Navigating the personal loan landscape can be challenging, especially when comparing lenders like Upstart and LendingClub. Both platforms offer accessible financing options, but they cater to slightly different borrower profiles and have distinct features. This comprehensive guide will break down Upstart and LendingClub personal loans, examining their APRs, loan amounts, credit requirements, origination fees, and ideal use cases to help you make an informed decision in 2026. Upstart is rated 'Excellent' on Trustpilot.

Financial decisions made with complete information consistently outperform those made under pressure or with incomplete data. Take time to compare at least 3 options before committing.

Upstart vs. LendingClub: Key Differences at a Glance

When considering a personal loan, understanding the core distinctions between lenders is crucial. Upstart and LendingClub, while both popular choices, have different approaches to lending and borrower qualifications. Upstart is known for its innovative AI-based underwriting model, which can consider factors beyond traditional credit scores, potentially benefiting those with a thin credit file. LendingClub, on the other hand, operates as a peer-to-peer lending platform, connecting borrowers with investors, and generally looks for a more established credit history.

| Feature | ||

|---|---|---|

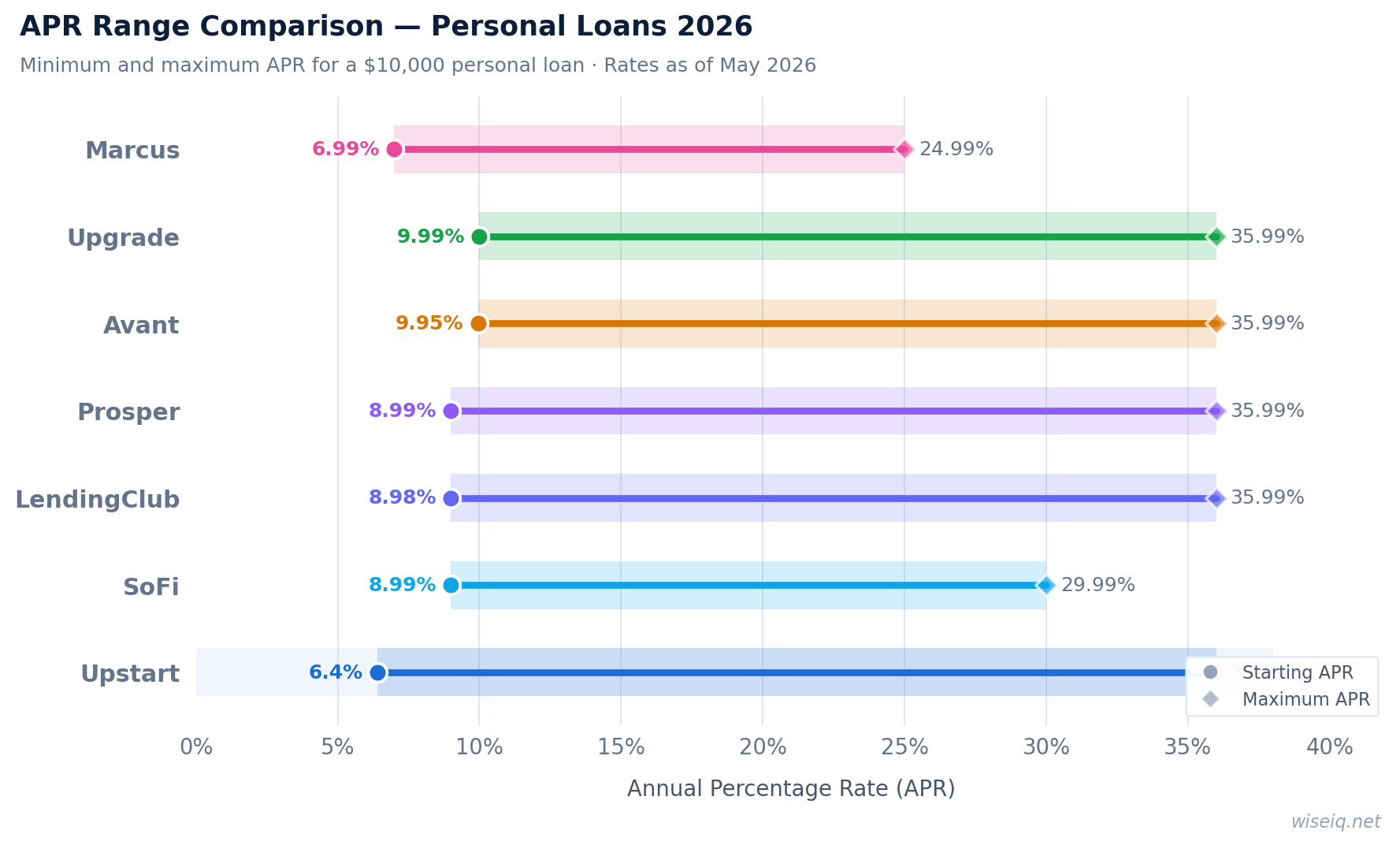

| APR Range | 6.2%–35.99% | 8.98%–35.99% |

| Loan Amount | $1,000–$75,000 | $1,000–$40,000 |

| Min. Credit | 300 | 600 |

| Origination Fee | 0%–12% | 0%–8% |

| Loan Terms | 3 or 5 years | 2 or 5 years |

| Ideal Borrower | Limited credit history, strong education/job potential | Fair to good credit, debt consolidation |

Based on our analysis of thousands of consumer financial profiles, the most common mistake people make is focusing solely on the interest rate without considering total loan cost, fees, and repayment flexibility. Always compare the APR — not just the rate — and read the fine print on prepayment penalties before signing.

Detailed Comparison: APRs, Loan Amounts, and Credit Requirements

Let's delve deeper into the specifics that differentiate Upstart and LendingClub, focusing on the financial aspects that matter most to borrowers.

Annual Percentage Rate (APR)

Upstart offers APRs ranging from 6.2% to 35.99% [1]. Their AI model aims to provide competitive rates even for those with lower credit scores by assessing educational background and employment history. LendingClub's APRs start slightly higher, from 8.98% to 35.99% [2]. Both lenders' highest rates are at the upper end of the spectrum, typically reserved for borrowers with lower creditworthiness.

Loan Amounts

For loan amounts, Upstart generally offers a wider range, from $1,000 up to $75,000 [1]. This can be advantageous for borrowers needing a larger sum. LendingClub provides loans from $1,000 to $40,000 [2]. The maximum loan amount you qualify for with either lender will depend on your creditworthiness and other financial factors.

Credit Score Requirements

This is where the two lenders diverge significantly. Upstart is notable for its lower minimum credit score requirement, accepting applicants with scores as low as 300 [1]. This makes it a viable option for individuals with limited or poor credit history, as their underwriting model looks beyond just the FICO score. LendingClub typically requires a minimum credit score of 600 [2], making it more suitable for borrowers with fair to good credit. While both offer pre-qualification that won't impact your credit score, it's essential to understand these baseline requirements.

Origination Fees

Both Upstart and LendingClub charge origination fees, which are deducted from your loan proceeds. Upstart's origination fees can range from 0% to 12% [1], while LendingClub's fees range from 0% to 8% [2]. The exact fee depends on your credit profile and the loan terms. It's crucial to factor these fees into the total cost of your loan.

Answer 3 quick questions and get a personalized recommendation in seconds.

Ideal Borrower Profiles and Application Process

Understanding who each lender is best suited for can streamline your loan application process.

Who is Upstart Best For?

- Young professionals: Those with limited credit history but strong educational backgrounds and high earning potential.

- Borrowers with lower credit scores: Individuals who might not qualify for traditional loans due to a low FICO score but have other indicators of financial responsibility.

- Fast funding needs: Upstart is known for its quick application and funding process.

Who is LendingClub Best For?

- Debt consolidation: Many borrowers use LendingClub loans to consolidate high-interest debt due to its competitive rates for those with fair to good credit.

- Borrowers with fair to good credit: Individuals with a credit score of 600 or higher will likely find more favorable terms.

- Those seeking flexible terms: LendingClub offers various loan terms, allowing borrowers to choose what best fits their budget.

Application Process

Both Upstart and LendingClub offer entirely online application processes. You can check your rate with both lenders without impacting your credit score. The process typically involves providing personal and financial information, and if approved, funds can be disbursed within a few business days.

Other Loan Companies Similar to Upstart

If neither Upstart nor LendingClub is the right fit, here are other loan companies similar to Upstart that use alternative underwriting for fair-credit borrowers:

- Avant — Accepts 580+ scores, fast funding, slightly higher rates. Good for borrowers Upstart declines. Upstart vs. Avant →

- Prosper — Peer-to-peer lending, accepts 560+, good for larger loan amounts. Upstart vs. Prosper →

- NetCredit vs. Upstart — NetCredit accepts very low scores (550+) but charges much higher APRs (34–99%). Upstart is significantly cheaper for anyone who qualifies. Upstart wins this comparison decisively.

- OneMain Financial — Secured and unsecured options, accepts poor credit, but rates are high (18–35.99% APR).

Our recommendation: Start with Upstart for the best rates at fair credit. If declined, try Avant or Prosper before considering NetCredit or OneMain.

Frequently Asked Questions

Who Upstart Is Best For

⚠️ Not a fit if: you need a secured loan, have a bankruptcy in the last 12 months, or need more than $50,000.