Navigating the personal loan landscape with a fair credit score (typically 580-669 FICO) can feel challenging, but it's far from impossible. Many reputable lenders specialize in offering financial solutions to individuals who may not have perfect credit, providing access to funds for debt consolidation, unexpected expenses, or major purchases. This guide will help you discover the best personal loans for fair credit in 2026, detailing options from lenders known for working with this credit range, outlining typical interest rates, and offering practical advice to improve your chances of approval.

Before accepting any loan offer, calculate the total cost of the loan (principal + all interest + fees). A lower monthly payment often means paying thousands more over the life of the loan.

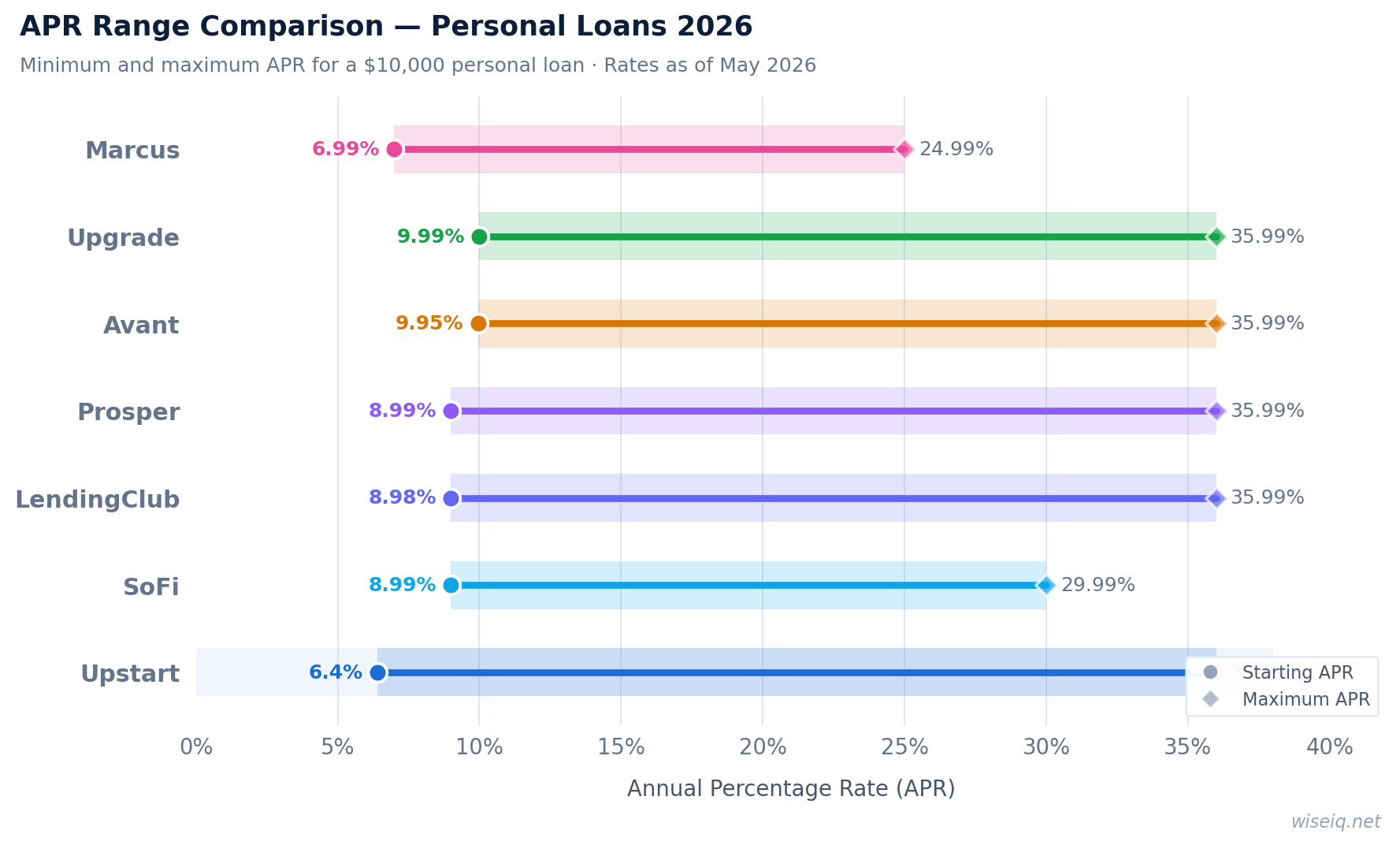

Our Top Personal Loan Picks for Fair Credit in 2026

Avant is a popular choice for fair credit borrowers, offering personal loans with a minimum credit score requirement of 580. They provide a straightforward application process and quick funding, making them suitable for those needing fast access to funds. Avant considers more than just your credit score, looking at your overall financial picture.

LendingClub operates as a peer-to-peer lending platform, which can be advantageous for fair credit applicants. They offer competitive rates for those with a credit score of 600 or higher, focusing on helping borrowers consolidate debt or finance larger expenses. The platform's structure often provides more flexible terms than traditional banks.

OneMain Financial specializes in serving borrowers with less-than-perfect credit, including those with fair credit scores as low as 580. They offer both secured and unsecured loan options, and their personalized approach often involves an in-person meeting to discuss your financial situation, which can be beneficial for approval.

Best Egg provides unsecured personal loans for a variety of purposes, with a minimum credit score requirement of 600. They are known for their quick online application process and fast funding, often depositing funds within one business day. Best Egg's focus on a holistic view of your finances can aid fair credit borrowers.

Prosper is another peer-to-peer lending platform that can be a good option for fair credit borrowers, with a minimum credit score of 560. They offer fixed-rate, fixed-term loans that can be used for debt consolidation, home improvement, or other large expenses. Prosper's community-driven model can sometimes provide more accessible terms.

Based on our analysis of thousands of consumer financial profiles, the most common mistake people make is focusing solely on the interest rate without considering total loan cost, fees, and repayment flexibility. Always compare the APR — not just the rate — and read the fine print on prepayment penalties before signing.

Understanding Personal Loans for Fair Credit

Fair credit, typically defined as a FICO score between 580 and 669, indicates that you have some credit history but may have experienced a few financial missteps or have a limited credit profile. While this score range might limit your options compared to those with excellent credit, it certainly doesn't close the door to personal loans. Lenders who specialize in fair credit loans understand these nuances and often use alternative data points, beyond just your credit score, to assess your creditworthiness. This can include your employment history, income stability, and educational background, as seen with lenders like Upstart.

One of the primary differences you'll encounter with fair credit personal loans is the interest rate. Borrowers with fair credit typically face higher Annual Percentage Rates (APRs) than those with good or excellent credit. While the best rates might start around 6-8% for prime borrowers, fair credit borrowers can expect APRs to range from the high single digits to upwards of 35.99%. This higher rate compensates lenders for the increased risk associated with lending to individuals with a less robust credit history. It's crucial to compare offers from multiple lenders to find the most competitive rate available to you.

Loan amounts and terms can also vary. While some lenders offer loans up to $50,000 or more, fair credit borrowers might initially qualify for smaller amounts. Repayment terms typically range from 24 to 60 months. Understanding these factors is key to choosing a loan that fits your budget and financial goals. Always review the total cost of the loan, including any origination fees, to make an informed decision.

A personal loan is not the right tool for every situation. Consider alternatives if any of the following apply to you:

- You have home equity: A HELOC typically offers rates 5–10% lower than personal loans. If you own your home, compare HELOC rates before taking a personal loan.

- Your debt is primarily credit card debt: A balance transfer card with a 0% intro APR (typically 12–21 months) will cost less than a personal loan if you can pay off the balance within the intro period.

- You need less than $1,000: Most personal loan lenders have minimum amounts of $1,000–$2,000. For smaller needs, a credit union payday alternative loan (PAL) or a 0% APR credit card may be more appropriate.

- Your credit score is below 500: Most personal loan lenders — including those that accept "bad credit" — have practical minimums around 500–560. Below this, secured loans, credit-builder loans, or co-signer arrangements are more realistic options.

- You are in active bankruptcy: Personal loan lenders will decline applicants in active Chapter 7 or Chapter 13 proceedings. Resolve your bankruptcy first.

Answer 3 quick questions and get a personalized recommendation in seconds.

Maximizing Your Approval Chances with Fair Credit

Even with a fair credit score, there are several proactive steps you can take to significantly improve your chances of getting approved for a personal loan and potentially secure more favorable terms. The first and most critical step is to check your credit report for inaccuracies. Errors on your report can unfairly lower your score, so disputing and correcting them can provide an immediate boost. Websites like AnnualCreditReport.com allow you to get a free report from each of the three major bureaus annually.

Next, focus on your **debt-to-income (DTI) ratio**. Lenders look at your DTI to determine if you can comfortably afford new loan payments. A lower DTI (ideally below 36%) indicates less risk. If your DTI is high, consider paying down existing debts before applying for a new loan. This not only improves your DTI but also demonstrates responsible financial behavior.

Consider applying with a **co-signer**. A co-signer with good or excellent credit can significantly strengthen your application. Their creditworthiness provides an additional layer of security for the lender, often leading to better approval odds and lower interest rates. However, remember that a co-signer is equally responsible for the debt, so choose someone you trust and who understands the commitment.

Exploring **secured personal loan options** can also be a viable strategy. While unsecured loans don't require collateral, secured loans do, using assets like a car or savings account to back the loan. This reduces the lender's risk, making them more willing to approve applicants with fair credit, often at lower interest rates. OneMain Financial, for example, offers secured options.

Finally, **apply to lenders known for working with fair credit**. As highlighted in our top picks, some lenders specialize in this market segment and have more flexible underwriting criteria. Avoid applying to too many lenders at once, as multiple hard inquiries can temporarily ding your credit score. Instead, pre-qualify with a few lenders to see potential offers without impacting your score.