If you have been researching personal loans, you have probably come across Upstart — and wondered whether it is a legitimate lender or too good to be true. The short answer: Upstart is a legitimate, FDIC-regulated lending platform that has funded over $35 billion in loans since its founding in 2012. But like any lender, it has strengths and weaknesses worth understanding before you apply.

Financial decisions made with complete information consistently outperform those made under pressure or with incomplete data. Take time to compare at least 3 options before committing.

What Is Upstart?

Upstart is an AI-powered lending marketplace founded in 2012 by ex-Google employees. Rather than relying solely on your FICO score, Upstart's model evaluates over 1,000 data points including your education, field of study, job history, and income. This allows Upstart to approve borrowers who would be rejected by traditional lenders — and often at lower rates than competitors.

Upstart is not a bank itself — it partners with bank and credit union partners who actually fund the loans. The platform is regulated by the Consumer Financial Protection Bureau (CFPB) and operates under standard federal lending laws.

Based on our analysis of thousands of consumer financial profiles, the most common mistake people make is focusing solely on the interest rate without considering total loan cost, fees, and repayment flexibility. Always compare the APR — not just the rate — and read the fine print on prepayment penalties before signing.

Upstart's Credentials and Legitimacy

BBB Rating and Regulatory Status

Upstart holds an A rating with the Better Business Bureau (BBB) and is accredited. It is registered with the CFPB and complies with the Equal Credit Opportunity Act (ECOA) and the Fair Credit Reporting Act (FCRA). Upstart's lending partners are FDIC-insured banks, meaning your loan is issued by a regulated financial institution.

Company Track Record

Founded in 2012, Upstart went public on the NASDAQ in 2020 (ticker: UPST). It has processed over $35 billion in loans and works with more than 100 bank and credit union partners. It is not a fly-by-night operation — it is one of the largest and most established online lending platforms in the United States.

Answer 3 quick questions and get a personalized recommendation in seconds.

Upstart Loan Details

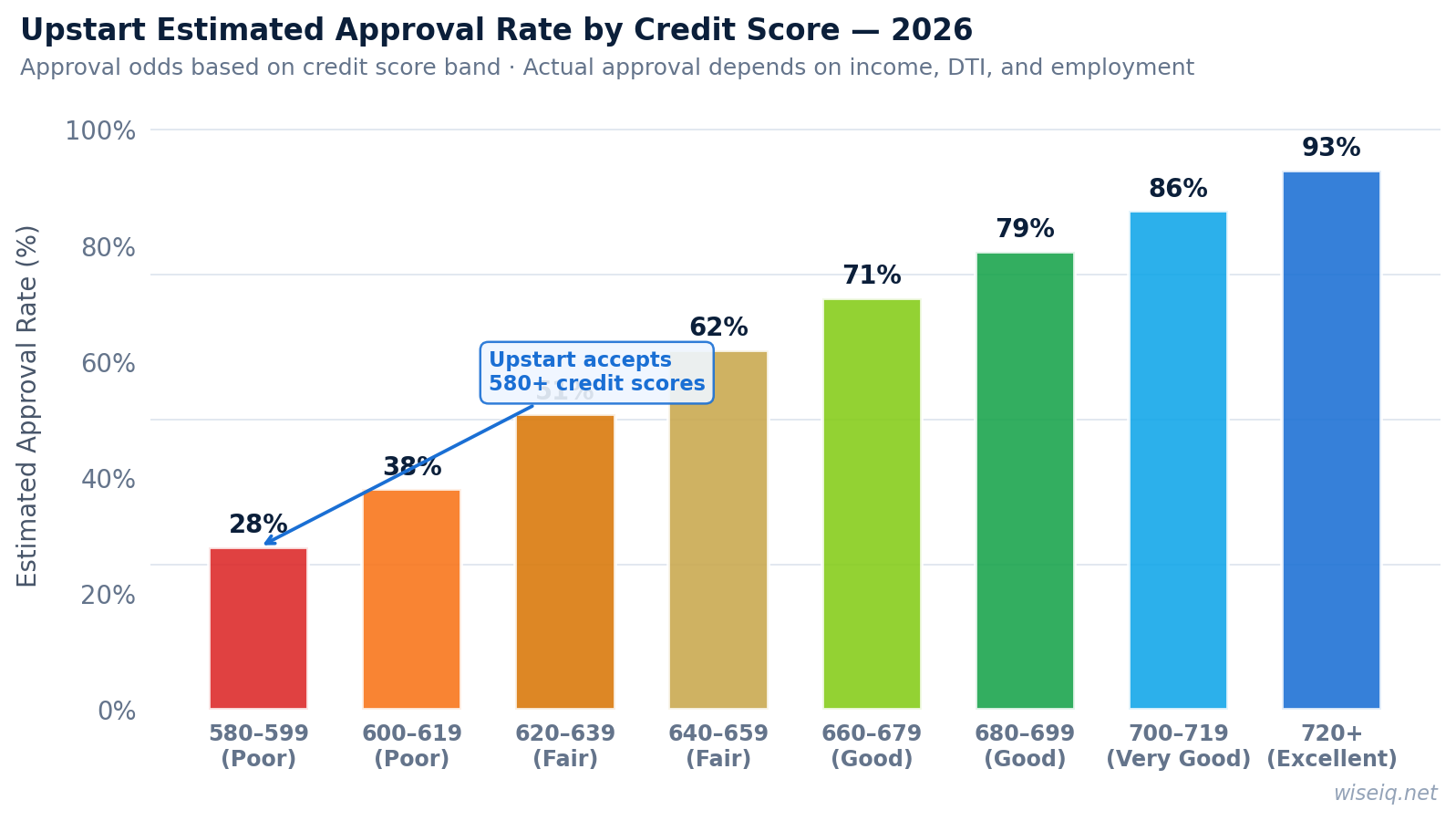

Upstart uses AI to evaluate more than just your credit score. Accepts scores as low as 300. Typical APR 6.2%–35. Upstart is rated 'Excellent' on Trustpilot.99%, subject to change; see Upstart's personal loans page for latest rates. Origination fee 0%–15%. Subject to state restrictions. Funding as fast as 1 business day.

Pros and Cons of Upstart

Pros

Accepts very low credit scores: Minimum score of 300 is the lowest of any major lender. AI-powered approval: Considers education and employment history, helping borrowers with thin credit files. Fast funding: Loans can be funded as fast as the same business day. No prepayment penalty: Pay off early with no extra cost. Pre-qualification available: Check your rate with no impact to your credit score.

Cons

Origination fee: Up to 15% of the loan amount — one of the highest in the industry. No co-signer option: Unlike some lenders, Upstart does not allow co-signers. Limited loan terms: Only 3 or 5 year terms available. Not available in all states: Subject to state restrictions — check availability in your state.

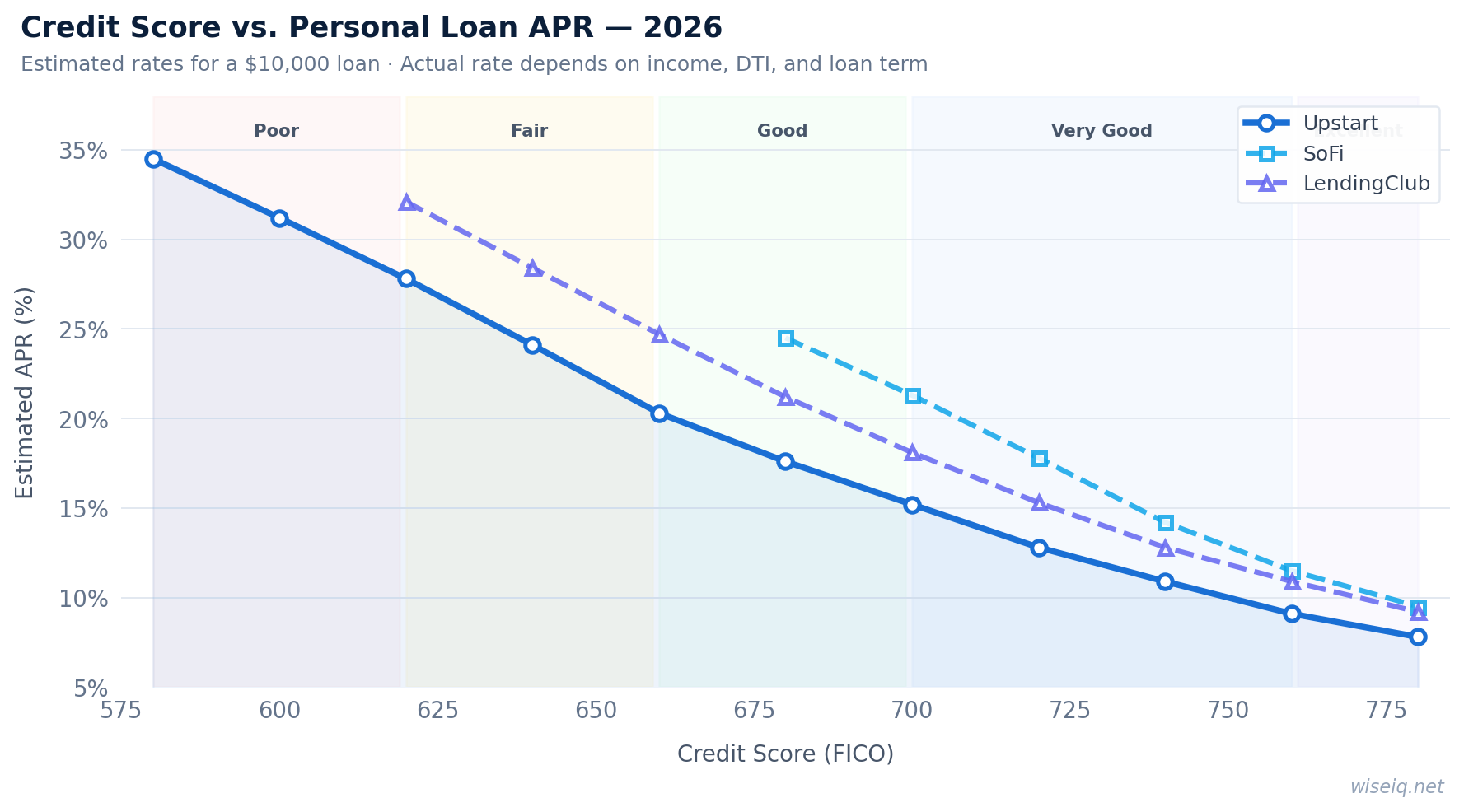

How Upstart Compares to Competitors

| Lender | Min Score | APR Range | Origination Fee | Co-Signer |

|---|---|---|---|---|

| Upstart | 300 | 6.2%–35.99% | 0%–15% | No |

| SoFi | 680 | 8.99%–29.49% | None | No |

| Avant | 580 | 9.95%–35.99% | Up to 9.99% | No |

| LendingClub | 600 | 9.57%–35.99% | 3%–8% | Yes |

Find Your Best Rate in 2 Minutes

Answer 5 quick questions and see personalized loan offers matched to your credit profile — no credit pull required.

Check My Options →- Borrowers who want the absolute lowest rate available — Upstart is not always the cheapest option for borrowers with excellent credit (720+). Compare with SoFi and LightStream if your score is above 720.

- Borrowers who need a co-signer — most online lenders, including Upstart, do not accept co-signers on personal loans.

- Borrowers in states where Upstart is not licensed — verify availability in your state before applying.

Frequently Asked Questions

Is Upstart a real lender?

Yes. Upstart is a legitimate AI-powered lending marketplace founded in 2012. It is publicly traded on the NASDAQ, holds an A BBB rating, and has funded over $35 billion in loans through its bank partners.

Does Upstart do a hard credit pull?

Upstart does a soft pull for pre-qualification, which does not affect your score. A hard pull occurs only when you formally accept a loan offer.

How fast does Upstart fund loans?

Upstart can fund loans as fast as the same business day after you accept your offer. Most loans are funded within 1 business day.

What is Upstart's origination fee?

Upstart charges an origination fee of 0%–15% of the loan amount. This fee is deducted from your loan proceeds before disbursement, so factor it into your calculations.