Navigating the personal loan landscape with a fair credit score (typically 580-650) can be challenging, but lenders like Upstart and Avant specialize in serving this demographic. Both offer accessible personal loans, but their approaches, terms, and ideal borrower profiles differ significantly. Upstart is rated 'Excellent' on Trustpilot. This guide dives deep into an Upstart vs. Avant personal loans comparison for 2026, examining their APRs, fees, credit requirements, funding speed, and ultimately, helping you decide which lender is the better fit for your financial needs.

Financial decisions made with complete information consistently outperform those made under pressure or with incomplete data. Take time to compare at least 3 options before committing.

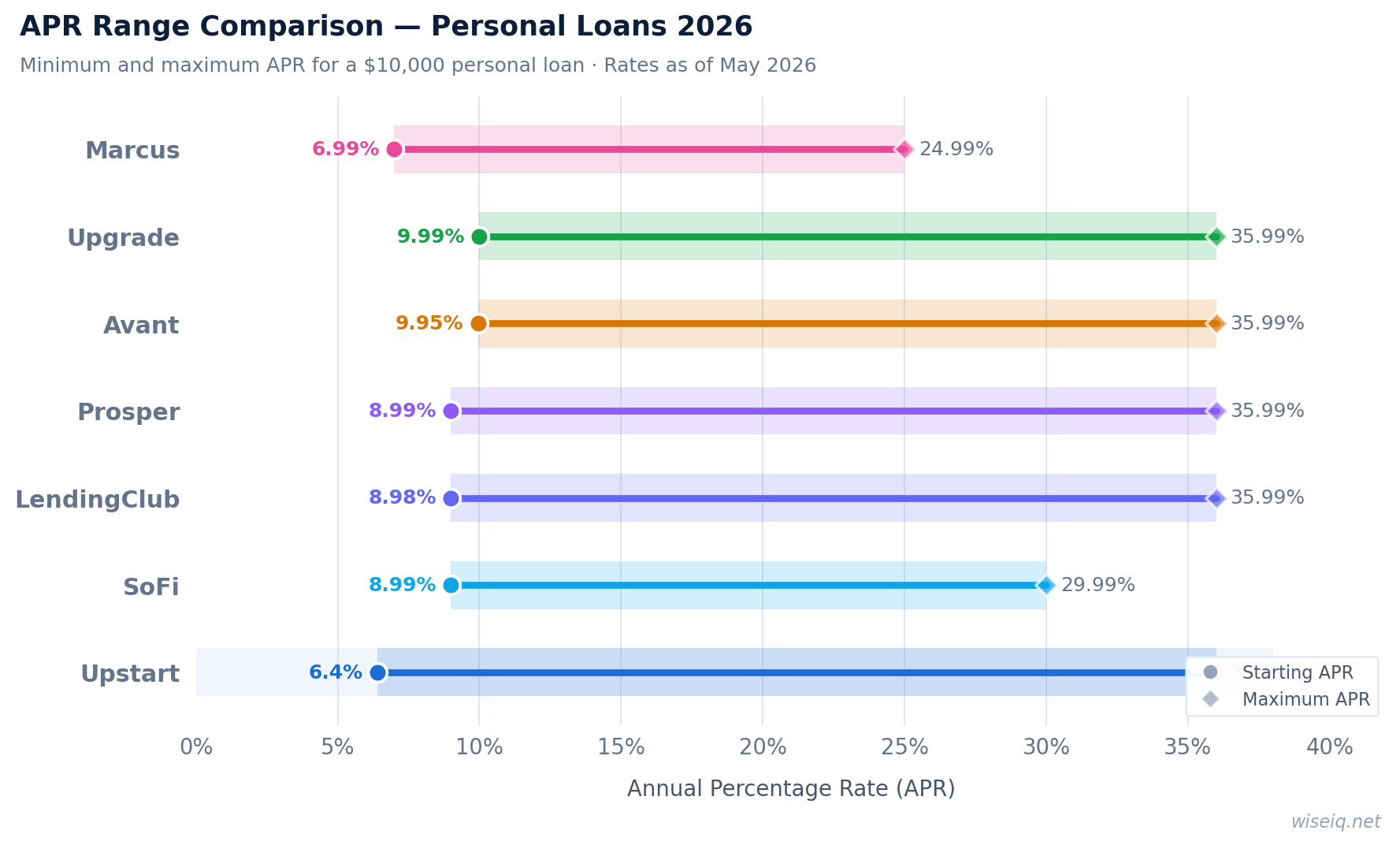

Key Differences at a Glance

When comparing Upstart and Avant for personal loans, it is crucial to understand their core offerings and how they cater to fair credit borrowers. While both aim to provide financial solutions, their underwriting models and target audiences have distinct characteristics. The table below provides a quick overview of their key features:

| Feature | ||

|---|---|---|

| Min. Credit Score | 300 (but considers other factors) | 580 |

| APR Range | 6.2% – 35.99% | 9.95% – 35.99% |

| Loan Amounts | $1,000 – $75,000 | $2,000 – $35,000 |

| Origination Fees | 0% – 12% (deducted from loan proceeds) | Up to 9.99% (deducted from loan proceeds) |

| Funding Speed | As fast as 1 business day | As fast as 1 business day |

| Ideal Borrower | Fair credit, limited credit history, strong earning potential, higher education | Fair credit (580+), predictable income, need for quick funds |

Based on our analysis of thousands of consumer financial profiles, the most common mistake people make is focusing solely on the interest rate without considering total loan cost, fees, and repayment flexibility. Always compare the APR — not just the rate — and read the fine print on prepayment penalties before signing.

Upstart Personal Loans: What to Know

Upstart distinguishes itself with an AI-driven underwriting model that looks beyond traditional credit scores. While a minimum FICO score of 300 is often cited, Upstart considers factors like education, employment history, and income potential. This approach can be particularly beneficial for fair credit borrowers who may have a limited credit history but demonstrate strong financial responsibility through other metrics.

Key Details:

- APR Range: 6.2% – 35.99%

- Loan Amounts: $1,000 – $75,000

- Fees: Origination fees range from 0% to 12%, which are typically deducted from the loan proceeds.

- Credit Requirements: While a 300 FICO is the stated minimum, Upstart's model evaluates a broader set of data points. This means individuals with fair credit (580-650) who have strong educational backgrounds or promising career paths might secure more favorable rates.

- Funding Speed: Upstart is known for its efficiency, often disbursing funds as fast as one business day after loan acceptance.

- Best For: Borrowers with fair credit, especially those with limited credit history, strong earning potential, or higher education who might be overlooked by traditional lenders.

Upstart is ideal for fair credit borrowers who may have a limited credit history but strong earning potential, leveraging AI to assess creditworthiness beyond just FICO scores.

Answer 3 quick questions and get a personalized recommendation in seconds.

Avant Personal Loans: What to Know

Avant focuses on providing personal loans to individuals with fair to good credit, typically those with FICO scores of 580 and above. Their application process is straightforward, and they are known for quick funding, making them a popular choice for those who need access to funds relatively fast. Avant's model is more traditional than Upstart's, relying heavily on credit scores and income stability.

Key Details:

- APR Range: 9.95% – 35.99%

- Loan Amounts: $2,000 – $35,000

- Fees: Avant charges an administration fee of up to 9.99%, which is also deducted from the loan proceeds.

- Credit Requirements: A minimum FICO score of 580 is generally required, making it accessible for many fair credit borrowers.

- Funding Speed: Similar to Upstart, Avant often deposits funds into the borrower's account as soon as the next business day after approval.

- Best For: Fair credit borrowers (580-650) who have a predictable income and need quick access to funds, and prefer a lender with a clear, traditional credit assessment process.

Avant is a strong option for fair credit borrowers (580+ FICO) who need quick funding and appreciate a straightforward application process based on traditional credit metrics.

Who Wins for Fair Credit Borrowers (580-650)?

The choice between Upstart and Avant largely depends on your specific financial profile and needs within the 580-650 credit score range:

Who Upstart Is Best For

⚠️ Not a fit if: you need a secured loan, have a bankruptcy in the last 12 months, or need more than $50,000.

What Happens When You Click — 3 Steps

Soft pull only · No impact to your credit score · Takes 2 minutes