Understanding Upstart prequalification is the first step toward securing a personal loan that fits your financial needs. Unlike traditional lenders who rely heavily on your FICO score, Upstart utilizes an innovative AI underwriting model that considers a broader range of factors, including your education and employment history. This approach can open doors for borrowers with limited credit history or those who might not qualify for conventional loans. The best part? Checking your rate through Upstart's prequalification process involves only a soft credit pull, meaning there's no hard inquiry on your credit report and absolutely no credit score impact. This allows you to confidently explore your potential loan options and see personalized rates without any risk to your credit standing.

Expert Tip: Maximize Your Upstart Prequalification

To get the most accurate prequalification offers from Upstart, ensure all information provided is current and complete. While Upstart considers non-traditional credit factors, a strong employment history and a clear understanding of your debt-to-income ratio can significantly improve your chances of receiving favorable terms. Remember, prequalification is not a guarantee of approval, but it provides a clear snapshot of what you might qualify for.

How Upstart Prequalification Works

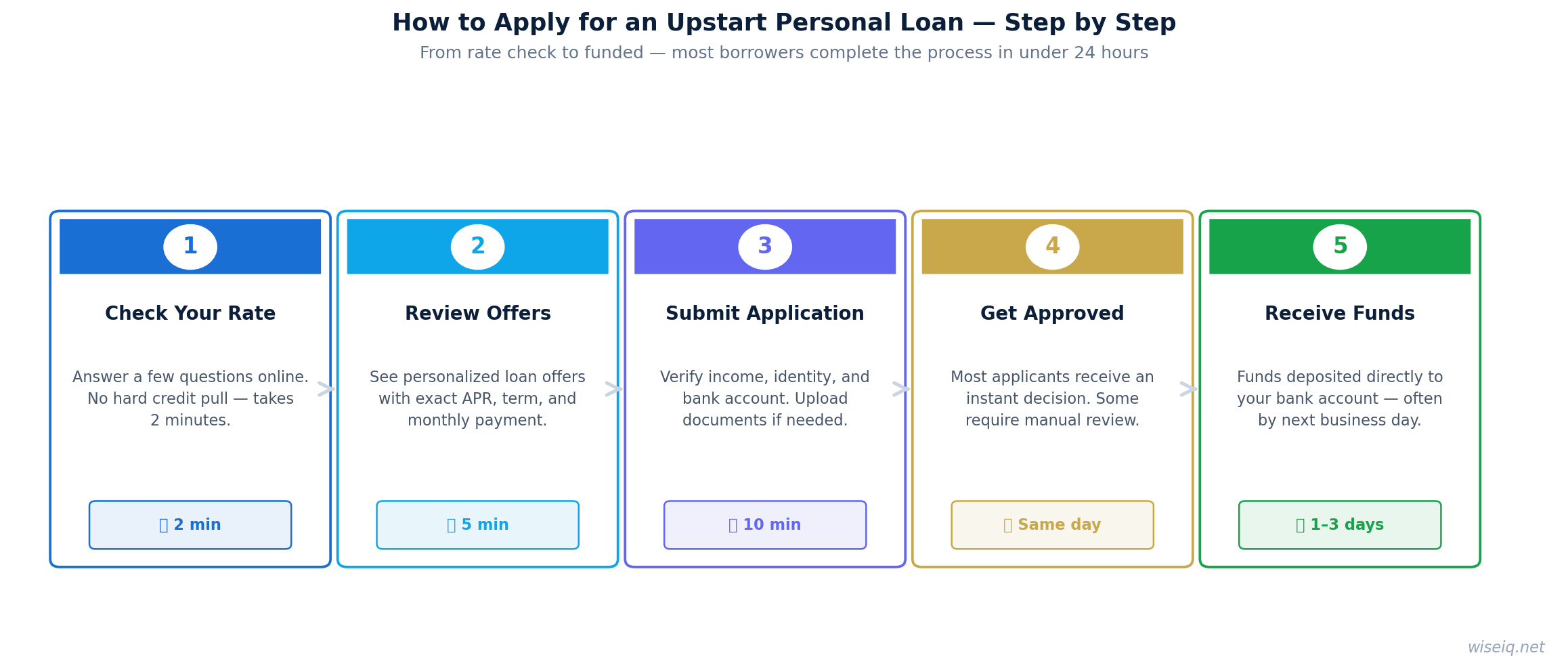

The Upstart prequalification process is designed for speed and transparency, allowing you to quickly understand your loan options. It typically takes just a few minutes to complete and provides you with personalized rates without affecting your credit score. Here's a step-by-step breakdown:

Step 1: Provide Basic Information

You'll start by entering some fundamental details about yourself, including your name, address, income, and educational background. Upstart's AI underwriting model uses this information to build a comprehensive profile.

Step 2: Soft Credit Pull

Upstart performs a soft credit pull to access your credit report. This is a crucial distinction from a hard credit inquiry, as it does not negatively impact your credit score. This allows you to check your rate risk-free.

Step 3: Receive Personalized Offers

Based on your provided information and the soft credit pull, Upstart's AI quickly analyzes your profile and presents you with personalized loan offers, including potential APR (Annual Percentage Rate) and loan term options.

Step 4: Review and Decide

You can then review these offers and decide if you want to proceed with a formal application. If you choose to apply, a hard credit inquiry will be made, which may temporarily affect your credit score.

Prequalification vs. Application: What's the Difference?

It's essential to understand the distinction between prequalification and a full loan application. Prequalification is a preliminary step that gives you an idea of what loan terms you might qualify for without any commitment or impact on your credit score. It's like getting a sneak peek at your options. A full application, on the other hand, is a formal request for a loan. When you submit a full application, the lender will perform a hard credit inquiry, which can cause a slight, temporary dip in your credit score. This inquiry is a necessary part of the final approval process, as it allows the lender to verify all your financial details and make a definitive lending decision. Upstart's transparent process ensures you know exactly when a hard inquiry will occur.

Why Choose Upstart for Your Personal Loan?

Upstart stands out in the personal loan market due to its innovative approach to lending. Here are some key benefits:

- AI Underwriting: Upstart's advanced artificial intelligence model looks beyond just your credit score, considering factors like education, area of study, and job history. This can be particularly beneficial for younger borrowers or those with a limited credit file.

- Education-Based Lending: Your academic achievements and potential earning capacity play a role in Upstart's assessment, offering a unique advantage for graduates.

- Non-Traditional Credit Factors: By evaluating more than just your FICO score, Upstart provides opportunities for a wider range of borrowers who might be overlooked by traditional lenders.

- Fast Prequalification: Get personalized rates in just minutes with a soft credit pull, ensuring no credit score impact.

- Competitive APRs: Upstart offers a competitive APR range from 6.40% to 35.99%, depending on your creditworthiness and other factors.

- No Prepayment Penalty: You can pay off your loan early without incurring any additional fees, saving you money on interest.

- Next-Day Funding: Many borrowers report receiving their funds as soon as the next business day after final approval, making it a great option for urgent financial needs.

- Transparent Fees: While Upstart does charge an origination fee (0%–12%), it's clearly disclosed upfront, and there are no hidden costs.

Upstart Loan Statistics and Examples

To give you a clearer picture of what to expect, here's a look at some typical Upstart loan statistics and a hypothetical payment example. Remember that your actual rates and terms will depend on your individual financial profile.

Rate-Verified Data Table: Upstart Personal Loan Overview

| Feature | Details |

|---|---|

| Loan Amounts | $1,000 - $50,000 |

| APR Range | 6.40% - 35.99% |

| Loan Terms | 3 or 5 years |

| Origination Fee | 0% - 12% |

| Prequalification | Soft credit pull (no credit score impact) |

| Funding Time | As fast as 1 business day |

| Minimum FICO Score | No minimum FICO score (alternative data considered) |

Hypothetical Loan Payment Example

Let's consider a hypothetical scenario to illustrate potential monthly payments:

| Loan Amount | APR | Loan Term | Estimated Monthly Payment | Total Interest Paid |

|---|---|---|---|---|

| $10,000 | 15% | 3 years | $346.65 | $2,479.40 |

| $10,000 | 15% | 5 years | $237.90 | $4,274.00 |

This example is for illustrative purposes only. Your actual rates and payments may vary based on your creditworthiness, loan amount, and loan term.

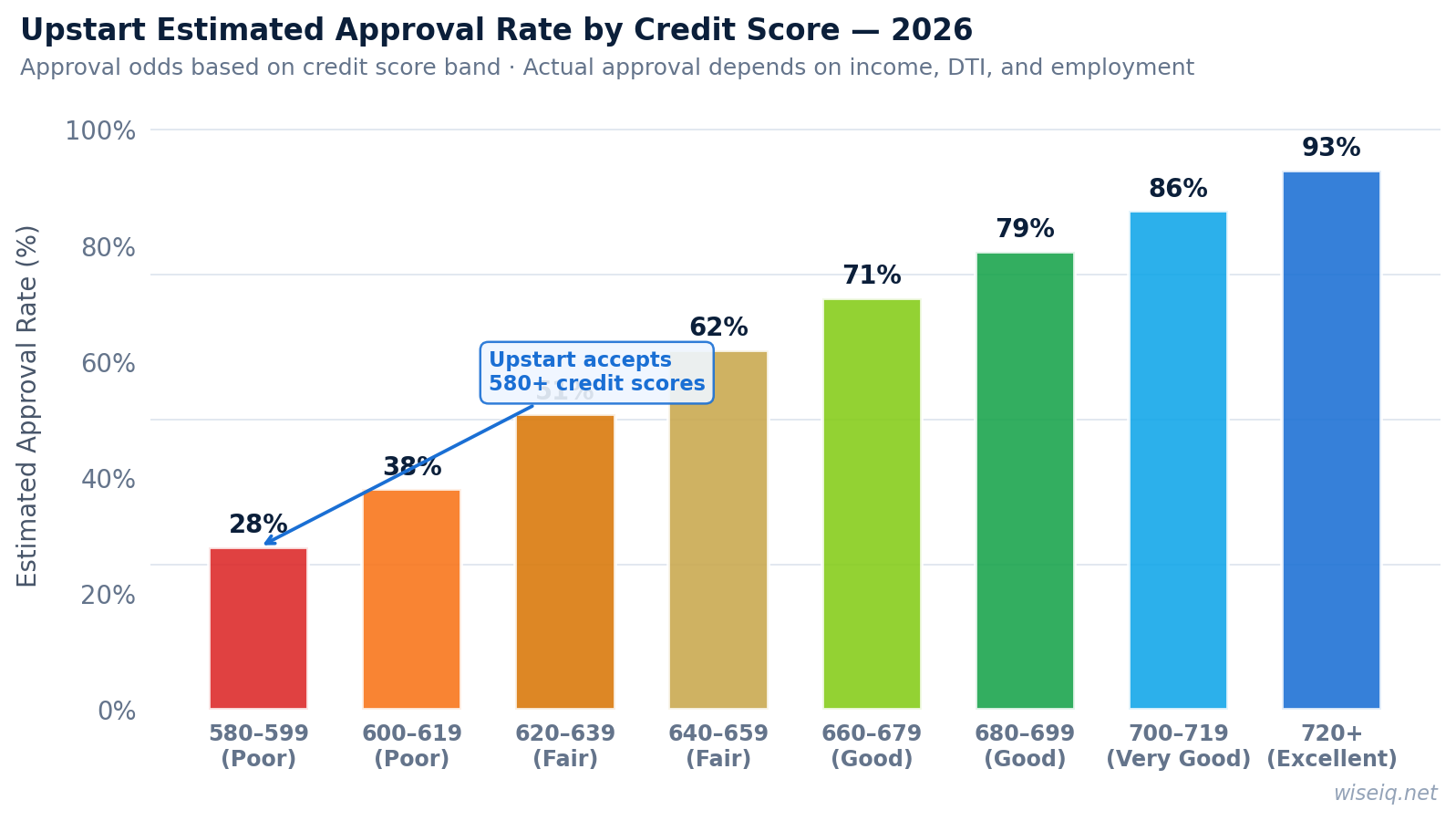

Upstart Prequalification Requirements and Eligibility

While Upstart considers a broader range of factors than traditional lenders, there are still some basic eligibility requirements you'll need to meet to qualify for a personal loan. Understanding these can help you prepare for the prequalification and application process.

- Age: You must be at least 18 years old (19 in Alabama and Nebraska).

- Residency: You must be a U.S. citizen or permanent resident, or a non-permanent resident with a valid U.S. visa.

- Bank Account: You must have a valid U.S. bank account.

- Email Address: A verifiable email address is required.

- Minimum Income: While there isn't a strict minimum income, you must have a verifiable source of income.

- Debt-to-Income Ratio: Your debt-to-income ratio (DTI) will be assessed. A lower DTI generally indicates a healthier financial situation and can improve your chances of approval.

- Education and Employment: Upstart places significant emphasis on your educational background and employment history, especially if you have a limited credit file.

- No Recent Bankruptcies: You generally cannot have any bankruptcies or public records on your credit report.

It's important to note that meeting these requirements does not guarantee approval, but it makes you eligible to apply. Upstart's AI model will evaluate all aspects of your financial profile to make a lending decision.

Alternatives to Upstart Prequalification

While Upstart offers a unique and accessible prequalification process, it's always wise to explore alternatives to ensure you're getting the best possible terms for your personal loan. Different lenders cater to different borrower profiles, and what works best for one person might not be ideal for another. Here are some common alternatives and considerations:

Traditional Banks and Credit Unions

Many traditional banks and credit unions offer personal loans. They often have competitive rates for borrowers with excellent credit scores and established banking relationships. However, their underwriting processes can be more rigid, relying heavily on FICO scores and extensive credit history. If you have a strong credit profile, it's worth checking with your existing bank or local credit union.

Online Lenders (Other than Upstart)

The online lending landscape is vast, with many platforms offering personal loans. Some, like Marcus by Goldman Sachs or SoFi, also offer prequalification with a soft credit pull. These lenders often have streamlined application processes and can provide quick funding. It's beneficial to compare interest rates, fees (including origination fee), and loan terms across multiple online lenders to find the most suitable option for your needs. Always pay attention to the annual percentage rate (APR), as it represents the true cost of borrowing.

Secured Personal Loans

If you have a lower credit score or limited credit history, a secured personal loan might be an option. These loans require collateral, such as a car or savings account, which reduces the lender's risk and can lead to easier approval and potentially lower interest rates. However, you risk losing your collateral if you fail to repay the loan.

Considering Your Credit Score

For individuals with fair credit or those looking for loans with a subprime borrower profile, exploring lenders that specialize in these areas is crucial. Some lenders are more forgiving of past credit issues or have programs specifically designed for credit building. Upstart's emphasis on non-traditional underwriting and alternative credit data makes it a strong contender for these borrowers, but it's not the only option.

Related Guides for Further Reading

To help you make an informed decision, explore these related guides on WiseIQ:

- Upstart Personal Loan Review 2026: Get a comprehensive overview of Upstart's offerings, pros, and cons.

- Upstart Loan Requirements: Dive deeper into the specific criteria Upstart uses for loan approval.

- How to Get Approved for an Upstart Loan: Learn strategies to improve your chances of approval.

- Is Upstart Legit?: Address common concerns about Upstart's legitimacy and reliability.

- Best Personal Loans 2026: Compare Upstart with other top personal loan providers.

- Upstart for Debt Consolidation: See how Upstart loans can help manage and reduce debt.

About the WiseIQ Editorial Team

The WiseIQ Editorial Team is comprised of experienced financial writers and analysts dedicated to providing accurate, unbiased, and actionable personal finance advice. Our mission is to empower readers to make smarter financial decisions through comprehensive guides, reviews, and comparisons.

Frequently Asked Questions About Upstart Prequalification

What is Upstart prequalification?

Upstart prequalification is a process that allows you to see potential loan offers and personalized rates from Upstart without undergoing a hard credit inquiry. It involves a soft credit pull, which means it won't affect your credit score. This gives you a risk-free way to gauge your eligibility and potential loan terms before committing to a full application.

Does Upstart prequalification hurt my credit score?

No, Upstart prequalification does not hurt your credit score. When you prequalify, Upstart performs a soft credit pull, which is only visible to you and does not impact your FICO score. A hard credit inquiry, which can temporarily lower your score, only occurs if you proceed with a full loan application after prequalification.

How long does Upstart prequalification take?

The Upstart prequalification process is typically very fast, often taking just a few minutes to complete online. You'll provide some basic personal and financial information, and Upstart's AI underwriting model will quickly generate personalized loan offers for you to review.

What information do I need for Upstart prequalification?

For Upstart prequalification, you'll generally need to provide your name, address, date of birth, income information, educational background, and employment history. Upstart uses this data, along with a soft credit pull, to assess your creditworthiness beyond just your FICO score.

Is prequalification a guarantee of loan approval?

No, prequalification is not a guarantee of loan approval. It provides an estimate of the loan amount and terms you might qualify for. If you decide to proceed with a full application, Upstart will conduct a hard credit inquiry and verify all your provided information. Final approval is contingent on meeting all their lending criteria.

What is the typical APR range for Upstart personal loans?

Upstart personal loans typically have an APR range from 6.40% to 35.99%. The specific APR you receive will depend on various factors, including your credit history, income, education, and other non-traditional credit factors assessed by Upstart's AI underwriting model. It's important to compare the APR across different lenders to understand the true cost of your loan.

Does Upstart charge an origination fee?

Yes, Upstart does charge an origination fee, which typically ranges from 0% to 12% of the loan amount. This fee is deducted from your loan proceeds before the funds are disbursed. The exact fee depends on your creditworthiness and other factors. There is no prepayment penalty if you decide to pay off your loan early.

Legal Disclaimer: The information provided on WiseIQ is for educational and informational purposes only, and does not constitute financial advice. Always consult with a qualified financial professional before making any financial decisions. Loan approval is subject to meeting the lender's criteria.