Top Personal Loans for 580 Credit Score

At this score range, you'll qualify for some products but with higher rates and stricter terms. Subprime lenders are your primary option.

Before accepting any loan offer, calculate the total cost of the loan (principal + all interest + fees). A lower monthly payment often means paying thousands more over the life of the loan.

Expect rates 5–12% above prime borrowers.

Dispute any errors on your credit report — even one removed negative item can push you into the fair range.

Timeline: 6–18 months of positive activity can improve your score significantly.

AI-powered approval considers education and job history — not just credit score.

Specializes in fair-credit borrowers. Next-day funding available.

No minimum credit score required. Secured loan option available for lower rates.

Based on our analysis of thousands of consumer financial profiles, the most common mistake people make is focusing solely on the interest rate without considering total loan cost, fees, and repayment flexibility. Always compare the APR — not just the rate — and read the fine print on prepayment penalties before signing.

What to Know About Personal Loans with a 580 Score

Your credit score is one of the most important factors lenders use to determine your interest rate and loan amount. A 580 score (Fair Credit) means you have limited credit history or some negative marks. Understanding where you stand helps you target the right lenders and negotiate better terms.

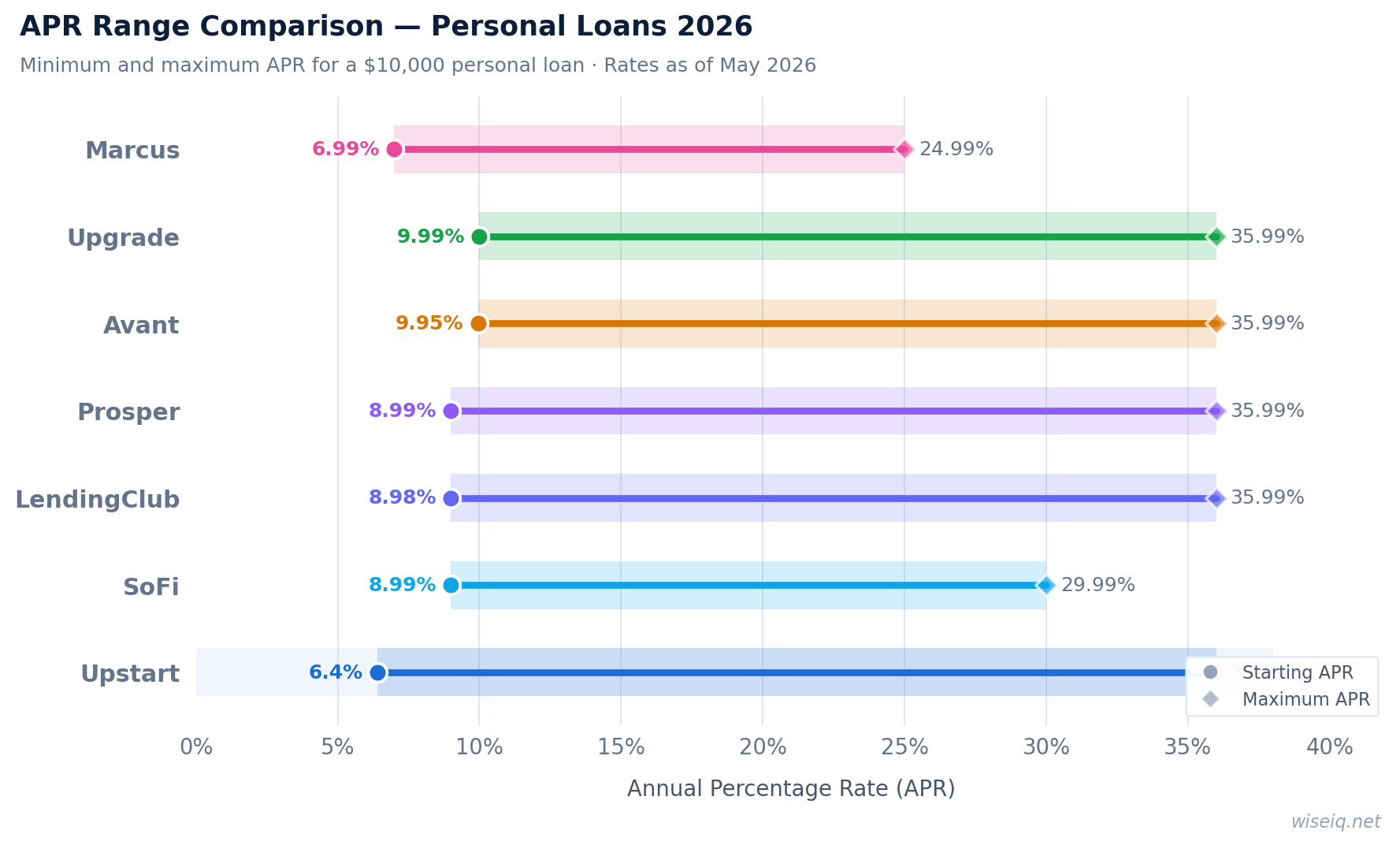

When comparing personal loans, focus on the Annual Percentage Rate (APR) rather than just the interest rate. The APR includes all fees and gives you the true cost of borrowing. Also compare loan amounts, repayment terms, and whether the lender charges origination fees, prepayment penalties, or late fees.

Answer 3 quick questions and get a personalized recommendation in seconds.

How to Get the Best Rate with a 580 Score

Even with a 580 credit score, there are several strategies to improve your offered rate. First, always pre-qualify with multiple lenders before accepting any offer — this uses a soft credit pull that doesn't affect your score, and comparing offers takes less than 10 minutes. Second, consider the loan term carefully: shorter terms typically come with lower interest rates, though monthly payments will be higher. Third, if you have a trusted family member or friend with excellent credit, adding them as a co-signer can significantly lower your rate.

Reducing your debt-to-income ratio before applying is another powerful lever. Lenders look at how much of your monthly income goes toward debt payments — a ratio below 35% is generally considered favorable. Paying down existing credit card balances before applying can improve both your credit score and your debt-to-income ratio simultaneously.

Find Your Best Personal Loan

Compare rates from top lenders in 2 minutes. No credit impact.

Compare Personal Loan Rates →What to Expect When Applying with a 580 Credit Score

A 580 credit score puts you in the "fair" credit range (580–669 by FICO's definition). You will qualify for personal loans, but with meaningful restrictions: APRs will typically be 20%–36%, loan amounts will be capped lower than for good-credit borrowers, and some lenders will require proof of income or employment verification that good-credit borrowers don't need.

The most important thing to understand: at 580, the difference between lenders is enormous. The best offer might be 22% APR; the worst might be 36% APR. On a $5,000 loan over 3 years, that difference is $700 in extra interest. Shopping multiple lenders — using soft-pull prequalification that doesn't affect your score — is essential at this credit level.

How to Improve Your Odds of Approval at 580

Credit score is one factor, but lenders also evaluate your debt-to-income ratio, employment stability, and income. Here's how to strengthen your application:

Calculate your DTI before applying. Add up all monthly debt payments and divide by gross monthly income. Most lenders want a DTI below 40%. If yours is higher, paying down a credit card balance before applying can improve your odds without waiting for your score to change.

Apply with a co-signer if possible. A co-signer with a 680+ score can dramatically improve your approval odds and lower your rate. The co-signer takes on equal responsibility for the loan, so this is a significant ask — only pursue it if you're confident in your repayment ability.

Show income stability. Lenders at this credit level scrutinize income more carefully. Having 12+ months at the same employer, or consistent self-employment income with tax returns to prove it, significantly helps your application.

Real Cost Comparison: 580 Score vs. 680 Score

Understanding the actual dollar cost of a 580 score helps you decide whether to apply now or spend 3–6 months improving your score first.

| Scenario | $5,000 Loan | $10,000 Loan |

|---|---|---|

| Score 580 — 28% APR, 36 months | $2,189 total interest | $4,378 total interest |

| Score 680 — 14% APR, 36 months | $1,109 total interest | $2,218 total interest |

| Savings from improving score first | $1,080 saved | $2,160 saved |

If you can raise your score from 580 to 680 in 3–6 months (by paying down credit card balances and disputing any errors), you could save over $1,000 on a $5,000 loan. Whether that's worth waiting depends on how urgently you need the funds. Use our Credit Score Simulator to see what actions would raise your score fastest.

Alternatives to a Personal Loan at 580

Before taking a personal loan at 25%+ APR, consider whether any of these alternatives fit your situation:

Credit union loans. If you're a member of a credit union, their personal loan rates are often 2–5 percentage points lower than online lenders for the same credit profile. Many credit unions also offer "credit builder loans" specifically designed for rebuilding credit.

Secured personal loans. Some lenders offer secured personal loans where you put up collateral (a savings account, car, etc.) in exchange for a lower rate. The risk: if you default, you lose the collateral.

0% APR credit cards. If your need is for a smaller amount ($1,000–$3,000) and you can pay it off within 12–15 months, a 0% intro APR credit card is cheaper than any personal loan. Some cards are available to fair-credit borrowers, though the credit limits may be lower.

Check Your Rate — No Credit Impact

See personalized loan offers for your 580 credit score in 2 minutes.

See My Options →