Navigating the personal loan landscape can be challenging, especially when comparing lenders like Upstart and Prosper. Both offer accessible personal loans, but they utilize distinct approaches to assess borrower eligibility and structure their loan products. Upstart is rated 'Excellent' on Trustpilot. Understanding the nuances of an Upstart vs Prosper personal loan comparison is crucial for borrowers with credit scores ranging from 580 to 720, as each platform caters to slightly different financial profiles and needs. This guide will delve into their underwriting methods, APR ranges, associated fees, and credit score requirements to help you make an informed decision in 2026.

Financial decisions made with complete information consistently outperform those made under pressure or with incomplete data. Take time to compare at least 3 options before committing.

Underwriting Models: AI-Driven vs. Peer-to-Peer

One of the most significant distinctions between an Upstart vs Prosper personal loan lies in their underwriting methodologies. Upstart pioneered an AI-driven approach that goes beyond traditional credit scores. Thei

Prosper, on the other hand, operates as a peer-to-peer lending platform. This means individual investors fund the loans, and borrowers are assigned a "Prosper Rating" (from AA to HR) based on their credit profile. While Prosper also aims to provide accessible loans, its underwriting is more aligned with traditional metrics, placing a stronger emphasis on credit scores and debt-to-income ratios. This model can be beneficial for borrowers with a solid credit history who are looking for potentially competitive rates from a community of investors.

Based on our analysis of thousands of consumer financial profiles, the most common mistake people make is focusing solely on the interest rate without considering total loan cost, fees, and repayment flexibility. Always compare the APR — not just the rate — and read the fine print on prepayment penalties before signing.

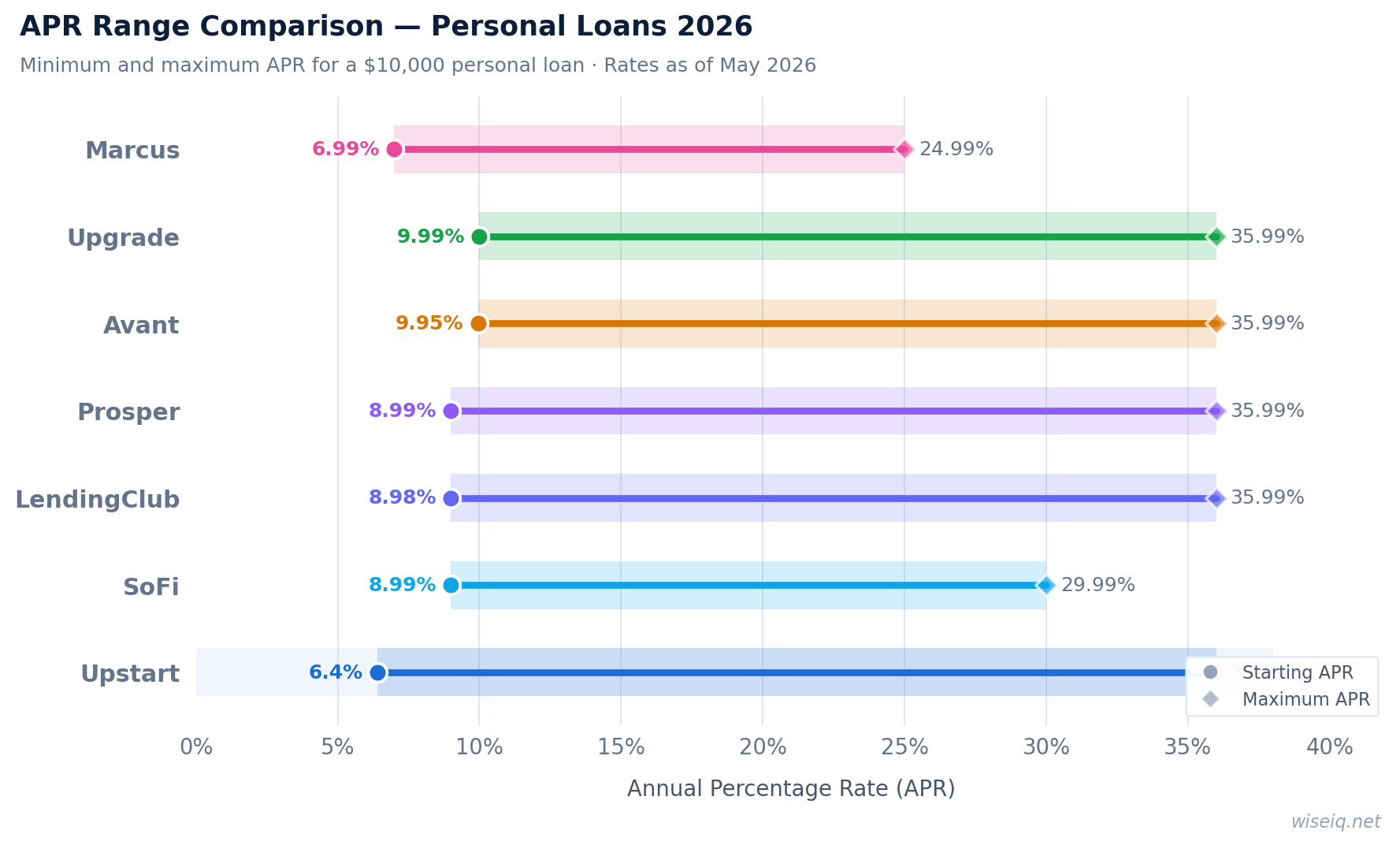

APR Ranges and Fees: What to Expect

When comparing the cost of an Upstart vs Prosper personal loan, both APRs and fees play a critical role. It's important to note that the lowest rates are typically reserved for borrowers with excellent credit.

| Feature | ||

|---|---|---|

| APR Range | 6.2%–35.99% | 8.99%–35.99% |

| Loan Amount | $1,000–$75,000 | $2,000–$40,000 |

| Minimum Credit Score | 300 | 560 |

| Origination Fee | 1%–8% | 1%–5% |

| Check Payment Fee | $10 | $5 |

| Late Payment Fee | 5% of past due amount or $15 (whichever is greater) | 5% of past due amount or $15 (whichever is greater) |

| Prepayment Penalty | None | None |

| Funding Speed | As quickly as next business day | 3–5 business days |

Upstart's APRs start slightly lower than Prosper's, but both can reach the higher end of the spectrum depending on your creditworthiness. In terms of fees, both lenders charge an origination fee, which is deducted from your loan proceeds. Upstart's origination fees can range from 1% to 8%, while Prosper's are typically between 1% and 5%. For those who prefer to make payments via check, Prosper charges a lower fee ($5) compared to Upstart ($10). Both lenders have similar policies for late payments and neither charges a prepayment penalty, which is a positive for borrowers looking to pay off their loan early.

Answer 3 quick questions and get a personalized recommendation in seconds.

Credit Requirements and Borrower Profiles

The target audience for an Upstart vs Prosper personal loan differs based on their credit requirements. Upstart is known for its willingness to lend to individuals with lower credit scores, with a minimum reported score of 300. This makes it a viable option for those rebuilding their credit or who are new to credit. Their AI model aims to identify creditworthy individuals who might be overlooked by traditional scoring methods.

Prosper requires a slightly higher minimum credit score of 560. While still accessible to fair credit borrowers, it generally appeals to those with a more established credit history. The peer-to-peer model means that investors are evaluating your profile, and a stronger credit history can lead to more favorable offers. If your credit score falls within the 580-720 range, both lenders could be an option, but your specific score and financial situation will dictate which offers you the best terms.

Funding Speed and Customer Satisfaction

When you need funds quickly, the funding speed of your personal loan is a significant factor. Upstart often boasts faster funding times, with many borrowers receiving their funds as quickly as the next business day after loan approval and acceptance. This can be a major advantage for urgent financial needs.

Prosper's funding process typically takes a bit longer, usually 3 to 5 business days after you accept your loan offer. This is partly due to the nature of peer-to-peer lending, where funds are sourced from individual investors. While still relatively fast, it's not as immediate as Upstart's potential turnaround.

Customer satisfaction can also provide insight into a lender's service. According to various review platforms, Upstart generally receives higher marks for customer satisfaction, often attributed to its streamlined application process and innovative approach. Prosper also maintains a good reputation, particularly among its investor community, but may have a slightly lower overall satisfaction rating from borrowers compared to Upstart.

Which is Better for You: Upstart or Prosper?

Choosing between an Upstart vs Prosper personal loan ultimately depends on your unique financial situation and priorities. Here's a breakdown to help you decide:

Choose Upstart if:

- You have a limited credit history or a lower credit score (as low as 300).

- You have a strong educational background and stable employment, which Upstart's AI model values.

- You need funds quickly, potentially as soon as the next business day.

- You are looking for a loan amount between $1,000 and $75,000.

Choose Prosper if:

- You have a fair to good credit score (minimum 560) and a more established credit history.

- You prefer a peer-to-peer lending model.

- You are looking for potentially lower origination fees (1%–5%).

- You are comfortable with a funding timeline of 3-5 business days.

- You are looking for a loan amount between $2,000 and $40,000.

For borrowers with credit scores in the 580-720 range, both lenders are worth considering. Upstart might offer a more personalized rate based on your broader financial picture, while Prosper could provide competitive offers from its investor network. It's always recommended to check your rates with both lenders, as this will not impact your credit score and will give you a clear picture of what each can offer.

Who Upstart Is Best For

⚠️ Not a fit if: you need a secured loan, have a bankruptcy in the last 12 months, or need more than $50,000.

What Happens When You Click — 3 Steps

Soft pull only · No impact to your credit score · Takes 2 minutes