Bottom line: Upstart is our top pick for bad credit personal loans because it accepts scores as low as 300 and uses AI to evaluate factors beyond your credit score. Avant is best if you need funding fast. If you're focused on rebuilding credit, Self Financial's credit builder loan is the most accessible option with no minimum score.

Before accepting any loan offer, calculate the total cost of the loan (principal + all interest + fees). A lower monthly payment often means paying thousands more over the life of the loan.

What Counts as Bad Credit — and Why It Matters for Loans

FICO scores range from 300 to 850. Most lenders use the following tiers: Exceptional (800+), Very Good (740–799), Good (670–739), Fair (580–669), and Poor (below 580). A score below 580 is what most lenders call "bad credit," though some set their cutoff at 620.

Bad credit typically results from missed payments, high credit utilization (using more than 30% of your available credit), collections accounts, bankruptcies, or simply a short credit history. According to FICO data, payment history alone accounts for 35% of your score — a single 30-day late payment can drop a good score by 50–100 points.

What this means practically: with bad credit, you'll face higher APRs (often 25%–36%), lower loan limits, and more lender rejections. But you are not locked out of the market. Several lenders specialize in bad credit borrowers and use income, employment history, and other factors to evaluate you beyond just your score.

How We Evaluated These Lenders

We reviewed 20+ personal loan lenders and narrowed the list based on: minimum credit score requirements, APR range (lower is better), origination fees, funding speed, loan amounts available, and whether the lender reports to all three credit bureaus. We prioritized lenders with transparent eligibility criteria and no prepayment penalties. Rates shown are current as of March 2026 but can change — always verify on the lender's site before applying.

Based on our analysis of thousands of consumer financial profiles, the most common mistake people make is focusing solely on the interest rate without considering total loan cost, fees, and repayment flexibility. Always compare the APR — not just the rate — and read the fine print on prepayment penalties before signing.

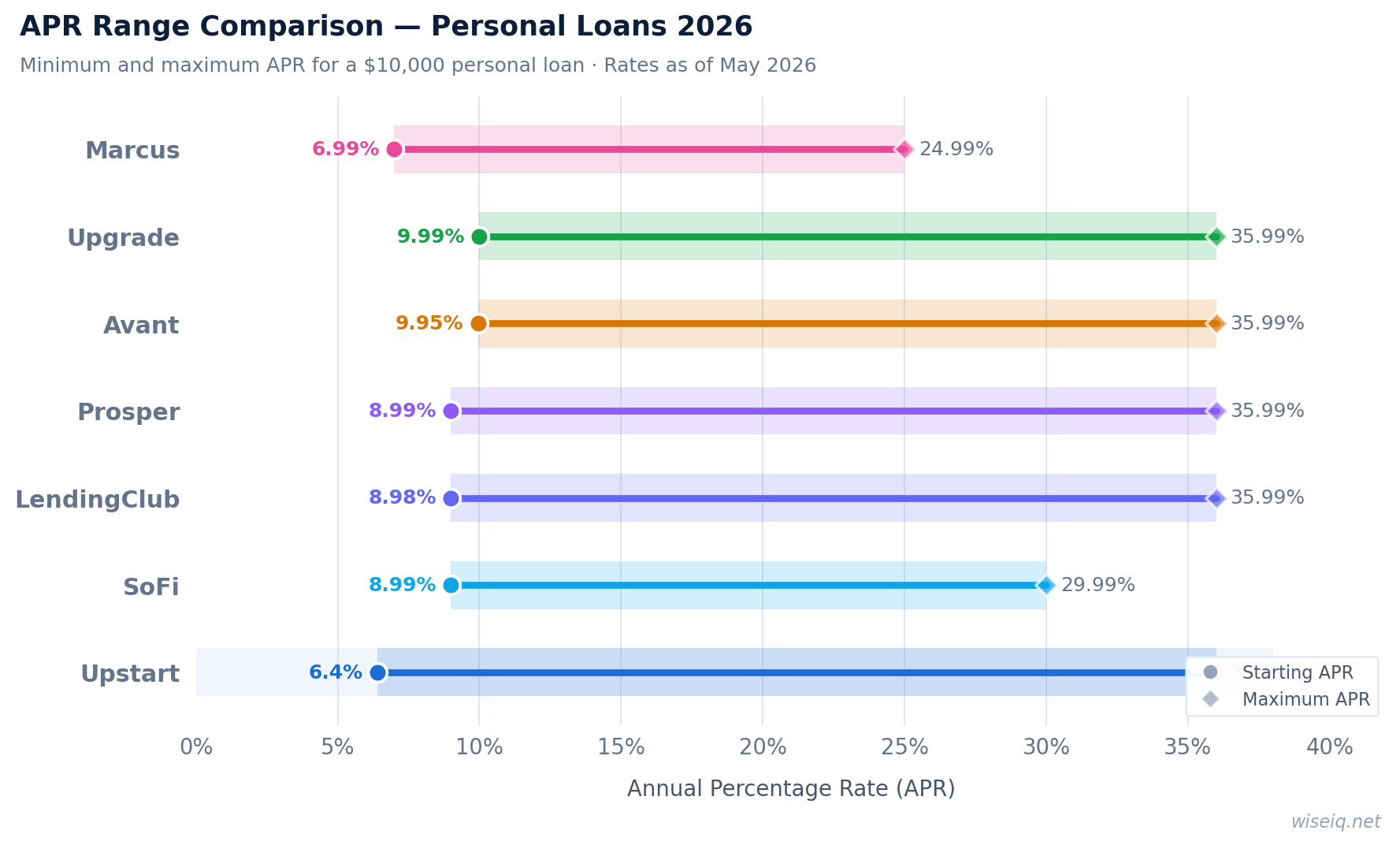

Best Personal Loans for Bad Credit in 2026

Upstart's AI underwriting model evaluates over 1,000 data points including education, job history, and income — not just your credit score. This is why it can approve borrowers that traditional lenders reject. It accepts scores as low as 300, the lowest minimum of any major lender. Origination fee 0%–12%. No prepayment penalty. Funds typically deposited within 1–3 business days.

Best for: Borrowers with low credit scores but stable income or a college degree. Not ideal if you have high debt-to-income ratio or no income history.

Avant specializes in fair-to-poor credit borrowers and is one of the fastest lenders in this space — funds can arrive as soon as the next business day after approval. The application is fully online and takes about 10 minutes. Administration fee up to 9.99% (charged upfront, deducted from loan proceeds). No prepayment penalty.

Best for: Borrowers with scores between 580–650 who need money quickly. The 9.99% administration fee is steep — factor it into your total cost calculation.

Self offers a credit builder loan — you make monthly payments into a locked savings account, and the money is released to you at the end of the term. It reports to all three bureaus every month. There's no credit check to apply. The interest you pay is the cost of building credit history — think of it as a structured savings plan that also improves your score.

Best for: People with no credit history or very damaged credit who need to build a payment history from scratch. Not a traditional loan — you won't receive funds upfront.

OneMain Financial has physical branches in 44 states and offers both secured and unsecured personal loans. The secured option — backed by your vehicle — can get you a lower rate even with very poor credit. Origination fee varies by state (flat fee or percentage). APR floor of 18% is higher than competitors, but approval rates for poor credit borrowers are strong.

Best for: Borrowers who own a vehicle and want to use it as collateral to lower their rate. Also good for those who prefer in-person service.

A personal loan is not the right tool for every situation. Consider alternatives if any of the following apply to you:

- You have home equity: A HELOC typically offers rates 5–10% lower than personal loans. If you own your home, compare HELOC rates before taking a personal loan.

- Your debt is primarily credit card debt: A balance transfer card with a 0% intro APR (typically 12–21 months) will cost less than a personal loan if you can pay off the balance within the intro period.

- You need less than $1,000: Most personal loan lenders have minimum amounts of $1,000–$2,000. For smaller needs, a credit union payday alternative loan (PAL) or a 0% APR credit card may be more appropriate.

- Your credit score is below 500: Most personal loan lenders — including those that accept "bad credit" — have practical minimums around 500–560. Below this, secured loans, credit-builder loans, or co-signer arrangements are more realistic options.

- You are in active bankruptcy: Personal loan lenders will decline applicants in active Chapter 7 or Chapter 13 proceedings. Resolve your bankruptcy first.

Answer 3 quick questions and get a personalized recommendation in seconds.

Side-by-Side Comparison

| Lender | APR Range | Loan Amount | Min Score | Origination Fee | Funding Speed |

|---|---|---|---|---|---|

| Upstart | 6.2%–35.99% | $1K–$75K | 300 | 0%–12% | 1–3 days |

| Avant | 9.95%–35.99% | $2K–$35K | 580 | Up to 9.99% | Next day |

| Self Financial | Credit builder | $600–$1,800 | None | $9 admin fee | N/A (savings) |

| OneMain Financial | 18%–35.99% | $1.5K–$20K | None stated | Varies by state | Same day possible |

Real Borrower Scenarios: What to Expect

Scenario 1: Score 520, $38,000 annual income, no collections

With a 520 score and stable income, Upstart is your best bet. Their AI model will weight your income heavily. You'll likely qualify for $5,000–$15,000 at 28%–35% APR. On a $7,500 loan at 32% APR over 36 months, your monthly payment would be approximately $320 and total interest paid would be roughly $2,700. That's expensive — only borrow what you genuinely need.

Scenario 2: Score 590, $55,000 annual income, one late payment

At 590, you're at the low end of "fair" credit. Both Upstart and Avant will approve you. With $55K income and only one late payment, you may qualify for rates in the 18%–25% range. Shop both lenders — pre-qualifying takes 2 minutes and won't affect your score. On a $10,000 loan at 22% APR over 48 months, monthly payment is about $290 and total interest is approximately $3,900.

Scenario 3: Score 480, recent collection account, $28,000 income

This is a difficult profile. Upstart may still approve you, but expect rates near the 35.99% ceiling. OneMain Financial with a secured loan (using your vehicle) is worth exploring — the collateral can offset the risk. Alternatively, Self Financial's credit builder loan is the most accessible path: no credit check, $25–$150/month, and you'll have a positive payment history within 6 months that opens more doors.

How to Improve Your Approval Odds with Bad Credit

Even with bad credit, there are concrete steps that meaningfully increase your chances of approval and can lower your rate.

Pre-Qualify with Multiple Lenders First

Most online lenders offer pre-qualification with a soft credit pull — this shows you estimated rates and terms without affecting your score. Always pre-qualify with at least 3 lenders before formally applying. The difference between lenders can be 10+ percentage points in APR for the same borrower profile. Use our Personal Loan Calculator to compare monthly payments across different rate scenarios before you decide.

Add a Co-Signer

A co-signer with good credit (670+) takes on equal legal responsibility for the loan. This significantly reduces the lender's risk and can result in a dramatically lower APR — sometimes 10–15 percentage points lower. The co-signer's credit score and income are factored into the approval decision. The critical caveat: if you miss payments, it damages your co-signer's credit just as much as yours. Only use a co-signer if you are fully confident in your ability to repay.

Apply for a Secured Loan

Secured personal loans require collateral — typically a savings account, certificate of deposit, or vehicle. Because the lender can recover the collateral if you default, they're more willing to approve borrowers with poor credit and offer lower rates. OneMain Financial and Avant both offer secured personal loan options. The risk is clear: defaulting means losing the collateral.

Reduce Your Debt-to-Income Ratio Before Applying

Your debt-to-income (DTI) ratio — total monthly debt payments divided by gross monthly income — is evaluated alongside your credit score. Most lenders want to see a DTI below 40%, with the best rates going to borrowers under 36%. If you have high-interest credit card debt, paying it down before applying for a personal loan can improve both your DTI and your credit utilization ratio simultaneously. Use our DTI Calculator to see where you stand.

Wait 6 Months and Build Your Score First

If your need isn't urgent, the most cost-effective approach is to spend 6 months improving your credit before applying. The difference between a 520 and 620 score can be 10+ percentage points in APR — on a $10,000 loan over 3 years, that's $3,000+ in interest savings. The fastest legitimate ways to raise your score: pay down credit card balances to under 10% utilization, dispute any errors on your credit report, and make every payment on time. See our guide: How to Improve Your Credit Score Fast.

Watch out for predatory lenders. If a lender guarantees approval before reviewing your application, charges fees before disbursing funds, or has an APR above 36%, walk away. Payday loans and some online "bad credit" lenders charge effective APRs of 200%–400%. The lenders listed on this page are legitimate — always verify a lender's license with your state's banking regulator before applying.

Find Your Best Rate in 2 Minutes

Answer 5 quick questions and see personalized loan offers matched to your credit profile — no credit pull required.

Check My Options →What to Do After Getting a Bad Credit Loan

Getting approved is step one. Using the loan to actually improve your financial situation is step two — and it's where most people fall short.

If you took the loan for debt consolidation, close or freeze the credit cards you paid off. The biggest mistake is paying off cards and then running them back up, leaving you with both the loan payment and new card debt. If you took the loan for an emergency expense, build an emergency fund of $1,000–$3,000 as your next priority so you don't need another high-rate loan next time.

Most importantly: set up autopay. A single missed payment on your new loan undoes months of credit score progress. Most lenders offer a 0.25%–0.5% APR discount for autopay enrollment — that's free money.

Frequently Asked Questions

Can I get a personal loan with a 500 credit score?

Yes. Upstart accepts scores as low as 300, and Avant accepts scores from 580. With a 500 score, your options are limited and rates will be high (typically 25%–36% APR), but approval is possible — especially if you have stable income and a low debt-to-income ratio. Pre-qualify with Upstart first; their AI model is the most favorable for low-score borrowers with good income.

What is the easiest personal loan to get with bad credit?

Upstart is generally the easiest to qualify for because its AI model considers education, job history, and income alongside your credit score. Self Financial's credit builder loan has no minimum score requirement at all and no credit check — though it's not a traditional loan (you don't receive funds upfront).

Will a bad credit personal loan help my credit score?

Yes, if you make all payments on time. Personal loans add installment credit to your credit mix (10% of your FICO score), and consistent on-time payments are reported to all three bureaus and build your payment history (35% of your score). Most borrowers see meaningful improvement within 6–12 months of consistent payments.

What APR should I expect with bad credit?

With a score below 580, expect APRs in the 25%–36% range from most lenders. Upstart's AI model may offer lower rates if your income and employment history are strong despite your score. Always compare at least 3 lenders — the same borrower can receive quotes that differ by 10+ percentage points.

How much can I borrow with bad credit?

Most bad credit lenders cap loans at $10,000–$35,000 for first-time borrowers. Upstart goes up to $75,000 but requires strong income. OneMain Financial offers up to $20,000 and accepts secured loans for higher amounts. Borrowing less than you need is rarely the problem — borrowing more than you can repay is the real risk.

Should I use a co-signer to get a better rate?

Yes, if someone is willing and you are certain you can repay. A co-signer with good credit (670+) can lower your APR by 10–15 percentage points and significantly improve approval odds. The risk: if you miss payments, it damages both your credit and your co-signer's credit equally. Never use a co-signer unless you have a clear repayment plan.