve your loan offer.

- Compare Offers: Always prequalify with multiple lenders. Upstart offers a soft credit pull for prequalification, which won\'t affect your credit score. This allows you to compare their offer, including the origination fee and APR, with other lenders to find the best deal. Don\'t settle for the first offer; shopping around can save you a substantial amount.

- Consider Loan Amount: Sometimes, adjusting your requested loan amount slightly can impact the fee structure. While not always the case, it\'s worth exploring if you have flexibility. Borrowing only what you need can also help reduce the overall cost, as the fee is a percentage of the loan amount.

- Understand the Fee Range: Upstart\'s origination fee can be 0%–12%. Aiming for the lower end of this range means you\'re seen as a less risky borrower. Work towards improving factors that influence this assessment before applying.

- Review Your Application Carefully: Ensure all information provided in your application is accurate and complete. Any discrepancies could lead to a less favorable assessment and a higher fee.

Upstart Loan Details: Rates and Fees at a Glance

To give you a clear picture, here\'s a summary of key statistics related to Upstart personal loans, including the origination fee and APR range. These figures are crucial for understanding the potential total loan cost and making an informed decision about your borrowing needs.

| Feature | Details |

|---|---|

| Origination Fee | 0%–12% of loan amount |

| APR Range | 6.40%–35.99% |

| Loan Amounts | $1,000 to $50,000 |

| Loan Terms | 3 or 5 years |

| Prepayment Penalty | None |

| Funding Speed | As fast as one business day |

Rates verified May 2026.

It\'s important to note that the APR (Annual Percentage Rate) is a key metric that combines the interest rate with the origination fee and any other charges. This gives you the true annual cost of your loan. Upstart\'s APR range of 6.40%–35.99% reflects the diverse risk profiles they serve through their AI underwriting. Your specific rate will depend on your individual financial situation, including your debt-to-income ratio, employment history, educational background, and other non-traditional credit factors. Always consider the full APR when comparing loan offers, as it provides the most accurate representation of the total cost of borrowing.

Check Your Upstart Rate Now!Comparing APR vs. Interest Rate with Upstart: Why the Distinction Matters

Many borrowers confuse APR with the interest rate, but understanding the distinction is vital, especially when an origination fee is involved. The interest rate is simply the cost of borrowing money, expressed as a percentage of the principal. It\'s the percentage you pay on the outstanding loan balance. The APR, or Annual Percentage Rate, provides a more holistic view of the total loan cost over the life of the loan. It includes the interest rate plus any additional fees, such as the Upstart origination fee, and is expressed as an annual percentage. This makes the APR a more accurate tool for comparing the true cost of different loan products.

For instance, if you secure an Upstart loan with a 10% interest rate and a 5% origination fee, your APR will be higher than 10%. This is because the origination fee is essentially an additional cost of borrowing that is spread out over the loan term. Upstart\'s transparency in providing both the interest rate and the APR allows borrowers to make informed decisions. Always prioritize comparing APRs across different lenders to get an accurate sense of which loan offers the best value. This is particularly important for personal loans where upfront fees can vary significantly. Focusing solely on the interest rate can be misleading, as a seemingly low interest rate could be offset by a high origination fee, making the overall loan more expensive.

The difference between APR and interest rate becomes even more critical when considering the total loan cost. While the interest rate dictates your monthly payment\'s interest portion, the APR gives you the complete financial picture, including all mandatory charges. This comprehensive view is essential for budgeting and ensuring that the loan aligns with your financial goals. Upstart, with its clear disclosure of both, empowers borrowers to make well-informed choices, emphasizing the importance of understanding every component of your loan\'s cost.

Related Guides to Upstart Personal Loans: Expand Your Knowledge

Explore more about Upstart and personal loans with our in-depth guides. These resources will help you navigate various aspects of personal lending and make the best financial decisions for your situation:

About the WiseIQ Editorial Team

Our team of financial experts at WiseIQ is dedicated to providing unbiased, accurate, and actionable advice to help you make informed financial decisions. We meticulously research and review every aspect of personal finance to empower our readers to achieve their financial goals. Our content is regularly updated to reflect the latest market trends and lending practices.

Frequently Asked Questions About Upstart Origination Fees

What is an Upstart origination fee?

An Upstart origination fee is a one-time charge deducted from your loan proceeds to cover the administrative costs of processing your loan. This fee can range from 0% to 12% of the total loan amount, depending on your creditworthiness and other factors assessed by Upstart\'s AI underwriting model. It\'s a common practice among lenders to cover the costs associated with loan approval and disbursement.

How is the Upstart origination fee calculated?

The origination fee calculation for an Upstart loan is based on several factors, including your credit score, education, employment history, and other non-traditional credit factors. Upstart\'s AI underwriting system assesses your risk profile to determine the exact percentage, which is then applied to your approved loan amount. This personalized assessment means the fee can vary significantly from one borrower to another.

Can I avoid paying the Upstart origination fee?

While it\'s not always possible to completely avoid an origination fee, you can minimize it by improving your credit profile, demonstrating a stable employment history, and having a low debt-to-income ratio. Some lenders offer 0% origination fees to highly qualified borrowers, so it\'s worth striving for the best possible financial standing before applying. A strong application can lead to more favorable terms.

Does the origination fee affect my APR?

Yes, the origination fee directly impacts your Annual Percentage Rate (APR). The APR represents the total cost of borrowing, including both the interest rate and any upfront fees like the origination fee. A higher origination fee will result in a higher APR, even if the stated interest rate remains the same. This is why comparing APRs is crucial for understanding the true cost of a loan.

How does Upstart\'s origination fee compare to other lenders?

Upstart\'s origination fee range of 0%–12% is comparable to many other personal loan lenders. Some lenders charge a flat fee, while others have a similar percentage-based structure. It\'s crucial to compare the total loan cost, including all fees and the APR, across multiple lenders to find the best deal. Always look beyond just the advertised interest rate.

What are \"net loan proceeds\" and \"disbursement amount\"?

The \"net loan proceeds\" refer to the actual amount of money you receive after any upfront fees, such as the origination fee, have been deducted from the total approved loan amount. The \"disbursement amount\" is synonymous with net loan proceeds; it\'s the sum that is actually sent to your bank account or creditors. Understanding this distinction is crucial for budgeting and ensuring you receive enough funds for your intended purpose, as the amount you apply for might not be the exact amount you receive.

Are there any other upfront fees besides the origination fee?

While the origination fee is the most common upfront fee for personal loans, some lenders might charge application fees or other administrative charges. Upstart primarily focuses on the origination fee. Always review your loan agreement carefully to identify all potential fees before finalizing your loan. WiseIQ recommends looking at the total loan cost to avoid surprises and ensure full transparency.

Does a soft credit pull affect my credit score?

No, a soft credit pull, which Upstart uses for prequalification, does not affect your credit score. It allows lenders to review your creditworthiness without leaving a hard inquiry on your credit report. A hard credit inquiry, which occurs when you formally apply for a loan, can temporarily lower your score by a few points. This makes prequalification a risk-free way to check your potential rates.

What is the typical loan term for Upstart personal loans?

Upstart typically offers personal loan terms of either three or five years. The loan term, along with your interest rate and origination fee, will determine your monthly payment. Choosing a shorter loan term usually means higher monthly payments but less interest paid overall, while a longer term offers lower monthly payments but increases the total interest cost. Consider your budget and financial goals when selecting a loan term.

What if I have a bad credit score?

Upstart is known for its AI underwriting model that considers more than just your FICO score, making it a potential option for borrowers with fair credit or even those with a limited credit history. They look at education, employment history, and other non-traditional credit factors. While a bad credit score might result in a higher APR and origination fee, it doesn\'t automatically disqualify you. Explore our guide on Personal Loans for Bad Credit for more options and strategies to improve your chances of approval.

How quickly can I get funds from an Upstart loan?

Upstart is known for its fast funding speed. Once your loan is approved and you accept the offer, funds can be disbursed as fast as one business day. This quick turnaround makes Upstart an attractive option for those who need access to funds urgently, whether for unexpected expenses or time-sensitive projects. However, the exact timing can depend on your bank\'s processing times.

Is there a prepayment penalty with Upstart?

No, Upstart does not charge any prepayment penalties. This means you can pay off your loan early without incurring additional fees, which can save you a significant amount in interest over the life of the loan. This flexibility is a major benefit for borrowers who anticipate being able to repay their loan ahead of schedule.

Disclaimer: The information provided on WiseIQ is for educational purposes only and should not be considered financial advice. Always consult with a qualified financial professional before making any financial decisions. Loan terms and availability are subject to change, and individual results may vary based on creditworthiness and other factors.