Top Personal Loans for 660 Credit Score

You're approaching good credit territory. Most lenders will approve you, and you can start negotiating better terms.

Before accepting any loan offer, calculate the total cost of the loan (principal + all interest + fees). A lower monthly payment often means paying thousands more over the life of the loan.

Rates are 1–4% above prime borrowers.

Pay down revolving balances to below 20% utilization for the fastest score improvement.

Timeline: 3–9 months to reach the 700+ threshold.

Zero fees of any kind. Fixed rates. On-time payment reward lets you defer one payment per year.

No fees, unemployment protection, and member benefits. Check if you pre-qualify.

No fees at all — including no late fee on your first late payment. 30-day money-back guarantee (subject to Discover's program terms).

Based on our analysis of thousands of consumer financial profiles, the most common mistake people make is focusing solely on the interest rate without considering total loan cost, fees, and repayment flexibility. Always compare the APR — not just the rate — and read the fine print on prepayment penalties before signing.

What to Know About Personal Loans with a 660 Score

Your credit score is one of the most important factors lenders use to determine your interest rate and loan amount. A 660 score (Good Credit) means you have a solid credit history with room for improvement. Understanding where you stand helps you target the right lenders and negotiate better terms.

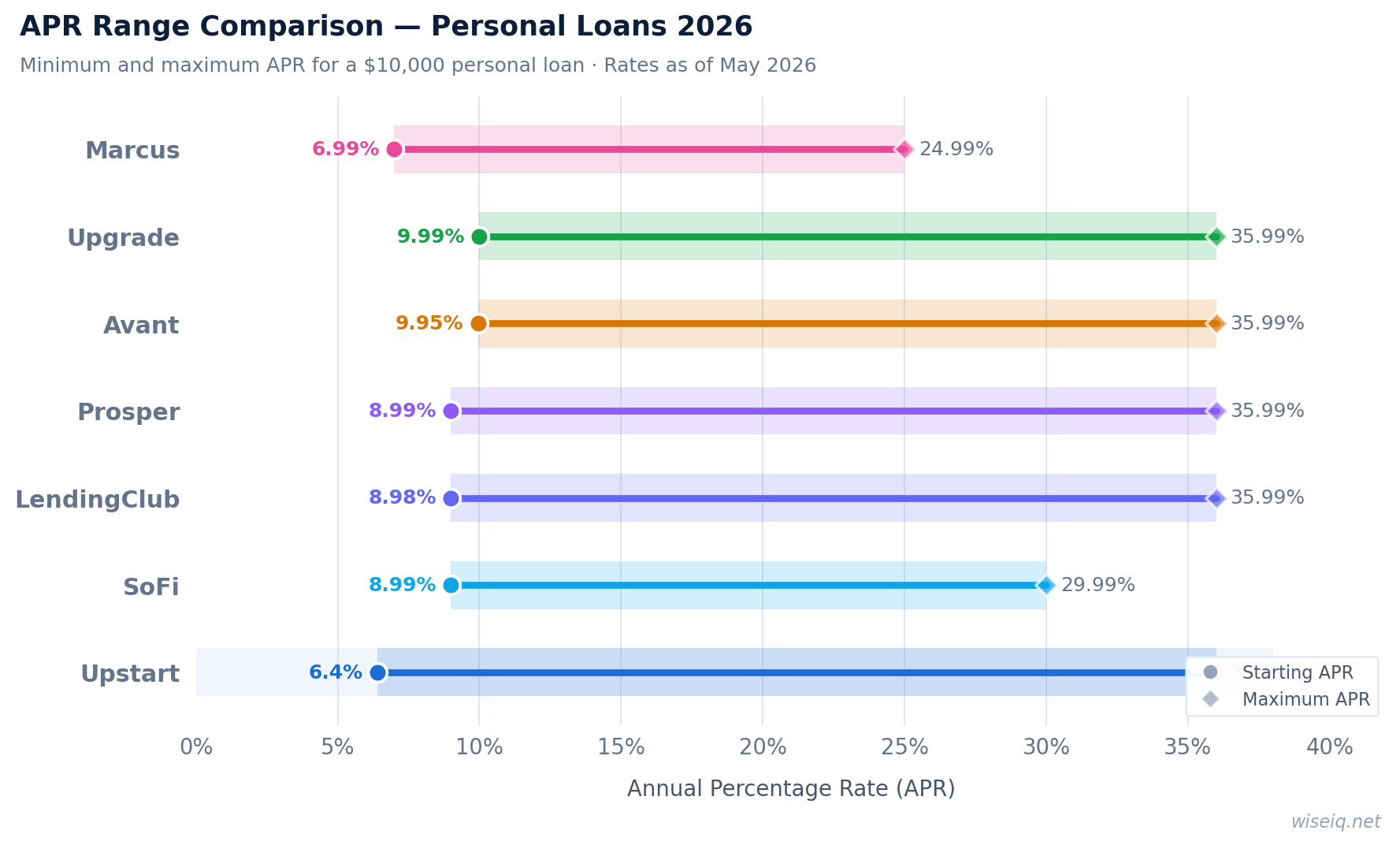

When comparing personal loans, focus on the Annual Percentage Rate (APR) rather than just the interest rate. The APR includes all fees and gives you the true cost of borrowing. Also compare loan amounts, repayment terms, and whether the lender charges origination fees, prepayment penalties, or late fees.

Answer 3 quick questions and get a personalized recommendation in seconds.

How to Get the Best Rate with a 660 Score

Even with a 660 credit score, there are several strategies to improve your offered rate. First, always pre-qualify with multiple lenders before accepting any offer — this uses a soft credit pull that doesn't affect your score, and comparing offers takes less than 10 minutes. Second, consider the loan term carefully: shorter terms typically come with lower interest rates, though monthly payments will be higher. Third, if you have a trusted family member or friend with excellent credit, adding them as a co-signer can significantly lower your rate.

Reducing your debt-to-income ratio before applying is another powerful lever. Lenders look at how much of your monthly income goes toward debt payments — a ratio below 35% is generally considered favorable. Paying down existing credit card balances before applying can improve both your credit score and your debt-to-income ratio simultaneously.

Find Your Best Personal Loan

Compare rates from top lenders in 2 minutes. No credit impact.

Compare Personal Loan Rates →